SA & Africa: A View From the Margins

In 60 seconds

South Africa is the diagnostic block at full resolution with the safety rails removed: 2.6% of registered personal income taxpayers pay 66.3% of personal income tax; youth unemployment is 60.7%; the state is present but progressively unable to deliver. Yet SA's debt trajectory is now favourable relative to the US, S&P upgraded it to BB in November 2025, and the rand strengthens on fiscal discipline. The periphery has become the comparative case.

I write this from Cape Town.

The previous essay closed by pointing past itself: the K-shape that runs through the dollar system between countries does not stop at the comfortable end of the institutional-quality distribution, and what the mechanisms look like when they run without the reserve-currency option and without the deep institutional buffers is not visible from inside the developed-world data the diagnostic block has been working with. That is the essay this one is. The view is from the institutional-margin end of the K-shape, written by a South African chartered accountant with a parenthetical promised at line sixteen of essay one, expanded here at full strength.

The argument has three propositions. First, South Africa is the clinical-extreme case of the mechanisms documented in less acute form across the diagnostic block — sovereign debt approaching 95% of GDP on the broader liability measure without reserve-currency option; a tax base narrowed to a degree no developed economy has yet experienced; institutional capture documented at ground level over a fifteen-year window; a labour market structurally broken in a configuration that inverts the developed-world demographic problem. Second, the lessons run in both directions. South Africa prefigures what developed economies look like as their institutional buffers thin; it also contradicts the simpler "global pressures produce global outcomes" reading, because the institutional-quality axis — Acemoglu's framework, with Wade's developmental-state corrective — explains why South Africa is here and most of East Asia is not. Third, the investment implication is uncomfortable but specific. South African equity has been a structural value-trap on domestic fundamentals. The rand is structurally weak for institutional-quality reasons, not cyclical ones. The JSE Top 40's offshore-earnings exposure is the dominant pricing factor, not domestic South African conditions. Capital allocation is rewarded by the kind of system the capital is deployed inside, not by which country one happens to live in.

The discipline guards against two well-known failure modes. South African analysis from outside the country tends toward Afro-pessimism doom; analysis from inside tends, in roughly equal measure, toward rainbow-nation apologism. Both are outside the discipline this manuscript operates under. The honest read is structural and clinical: the assets are real, the liabilities are real, the institutional configuration that produces both is explicable on the institutional-economics framework, and the trajectory is determined less by which party holds power than by whether state capacity recovers fast enough to outrun the fiscal arithmetic.

I. The Two Shock-Absorbers South Africa Does Not Have

The Math Doesn't Work opened on the United States fiscal arithmetic: federal debt approaching 100% of GDP, Ferguson's Law breached in FY2024, mandatory spending plus net interest at parity with total federal revenues. The argument turned on a structural feature the essay made explicit but did not lean on: the United States can run that arithmetic for longer than its peers because it operates with two shock-absorbers no other economy possesses at the same scale.

The first shock-absorber is the reserve-currency option. The dollar is the global unit of account; US Treasury debt is the global risk-free asset; foreign demand is structurally inelastic to US fiscal probity because no alternative reserve asset exists at scale. The World Outside America documented this on Setser's data: the renminbi is at 2.5% of COFER after a decade of explicit Chinese policy effort; the ~$13 trillion of dollar-denominated debt outside the United States produces transactional demand for dollars regardless of any country's stated dedollarisation intent. When the fiscal arithmetic eventually bites, the United States can monetise — at considerable cost to the dollar's purchasing power, but inside an architecture where the alternative reserve asset has not yet been built.

The second shock-absorber is the institutional-quality buffer. State institutions — the tax authority, the central bank, the courts, the regulatory framework, the federal bureaucracy — survive political pressure with degraded but measurable capacity. The buffer is thinning. It is not absent.

South Africa has neither shock-absorber. It borrows in a currency structurally weak against every reserve currency it trades against, at a sovereign risk premium reflecting sub-investment-grade credit ratings affirmed by all three major agencies.1 When the fiscal arithmetic bites, there is nowhere to go: monetisation by the South African Reserve Bank2 would collapse the rand on a one-way trajectory. The institutional-quality buffer has been progressively hollowed out across a fifteen-year window — the State Capture period 2014–2019 documented by the Zondo Commission, the partial recovery 2019–2024 in specific institutions (SARS under Edward Kieswetter, the National Prosecuting Authority's reconstitution, Eskom board professionalisation), the Government of National Unity following May 2024. In aggregate, on the trajectory of state delivery, the buffer operates today at materially less than the capacity South Africa possessed in 2008.

Every figure that follows is to be read as: this is what the developed-world arithmetic produces when it runs without the reserve-currency option and without the institutional-quality buffer. The result is not a different system. It is the same system, observed at higher resolution, with the safety rails removed.

II. The Fiscal Arithmetic at the Margin

Single most arresting fiscal datum in the manuscript

| Cohort | % of registered taxpayers | % of personal income tax collected |

|---|---|---|

| Top 1% of registered taxpayers | 1.0% | ~43% |

| Top 2.6% of registered taxpayers | 2.6% | 66.3% |

| Top 5% of registered taxpayers | 5.0% | ~78% |

| Top 25% of registered taxpayers | 25% | ~96% |

Source: SARS Tax Statistics 2024/25. The 2.6% / 66.3% pair is the binding institutional fact about the SA fiscal base, and a sharper version of the K-shape the manuscript's diagnostic block diagnosed in the US.

| Metric | South Africa | United States |

|---|---|---|

| Gross debt / GDP, peak | 78.9% (2025/26) | ~100% and rising |

| Trajectory after peak | Falling to 77.3% (2026/27) | Rising through 2030s under any baseline |

| Sovereign rating direction | Upgraded BB Nov 2025 (first in ~20 years) | Stable AA+/Aa1; outlooks softening |

| Currency direction | Rand strengthening on fiscal discipline | Dollar plumbing migrating |

| Reform credibility | GNU governance; SARS rebuild; partial Eskom professionalisation | Trust at 17%; Fed independence contested |

The arithmetic resolves through three numbers and one structural relationship. Dawie Roodt at Efficient Group has been the most consistent public reader of these numbers against National Treasury and SARS data for two decades, and the version below leans on his framing of the base.

The narrowed tax base. On SARS National Income Tax Statistics for the 2023/24 tax year, published in November 2024, 2.6% of registered personal income taxpayers paid 66.3% of personal income tax collected.3 Roodt's framing is that the base is so concentrated that the emigration of roughly ten thousand high-income taxpayers per year materially threatens revenue projection. If the equivalent share of the United States personal income tax base were responsible for two-thirds of collection, an individual-income shock of the kinds the diagnostic block has been describing would cascade immediately into fiscal contraction with no available offset. The US base is broader by an order of magnitude. South Africa's is not.

The debt trajectory. The MTBPS of October 2024 projected gross loan debt at 75.9% of GDP for 2024/25, rising to approximately 80.3% by 2025/26.4 Roodt's broader liability measure — sweeping in contingent SOE debt (Eskom, Transnet, SANRAL, PRASA, SAA), unfunded public-sector pension obligations, and subnational arrears — sits in the 90–95%+ range.5 The two measures describe different time horizons of the same balance sheet: the 80% number is what the sovereign is contractually obligated to service today; the 95% number is the liability set once the calling-rate on contingent SOE debt resolves. The fifteen-point gap is the analytical territory the timing question is fought over.

The Ferguson's Law analogue. The Lens of History documented US net interest crossing defence spending in fiscal year 2024 for the first time since the 1930s. South Africa crossed this threshold earlier and at a more acute level. National Treasury Budget Review 2025 and the MTBPS sensitivity tables show net interest absorbing approximately 22–23% of consolidated government revenue in 2024/256 — roughly one rand in five. Net interest now exceeds defence, police, and higher-education allocations; it sits in the same range as basic education; it is materially below only social grants. Once interest consumes this share of revenue in a non-reserve-currency economy, the feedback loop between currency weakness, revenue shortfall, and spending cuts becomes extremely difficult to break without either a primary surplus achieved on a political timeline the diagnostic block is sceptical the system can deliver, or a sovereign credit event of the kind every South African Finance Minister since 2017 has been working to avoid.

The SOE conversion mechanism. Government has absorbed approximately R250 billion in Eskom debt since 2023, with further tranches probable; Transnet's restructuring is in progress; SANRAL operates under explicit guarantee; the Post Office, SABC, and several smaller SOEs are in various states of administration. Contingent liabilities are off-balance-sheet until called, and once called they convert to explicit government debt on a rolling basis. The structural read is that the calling rate matters less than the institutional question of why the contingent stock built up in the first place.

The 2026–2027 watch window for converging developed-world pressures overlaps with the South African fiscal cliff timing: National Treasury's debt-stabilisation window closes in 2025–27 if primary surplus targets are missed, and the rating-agency review calendars are calibrated to that window. The clinical-extreme case may reach its next acute inflection in the same window the manuscript has named for the developed world.

III. The Institutional Framework — Inclusive, Extractive, and the Developmental-State Corrective

The fiscal arithmetic does not explain itself. Two countries can run similar debt-to-GDP ratios and produce wildly different trajectories; two countries can experience similar external shocks and absorb them in radically different ways. The explanatory variable is institutional, and the framework that names it is the one Daron Acemoglu and James Robinson developed across two decades of comparative-historical work and synthesised in Why Nations Fail (Crown Business, 2012).

The framework's core distinction is between extractive and inclusive institutions. Inclusive institutions distribute political and economic power broadly, enforce property rights for wide constituencies, create incentives to invest in productive activities, and generate the conditions under which compounding economic growth is institutionally sustained. Extractive institutions concentrate power and property rights in narrow elite coalitions, channel output toward those coalitions through formal and informal mechanisms, and produce the institutional configuration in which the fiscal narrowing Roodt documents is not accidental but structural — the predictable consequence of an institutional architecture in which the political incentives of the dominant coalition reward extraction over investment, capture over reform, and short-term distributional gains over long-term productive capacity.

Applied to South Africa, the framework reads as follows. The post-apartheid settlement of 1994 inherited an extractive institutional architecture — race-based exclusion from formal economic participation, a state apparatus designed to enforce that exclusion, a tax base narrowed by the exclusion to the white minority — and had the constitutional opportunity to build inclusive institutions across a generational timeframe. The early successes were real: the constitutional settlement was broadly legitimate; the Constitutional Court was assembled with credibility intact; SARS under Pravin Gordhan (1999–2009) was a genuine state-capacity success that broadened the formal tax base, modernised collection, and for several years produced revenue overcollection sufficient to fund the social-grants expansion; the South African Reserve Bank operated with monetary-policy independence comparable to the most respected central banks in the developed world. The institutional design was inclusive in intent and in early operation.

What followed, across the 2009–2019 window, is what Acemoglu's framework predicts when extractive incentives are not actively contained by inclusive institutional scaffolding. Distributional coalitions — the political-economy term Mancur Olson used in The Rise and Decline of Nations and that The Democratic Trap will anchor — captured progressively more of the state machinery. The State Capture Commission (the Zondo Commission, 2018–2022) documented the mechanism in granular forensic detail: procurement processes redirected, regulatory bodies politically appointed, SOEs hollowed out by selective contract awards, the National Prosecuting Authority and the Hawks compromised, SARS itself partially captured under Tom Moyane's commissionership 2014–2018 with tax revenue under-collection of approximately R50 billion per year by the late 2010s on Treasury reconstruction estimates. The decay was not the consequence of bad individual actors making bad decisions; it was the consequence of an extractive equilibrium becoming self-reinforcing inside an institutional architecture designed to be inclusive but lacking the political-economy mechanisms to insulate the inclusive design against the distributional pressure exerted on it.

The framework has limits, and the libertarian reading of Why Nations Fail — that smaller, less interventionist states would have prevented the capture — is the wrong reading of the South African evidence. The corrective is Robert Wade — LSE political economist whose Governing the Market (Princeton UP, 1990) is the canonical statement of the East-Asian developmental-state framework — the most rigorous counterweight to the extractive-vs-inclusive institutional dichotomy. Wade's argument is that the East Asian developmental successes of the second half of the twentieth century — Taiwan, South Korea, Singapore, and to a meaningful degree Japan — were not built on market liberalism. They were built on active state intervention in capital allocation, directed via export-promotion regimes, managed exchange rates, and industrial policy that disciplined failing firms as ruthlessly as it supported successful ones, sustained by a professional civil service insulated from short-term distributional capture and a political compact connecting growth to legitimacy. The state in those cases was large, active, and interventionist. The reason it worked is not that it was absent from the market; it is that it had the institutional capacity to intervene coherently — what the political-science literature has come to call state capacity, distinct from state size.

The lesson for South Africa, reading Acemoglu through Wade, is therefore not "less state" but "more state capacity." The distinction is precise. State presence is the question of whether the state operates in a particular domain — collects the tax, supplies the electricity, runs the rail network, enforces the contracts. State capacity is the question of whether the state can actually deliver the function it has nominally assumed. South Africa's institutional decay has not been a reduction in state presence — the state has, if anything, expanded its nominal footprint across the post-1994 decades. The decay has been in state capacity. Eskom is the cleanest example: an electricity utility that supplied the grid with approximately 95% reliability through the 1990s now operates the rolling load-shedding regime that, at peak in 2022–23, removed up to 11 hours of grid power per day from the productive economy. The state did not retreat from the electricity domain; it remained nominally present and progressively lost the capacity to deliver. The trade-off is between state presence and state capacity. The South African configuration expanded the former and lost the latter, and the loss is what the foregoing fiscal arithmetic is the financial shadow of.

The honest limit of Why Nations Fail, which Wade's critique sharpens, is that the inclusive-versus-extractive dichotomy describes the difference between good and bad institutional configurations but provides limited guidance on the transition pathway from the second to the first, especially where both historical institutions and the reform constituency are contested simultaneously. The post-1994 institutions were designed to be inclusive; the institutional hollowing happened anyway, not because the design was flawed but because the political economy of redistribution in the most unequal society in the world (Gini coefficient consistently at or above 0.63, the highest sustained reading nationally reported in any major economy) created incentive structures that the inclusive design could not insulate against. Institutional quality is necessary but not sufficient. You also need the political compact connecting growth to legitimacy — and that compact, in South Africa, was contested from the start by distributional pressures the inclusive design lacked the mechanisms to manage.

IV. State Capture and the Formal-Informal Interface

The institutional-economics framework names the configuration. What it cannot do, from the level of abstraction at which it operates, is show what the configuration looks like at ground level — what state capture means in the daily operation of the institutions Acemoglu describes, what the formal-informal interface looks like when state capacity has degraded but the population still requires the functions the state nominally provides, what the criminology of institutional decay actually documents about the mechanics of how rent extraction reproduces itself once the institutional incentives have tilted.

Jonny Steinberg's ethnographic work on state capture, criminal economies, and institutional decay is the most rigorous available account of how that formal-informal interface actually operates. His project across four books patiently documents, in close contact with the populations he writes about, what happens to South African state delivery and to the parallel informal institutions that absorb the demand the state cannot meet. The Number (Jonathan Ball, 2004) examined the 28s prison gang as a parallel institution with a four-hundred-year doctrinal history more durable than any post-apartheid state institution. Three-Letter Plague (Jonathan Ball, 2008) tracked HIV/AIDS through the public health system across the years of state denialism, documenting informal-network substitution where the formal state was politically prevented from providing care. One Day in Bethlehem (Jonathan Ball, 2019) examined a single killing in a rural Eastern Cape town and traced the formal-informal interface in the legal system at a granularity no aggregate-data argument could deliver.

The argument Steinberg's body of work assembles is not primarily about state capture in the high-political sense — the Zuma-era networks, the Gupta family, the procurement scandals the Zondo Commission documented. It is about the next level down: what happens to the formal-informal interface when state institutions lose the capacity (not merely the will) to deliver their designated functions across the daily transactions in which most South Africans encounter the state. The central observation, paraphrased here because the verbatim is distributed across the four books rather than in a single quotable formulation, is that when the formal state withdraws — through corruption, through underfunding, through patronage prioritised over service, through the accumulated incompetence of a cadre-deployment system that promotes loyalty over capacity — the informal economy does not collapse into the vacuum. It substitutes. The substitution is often organised: gang structures, informal credit and collection networks, neighbourhood policing by street committees and private security companies, informal land tenure systems with their own enforcement mechanisms, informal taxation of formal businesses by the actors who effectively control specific physical territories. Steinberg is not romantic about these substitutions — The Number is among other things a rigorous documentation of the brutality of the prison gang as institution — but his central point is that the formal-informal interface is not a binary. It is a spectrum, and South Africa has drifted progressively toward the informal end across the fifteen-year window in which the fiscal arithmetic compounded.

The connection to the manuscript's fourth motif — mechanical, not informed — is the part of Steinberg's documentation the essay needs to surface explicitly. Steinberg's ethnographic work documents a specific pattern: at the operational level, the extraction becomes mechanical. The corruption at a South African traffic department or licensing office or municipal contract-award process does not require a discrete decision by a corrupt official for each transaction. It runs on protocol. There are understood prices for understood outcomes; the price schedule is enforced by the network in which the official participates; the bribe is not a negotiated deviation from an institutional norm but the operational norm itself, mechanically reproduced because the institutional incentives reward reproduction and punish refusal. This is the criminal-economy version of what The End of the Bull Run documents in passive equity flows: the system runs without informed intervention because the mechanism has been progressively automated by the institutional configuration itself. Mechanical, not informed — at the price-discovery layer of the global financial system, and at the operational layer of an institutional-margin economy's daily state functioning. The structural feature is the same.

The investment-implications consequence is not background colour. It is the mechanism that explains why formal-economy investment in South Africa does not generate the returns the legal, regulatory, and financial infrastructure should theoretically support. The risk premium the rand and the South African sovereign credit carry — quantifiable in the spread to US Treasuries, in rand implied volatility, in the equity-risk premium implied by JSE earnings yields against developed-market comparators — is partly a function of the formal-informal-interface dynamics Steinberg documents. The friction cost of operating in an economy where state delivery is partial, rule-of-law enforcement uneven, and parallel informal institutions extract a rent from formal operations across multiple touchpoints, is real and quantifiable. The institutional-quality discount embedded in JSE valuations and rand pricing is not a sentiment problem amenable to a sentiment recovery. It is a Steinberg problem, and resolving it requires the patient institutional rebuilding that one electoral cycle cannot deliver.

V. The Labour Market — The Demographic Crunch Inverted

The Demographic Crunch argued, on Goodhart and Pradhan's framework, that the developed world faces a labour-supply shortage. The working-age population is shrinking; the dependency ratio is rising; the wage-disinflationary pressure of the 1980–2020 period — built on the post-1990 entry of approximately one billion Chinese and Eastern European workers into the global tradeable-goods labour pool, plus the demographic-bulge maturation in the developed economies — has reversed. The structural prediction is that wages press up against capital share, inflation runs structurally hotter than the post-1990 norm, and central banks face a forced choice between accommodating the wage pressure and breaking the employment recovery they have been protecting since the financial crisis.

South Africa inverts this argument structurally and, in inverting it, exposes a feature of the developed-world demographic argument that the inversion makes more visible. South Africa has a young population — median age approximately 28 against the developed-world average of 41 — and has had a formal labour demand problem for two decades, not a supply problem. The structural feature is not that South Africa lacks workers. It is that South Africa lacks the productive economy, the institutional configuration, and the formal-employment infrastructure that would absorb the workers it has into the formal payroll-tax-paying employment relationship that the social compact assumes.

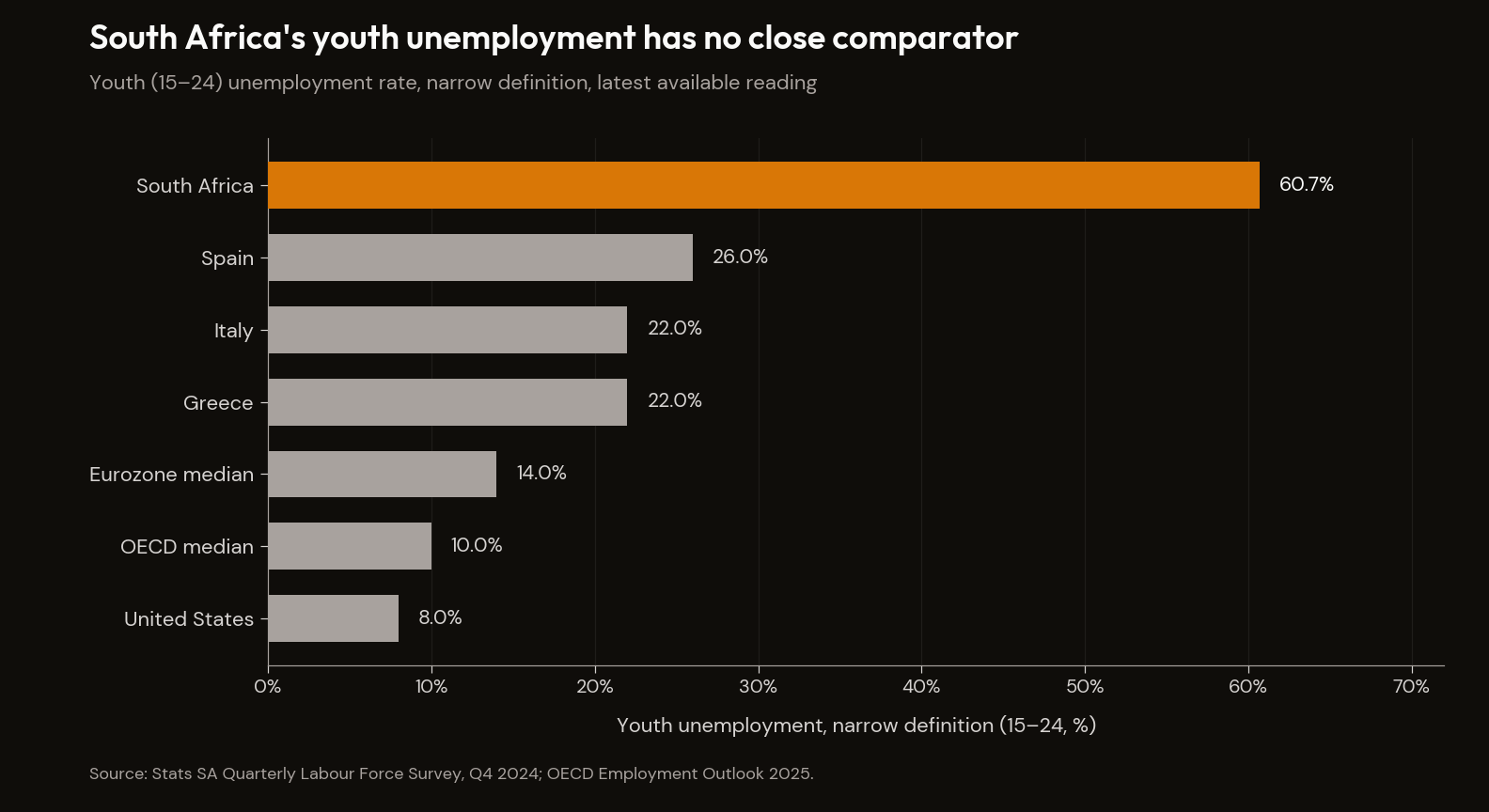

The numbers that anchor the section come from Stats SA's Quarterly Labour Force Survey for the fourth quarter of 2024, the most recent release at the time of writing.7 The narrow unemployment rate sits at 32.9%; the expanded unemployment rate, including discouraged work-seekers who have stopped actively searching but want to work, sits at 42.6%. These are not cyclical readings. They are structural features of the South African labour market that have been sustained, with limited variation, for over a decade. Among middle-income economies they are unusual; sustained at this level over this duration, they are without close comparator. Youth unemployment for the 15–24 age cohort sits at 60.7% on the narrow definition and 67.5% on the expanded definition — among the highest nationally reported youth unemployment rates in any economy outside active conflict zones. These are not cohort-asymmetric entry-level frictions of the kind The AI Reckoning and the Stanford Canaries data document for white-collar American labour markets entering the AI displacement era. They are something more primitive: the absence, across large parts of the South African economy, of the formal employment relationship at all.

What South Africa demonstrates that The Demographic Crunch and The AI Reckoning cannot, from inside their own scope, is what happens when capital-saving technology does not arrive in time, or arrives but cannot be deployed productively against the institutional friction of an institutional-margin economy. The Demographic Crunch describes a world where AI productivity gains race against demographic contraction. South Africa shows the configuration in which the productivity gains either do not arrive or arrive too late: large labour supply (from the demographics), inadequate labour demand (from a productive economy too small relative to the population, hollowed-out by load-shedding and institutional friction, exposed to import competition from precisely the global manufacturing overcapacity The World Outside America documented), and institutional structures that cannot translate the demographic cohort into productive formal employment. Approximately 30–35% of all South African employment, on Stats SA's QLFS measurement, is in the informal sector — a sector that does not pay personal income tax, does not accumulate pension wealth, and does not generate the payroll-tax revenue that would service the entitlement commitments the formal state has made. The fiscal arithmetic compounds because the labour-market structure cannot generate the revenue base to stabilise it.

The motif — addition not substitution — applies in a register the manuscript has not previously deployed it in. The South African demographic cohort adds to labour supply pressure. Institutional capacity to absorb that supply into productive formal employment does not substitute. The young population is not the problem. The institutional configuration that cannot translate young people into productive formal employment is the problem. The optimistic counter-narrative — that Africa's aggregate demographic profile (median age 19, the largest youth cohort in human history entering working age over the next two decades) constitutes the great twenty-first-century structural opportunity — is interrogated honestly by the South African case. South Africa's youth unemployment at 60.7% is the empirical evidence that demographics plus institutional failure equals a dividend deferred, not a dividend delivered.

The cross-essay link to The World Outside America is the K-shape between countries argument, sharpened. The South African labour market is the clinical-extreme resolution of the K-shape: a fully bifurcated economy in which the top decile of income earners (overlapping substantially with the 2.6% of taxpayers carrying 66% of personal income tax) participates in the global capital market and accumulates assets in dollar-denominated wrappers via offshore allowances and globally-listed securities, while the bottom 60% participates in an informal economy that does not generate the formal tax base that could fund the state services the demographic cohort requires. The K-shape that The World Outside America documented at the level of mechanism is, in South Africa, the operational reality of daily economic life.

VI. Investment Implications — The Rand, the JSE, the Value Trap

The investment implications of the structural diagnosis are uncomfortable, specific, and run against several intuitions that the deep-value EM framework consistently produces in the developed-world investor encountering the South African market for the first time. There are three propositions, and the section's task is to state each cleanly and engage the strongest counter to each.

First, South African real GDP per capita has not recovered. On World Bank World Development Indicators — GDP per capita, constant 2015 USD, series NY.GDP.PCAP.KD — South African real per-capita GDP in 2023 was at or below the 2008 level.8 Fifteen years of nominal-economy continuation that, on per-capita real terms, has produced no measurable progress. The 2009 recession was the first leg of the lost decade; the 2015–16 commodity-cycle slowdown extended it; the 2019–20 COVID shock — combined with the load-shedding regime that intensified in the same window — completed the trajectory; the partial recovery 2021–24 has not closed the gap. Cumulative population growth of approximately 18% across the same window means that the formal economy's productive capacity has expanded materially less than the population it must support, which is the per-capita arithmetic version of the same institutional argument running through every section of this essay. The lost-decade is empirical, not rhetorical.

Second, South African equity has been a structural value-trap on domestic fundamentals. Approximately 80% of the JSE Top 40's earnings are generated outside South Africa, by globally operating companies whose primary listing or corporate centre of gravity sits on the JSE for historical reasons but whose revenue base is elsewhere. BHP (which dual-listed and then unified its corporate structure offshore in 2022); Richemont, the Swiss luxury-goods group whose JSE listing reflects the founding Rupert family's historical South African base; Naspers and its Dutch subsidiary Prosus, whose value is dominated by the historical Tencent stake; Anglo American; Glencore. The JSE Top 40, viewed through the offshore-earnings lens, is an exposure to global commodity prices, global luxury-goods cycles, and Chinese technology valuations through a South African holding-company wrapper. The remaining ~20% of earnings are domestically generated, predominantly in financial services, retail, and telecoms — sectors whose performance has tracked the institutional-quality and consumer-spending trajectory of the domestic economy, and which have materially underperformed the offshore-earnings names across the fifteen-year window. The "deep value" thesis on JSE equity, which surfaces periodically when the headline index trades at apparent discounts to global comparators, runs into the offshore-earnings decomposition: the global-earnings exposure can be obtained directly, in deeper and more liquid markets, without the rand currency exposure or the institutional-friction discount. The value looks cheap; the offshore-earnings decomposition answers the question of whether the value is value or a value trap.

Third, the rand is structurally weak for institutional-quality reasons, not cyclical ones.9 The rand has been one of the most volatile emerging-market currencies against the USD, EUR, and GBP across the past twenty years — as a structural condition, not merely in crisis episodes. The weakness has three persistent components. The commodity-currency dimension: South Africa is a commodity exporter; commodity prices are cyclical and volatile; the rand tracks them with considerable amplitude. The current-account-deficit dimension: South Africa runs a persistent current account deficit, which requires continuous external financing and creates the exchange-rate fragility that any reduction in non-resident portfolio inflows immediately reveals. And the institutional-quality discount: when institutional quality deteriorates measurably (the State Capture period; specific ratings events), the rand weakens beyond what commodity prices and the current account alone explain; when institutional quality partially recovers, the rand recovers partially. The Pettis framework from The World Outside America applies cleanly: South Africa is a commodity-surplus economy operating inside a dollar-denominated global system; the Alden flywheel — dollar-denominated debt service amplifying any external shock — compounds the institutional-quality discount; the structural weakness is not amenable to short-cycle reversal in the absence of structural institutional repair.

The capital-allocation lesson generalises and is the section's load-bearing investment claim. The World Outside America argued that the relevant diversification axis is institutional quality and current-account configuration rather than geographic identity. The South African case sharpens this. Capital allocation rewards institutional quality inside which the capital is deployed, not geographic location. The developed-world investor who allocates to South Africa without explicitly pricing institutional quality has bought a value trap, not a value opportunity. The investor whose portfolio carries "emerging markets" exposure via the standard MSCI EM ETF wrapper is, in that portion of their book, holding South Africa at index weight precisely because the wrapper does not implement the institutional-quality screen the structural argument requires. The trade-off is between geographic-aggregate exposure and institutional-quality selection. The two produce materially different outcomes inside the same nominal allocation.

The watch window applies in South Africa with specific timing relevance: National Treasury's debt-stabilisation window closes in 2025–27 if primary surplus targets are missed. Moody's and Fitch have both flagged review of the stable outlook on South African sovereign credit — currently at BB+/Ba2/BB- in sub-investment-grade — if primary surplus targets are not met on the MTBPS schedule.1 A further downgrade into deeper sub-investment-grade territory would trigger forced-selling by EM index funds whose mandates limit such exposure, placing further pressure on the rand and on sovereign spreads. The Government of National Unity's delivery window overlaps with the same fiscal-cliff timing. The clinical-extreme case may reach its next acute inflection in the same window the manuscript has named for the developed world.

VII. Africa Beyond South Africa — The Broader Context

Africa is fifty-four countries. This section locates the South African case inside the continental context and refuses the analytical mistake of either generalising South Africa to Africa as a whole or treating Africa as a single unit. North Africa is a distinct regional pattern from Sub-Saharan Africa; resource-rich economies (Nigeria, Angola, the DRC) operate in a different macro register from the agriculture-and-services-anchored economies (Kenya, Ethiopia, Senegal) or the small open service economies (Mauritius, Botswana, Rwanda).

What the regional aggregates do show, on IMF data through the October 2024 release, is a structural pattern with three load-bearing features.10

The dollar-debt overhang. The post-2008 Eurobond issuance wave left approximately 20 sub-Saharan African economies classified by the IMF and World Bank, on the joint debt-sustainability framework, as in debt distress or at high risk of debt distress.11 The structural feature is shared: dollar-denominated external debt issued in the cheap-rates window and now refinanced at materially higher coupons against revenue bases too small to absorb the post-2022 debt-service step-up. Lyn Alden's flywheel framework operates across the cluster in textbook form; Setser's observation that approximately 70% of EM external sovereign bond issuance remains dollar-denominated is the macro shape it occupies.

Ghana 2022–23 as the live case. Ghana entered IMF programme conditionality in December 2022 with debt-to-GDP that had crossed 100%, external debt service absorbing approximately 60% of government revenue at the peak, and a cedi that had collapsed roughly 55% against the USD in calendar 2022. The 2023 domestic debt exchange imposed substantial losses on domestic bondholders; the external restructuring proceeded through 2024 under common-framework arrangements. The case illustrates how fast the commodity-currency mechanism operates at the institutional-margin extreme, and how the absence of reserve-currency protection makes adjustment faster and more disruptive than developed-world stress episodes.

The Africa-Rising counter-narrative. The 2010s framing — Robertson's The Fastest Billion, McKinsey's Lions on the Move12 — was not wrong about the drivers but was systematically wrong about the institutional preconditions required to translate them into per-capita outcomes. Urbanisation has occurred; formal-sector employment growth has not matched it — primarily informal-sector growth, the same substitution Steinberg documents at South African ground level. Median per-capita growth across Sub-Saharan Africa has been approximately 0.3–0.5% per year since 2015 against population growth of approximately 2.7% per year — per-capita income broadly flat at the median country, with the institutional outliers (Rwanda, Ethiopia pre-2020, Côte d'Ivoire, Mauritius, Botswana) demonstrating what the Acemoglu–Wade framework describes is achievable when institutional preconditions are present.13

South Africa sits at one extreme on a continuum that runs from Mauritius and Botswana at the upper end through Rwanda and Ethiopia through the median Sub-Saharan trajectory to the cluster of distressed sovereigns in IMF programmes. The argument is not that Africa is doomed; it is that the demographic-dividend framing requires an institutional-quality qualifier the Africa-Rising narrative systematically under-weighted, and South Africa is the case that shows what the qualifier costs when it is absent across the time horizon required for the dividend to compound.

VIII. The Coupling

South Africa demonstrates the coupling empirically, in a single country, across a fifteen-year window for which the data are now available with hindsight rather than in the predictive register the developed-world equivalent argument has to operate in. The fragmentation of political legitimacy — the ANC's vote share declining from 62% in 2009 to 57.5% in 2019 to 40.2% in May 2024 and the resulting Government of National Unity — co-evolved with the deterioration of institutional quality across the same window. The structural reading is that institutional decay and political fragmentation co-evolved as a mutually reinforcing system, in the way the institutional-economics framework predicts they will when the inclusive design lacks the political-economy mechanisms to insulate against the distributional pressures the most unequal society in the world generates. The clinical-extreme is the five-conditions-eroded argument The Democratic Trap makes, run forward fifteen years; this essay is the expansion of that paragraph at full strength.

The math is the math. The timing is the question.

What the clinical-extreme case demonstrates, in the country whose fiscal arithmetic opened this manuscript, is that when political fragility and financial fragility couple and compound without intervention, the equilibrium they find is not a gentle one — and the coupling is most visible precisely where the institutional buffers are thinnest.

Footnotes

-

South African Reserve Bank — Quarterly Bulletin. SARB Quarterly Bulletin: monetary-policy independence, FX reserves, and real-GDP series. ↩

-

SARS — Tax Statistics. South African Revenue Service National Income Tax Statistics 2023/24 (published November 2024); concentration of personal-income-tax base in top 2.6% of registered taxpayers. ↩

-

National Treasury — Medium Term Budget Policy Statement October 2024. Gross loan debt 75.9% of GDP for 2024/25, projected to rise to approximately 80.3% by 2025/26 on the MTBPS baseline. ↩

-

Stats SA — Quarterly Labour Force Survey (P0211). Q4 2024 release: narrow unemployment 32.9%; expanded 42.6%; youth (15–24) unemployment 60.7% narrow / 67.5% expanded; informal-sector share of employment ~30–35%. ↩

-

World Bank — World Development Indicators, GDP per capita (constant 2015 USD), South Africa. Series NY.GDP.PCAP.KD; SA real per-capita GDP in 2023 at or below 2008 level. ↩

-

Disruption Banking — How strong will the South African Rand (ZAR) be in 2026?. Rand structural-weakness decomposition: commodity-cycle, current-account-deficit, and institutional-quality components. ↩

-

IMF Regional Economic Outlook: Sub-Saharan Africa. October 2024 release: regional aggregates, country-appendix data, and the post-2008 Eurobond-issuance debt trajectory. ↩

-

IMF — Debt Sustainability Analysis. Joint IMF–World Bank Debt Sustainability Framework for Low-Income Countries; approximately 20 sub-Saharan economies classified as in debt distress or at high risk thereof in the most recent assessment cycle. ↩

-

McKinsey Global Institute. MGI Lions on the Move (2010; updated 2016) — Africa-Rising research underpinning the urbanisation, mobile-money, and demographic-dividend framing. ↩

-

World Bank — Sub-Saharan Africa data. Regional GDP-per-capita and population-growth series; median per-capita growth ~0.3–0.5% against population growth ~2.7% since 2015. ↩