The Case for Optimism

In 60 seconds

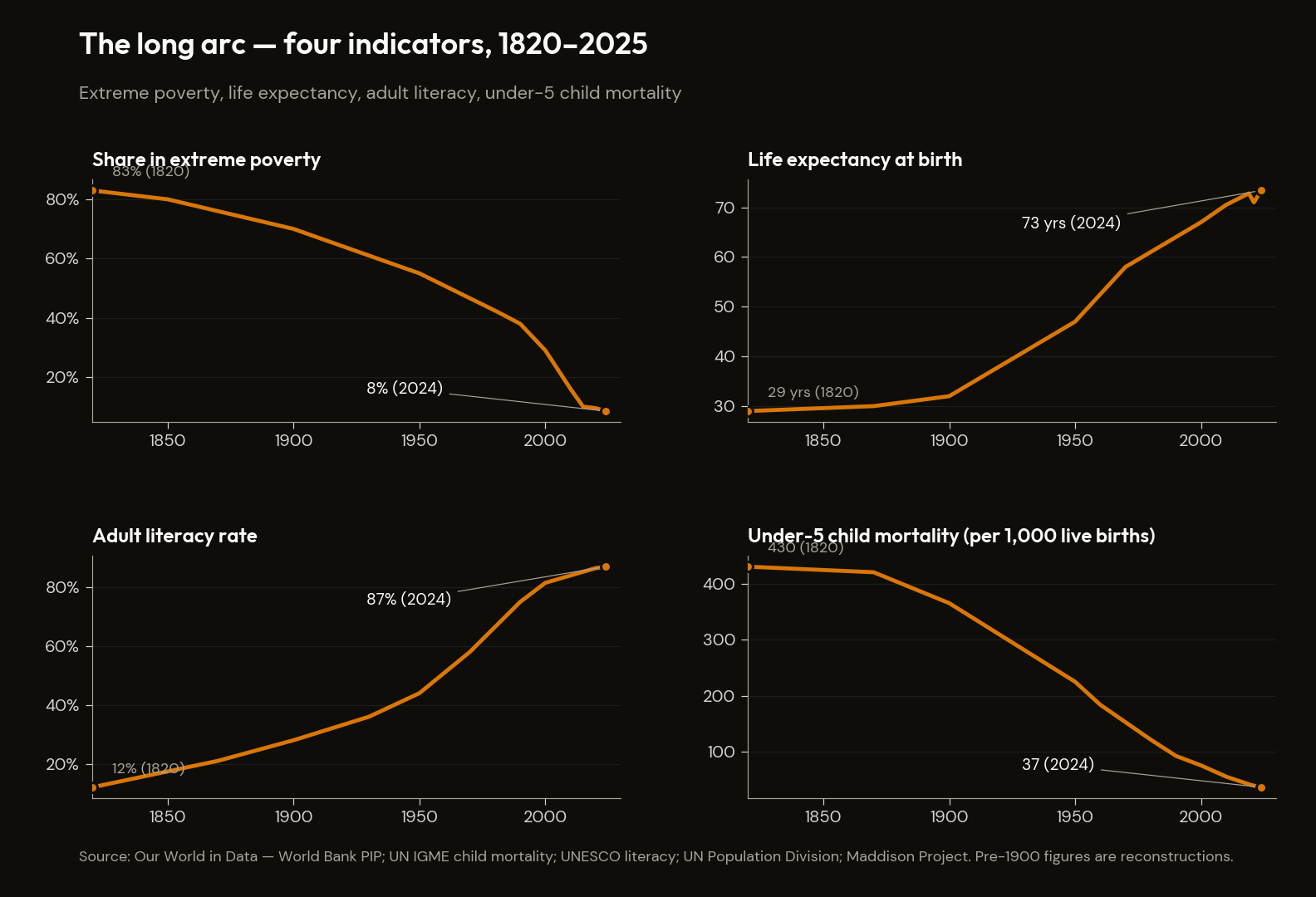

The bear regime is a property of the financial-institutional architecture. The long arc — global poverty 44%→10%, child mortality 18%→4%, literacy 12%→87%, life expectancy 32→73 — is a property of the human capability stock. The two are not in conflict; they operate on different time horizons. Hold both. The post-1933, post-1945 and post-1979 templates show what regenerative resolution looks like — and what preconditions it required, preconditions the current configuration does not have.

The honest counterweight to a bear thesis built across thirteen essays is not a softening of the thesis; it is the disciplined engagement with the strongest available counter-evidence and an accounting of what survives the engagement.

The diagnostic block of this manuscript has built the bear case against the post-2008 financial regime using primary sources and engaged its honest counter-arguments. The sovereign-fiscal arithmetic does not balance. The equity market is priced beyond its underlying cash flows. The demographic tailwind has reversed. The AI capex programme has run ahead of any productivity arithmetic that can credibly justify it. The energy infrastructure cannot be built on the capex timeline the hyperscalers require. The political system is structurally unable to fix any of that before crisis forces the resolution. The 2026–2027 watch window — on the convergent timing of multiple independent macro voices — is the frame this manuscript has asked the reader to be positioned against.

This essay does not retract any of it. It tests the diagnosis against the strongest available counter-evidence and accounts for what survives the engagement.

I. The Two-Horizon Distinction

The essay's load-bearing analytical move is the time-horizon distinction. It must be stated plainly enough that it cannot be misread.

The bear regime is a property of the financial-institutional architecture — sovereign-debt arithmetic, equity-market structure, monetary regime, capex-allocation behaviour, political institutions under fiscal pressure. The long-arc optimism is a property of the human capability stock — knowledge accumulated, institutions built, technologies diffused, health gains compounded across populations. The first can break and reorganise without the second resetting. That is the post-WWII case and, in less dramatic form, the post-1970s-stagflation case: regime-level resolution did not erase the capability stock; it reorganised the financial architecture around it.

The bear regime applies to the 2026–2027 watch window — the period in which sovereign-fiscal arithmetic, equity-market misallocation, demographic inflection, AI-capex overrun, energy-build constraint, and democratic fragility are most likely to crystallise into visible resolution pressure. The watch window is a frame, not a deterministic forecast. The fragility is structural and the convergent timing across multiple independent macro voices is real.

The long-arc capability expansion applies to the multi-decade trajectory of human progress. The thirty-five-year reduction in poverty. The two-generation halving of child mortality. The two-century expansion of literacy. The century-scale extension of life expectancy. These trends are also structural. They are produced by the cumulative-knowledge mechanism, the time-price compounding, the institutional mechanisms — and they have produced, on the data, the most measurable reduction in human suffering in recorded history.

The two are not in conflict. They operate on different time horizons and through different mechanisms. Addition not substitution — the recurring lens of this manuscript — applies as much to the relationship between near-term fragility and long-arc progress as it does to renewables-and-fossils, immigration-and-ageing, China-capacity-and-trade. Long-arc progress adds to humanity's capability stack; it does not substitute for the regime fragility documented elsewhere in the manuscript. Both are real. Both compound. The investment and life implication is asymmetric in time, not zero-sum.

That is the discipline this essay is asking the reader to hold. The rest of the essay does the work to earn it.

II. The Rosling Corrective

The corrective starts from a sharper claim than the popular reading suggests. It is not "the world is good." It is that people who consider themselves well-informed — development economists, journalists, members of the public, and the medical-school students Hans Rosling taught — systematically misread global trends. Not randomly. In a predictable direction.

Rosling tested this empirically across audiences in multiple countries using a thirteen-question quiz on basic global development facts. His consistent finding, set out in Factfulness (Sceptre, 2018): audiences in wealthy democracies performed worse than random guessing on questions about poverty, child mortality, literacy, and vaccination rates. A chimpanzee choosing randomly on a three-option question would score 33%; Rosling's human audiences scored between 7% and 17%.1

The mechanism is ten cognitive instincts that evolved for local stress in small groups and do not scale to global aggregate data. Three are load-bearing here.

The Negativity Instinct. Bad news is more neurologically salient than good news; decline is noticed before improvement. Rosling's corrective: distinguish bad levels from improving trends. The level of extreme poverty — roughly one in ten — is a bad level. The direction of the trend, from roughly 44% in 1990, is an improving trend. Both are simultaneously true. The corrective is to hold the bad news alongside the long-arc data and ask what is also true.

The Straight-Line Instinct. Humans tend to project improving trends as straight lines forward and project deteriorations the same way. Neither is typically warranted. The optimism case is as susceptible to this as the bear case: the poverty and mortality trends have improved consistently for thirty-five years; no mechanism guarantees they continue on the same slope.

The Fear Instinct. Risk that is emotionally salient crowds out accurate probability assessment. Financial crises are emotionally salient to readers of this manuscript. The reduction in child mortality in sub-Saharan Africa is not. The corrective is to assess probability and magnitude on the evidence, not on salience.

Rosling's own formulation, repeated through Factfulness: "things can be bad, and getting better." Not that it is fine. Not that the problems do not exist. The trajectory is more positive than the Negativity Instinct leads well-informed people to conclude. Factfulness is not Pangloss; it is Rosling insisting that intellectual honesty requires the same precision about what is improving that it requires about what is broken.

III. The Long-Arc Empirical Baseline

The world is awful. The world is much better. The world can be much better. Each panel is true. Collapsing into any one of them is dishonest. The diagnostic block of this manuscript has been primarily in panel one. This essay operates primarily in panel two while holding panel three as the honest forward-look — without projecting the trend as a straight line. The tripartite framing is Max Roser's — economist at the Oxford Martin Programme on Global Development and founder of Our World in Data, who has built the most comprehensive open-access primary-source repository on long-arc development indicators. The data points below draw on that repository.2

| Indicator | Pre-1820 baseline (~1820) | 1980 | 2024–25 | Change |

|---|---|---|---|---|

| Share of world in extreme poverty (<$1.90/day, current data) | ~95% | ~44% | <10% | ~85pp fall |

| Child mortality rate (deaths < age 5, per 1,000 live births) | ~430 | 184 | 37 | ~90% fall |

| Adult literacy (% of adult population) | ~12% | ~67% | ~87% | ~75pp rise |

| Life expectancy at birth (global average) | ~32 years | 63 | 73 | +41 years |

Sources: Our World in Data; UN Population Division; UNESCO; World Bank. Note that pre-1820 baselines are reconstruction estimates and carry methodological uncertainty.

The four numbers in the strip table carry the weight. A short note on each.

Extreme poverty: roughly 44% (1990) → approximately 10% (2025). The share of world population below the World Bank's $2.15/day threshold has fallen from approximately 1.9 billion people in 1990 to approximately 700–800 million today — both the rate and the absolute count have fallen, despite the world adding roughly 2.5 billion people over the same period.3 The contested zone — the threshold choice, the PPP-conversion, the K-shape distribution — is engaged in the next section. It does not change the directional finding.

Child mortality: 18.4% (1960) → 3.7% (2024). The under-5 mortality rate has fallen by a factor of five in two generations.4 This is the single most powerful data point: it is the least susceptible to PPP critique (dead children are not a monetary threshold question), the most concrete expression of human suffering reduced, and the clearest methodology. The improvement is multi-causal — vaccination (global DTP3 from near-zero in 1974 to ~85% by 2024),5 oral rehydration, bed nets, nutrition, clean water — and therefore robust to single-intervention failure.

Global literacy: roughly 12% (1820) → approximately 87% (2024). The longest-arc indicator.6 The 1820 figure is a historical reconstruction with wider uncertainty; the directional arc — from a class privilege in the wealthiest societies to near-universal — is uncontested. The absolute count of illiterate adults remains large (~750 million by UNESCO estimates); the rate is the long-arc claim, the absolute count is the panel-three obligation.

Life expectancy: roughly 32 years (1900) → approximately 73 years (2024). The pre-1950 reconstruction carries wider uncertainty; the more conservative 1950 → 2024 arc (47 → 73) gives the same picture.7 The increase is driven overwhelmingly by the reduction in early mortality — the conversion of early death from a probability to an anomaly across most of the world.

These four trends are the most robustly documented in social science. The directional finding is not contested at the data level. It is contested at the threshold level, the distributional level, and the causal-mechanism level — each engaged in what follows.

These are the long arc, not the watch window. Addition not substitution applies at the time-horizon level too.

The mechanism, not just the data

The cohort above shows the long arc happened. It does not show why the long arc has a mechanism that explains its continuation rather than being a happy historical accident.8

Knowledge creation — the open-ended generation of explanations that survive criticism — is a real mechanism, not a metaphor. Problems are inevitable, by the nature of the world having more potential states than any current model describes. Problems are soluble, by the nature of conjecture and refutation as a method for generating better models. The pairing produces a structural prediction: progress is not predetermined to defeat intelligence, because intelligence is the mechanism by which progress is produced. Where intelligence operates with the freedom to err, criticise, and revise, the trajectory of explanations is open-ended rather than bounded.

The empirical cohort — Rosling, Roser, Ridley, Tupy — gives us the long arc happened. Deutsch gives us the long arc has a mechanism. These are genuinely different claims. The first is correct about the past but consistent with many futures (decline, reversion, fragility, secular crash). The second extends the claim into the forward trajectory: the same mechanism that produced the historical record is the mechanism that determines what comes next, and that mechanism is the iterative generation of explanations that are hard-to-vary in Deutsch's specific sense — explanations whose components are tightly coupled, where changing any one part breaks the whole.

Easy-to-vary explanations accommodate any outcome and predict nothing; hard-to-vary explanations make sharp commitments and are testable. The post-1820 trajectory survives because the knowledge that produced it is increasingly hard-to-vary across economic, medical, agronomic, energy-engineering, computational, and now computational-biological domains. The bear case for the manuscript's watch window does not refute the trajectory. The watch window operates inside the trajectory, not against it.

This is what the two-horizon discipline rests on. The watch window is real because the financial-institutional architecture is fragile. The long arc is real because the knowledge stock is generative. The two operate through different mechanisms on different timescales — and the manuscript holds both.

IV. The Strongest Counter — Hickel, Engaged at Full Strength

The structural function of this essay is to test the optimism against its strongest available challenge. Relegating it to a footnote would invalidate the test. The strongest available challenge is Jason Hickel's, and it earns spine status for that reason.

Hickel — author of The Divide (2017) and Less Is More: How Degrowth Will Save the World (2020),9 associate professor at the Universitat Autònoma de Barcelona and visiting senior fellow at LSE — is the most analytically rigorous critic of the Roser/Rosling poverty-progress narrative. The critique has two distinct parts, with different logical structures and different evidential bases. They must be engaged separately.

Part one: the threshold problem. The World Bank's $2.15/day poverty line, Hickel argues, is too low to be meaningful. A person living on $2.15/day cannot meet basic nutritional requirements, cannot afford healthcare or education for their children, and has no buffer against any income shock. To call such a person "not extremely poor" if they cross the $2.16 mark, Hickel argues in his 2017 Third World Quarterly paper "Is global inequality getting better or worse?", is to convert a measurement convenience into a political claim.10 Hickel's preferred threshold — derived from asking what a dignified livelihood actually requires in developing-economy contexts — is approximately $7.40/day in 2011 PPP terms. At this threshold, by his 2017 calculation, approximately 3.4 billion people were in poverty. Roughly half of the world's population.

This is the counter-anchor. It must be conceded as a methodological point.

The response this essay must not give: Hickel is wrong about the threshold. The response this essay can give, and which the data supports: the directional trend survives the threshold critique. Extreme poverty — measured at Hickel's own preferred $7.40/day, and at the World Bank's own intermediate $6.85/day threshold introduced in the Poverty and Shared Prosperity 2022 report — has also declined since 1990.11 The rate of reduction is slower at higher thresholds, because higher thresholds include populations that are poor but not in the deepest poverty, and those populations have benefited less from the growth-driven poverty reduction of the past thirty-five years. The trend still runs the right way. Hickel's threshold is a legitimate methodological dispute. It is not a factual refutation of the trend's direction. The two are not the same thing, and conflating them — in either direction — is the analytical error.

Part two: the degrowth argument. This is Hickel's stronger and more interesting argument, and the one this essay must engage directly rather than deflect. The economic model that produced the poverty reduction over the past thirty-five years — export-led growth, integration into global supply chains, resource extraction, fossil-fuel-intensive industrialisation — is, Hickel argues in Less Is More, ecologically unsustainable. The planetary-boundary framework (Rockström et al., 2009; updated 2023) identifies nine Earth-system processes; as of the 2023 update, six of the nine have been breached.12 Hickel's argument is that the poverty progress of the past thirty-five years and the environmental degradation of the past thirty-five years are not coincidentally simultaneous. They are causally linked. The GDP growth that lifted people from $2.15/day poverty also pushed atmospheric CO₂ past 420 ppm, accelerated biodiversity loss, and committed the planet to temperature trajectories that will, on current projections, create the most severe poverty conditions in equatorial regions within the lifetimes of children born today.

This is the argument the optimism case must engage at full strength and cannot dismiss. The honest synthesis runs in four lines.

The trend in poverty, mortality, literacy, and life expectancy is real, and is among the most important positive developments in human history.

The mechanism that produced the trend has simultaneously produced ecological costs that are now large enough to threaten the trend's continuation.

The optimism case, honestly held, is not that the mechanism is fine. It is that the mechanism is transitioning — imperfectly, unevenly, with enormous political resistance — and that the capability expansion the trend has produced is precisely the human stock of knowledge, institutions, and ingenuity on which the transition must draw. The cumulative-knowledge framework is the structural account for why this is plausible; it does not make it inevitable.

Hickel's degrowth thesis — that the solution requires reducing aggregate economic output in wealthy countries rather than transitioning to a different growth model — is a separate claim from the threshold critique, and one on which the evidence is genuinely contested. This essay does not adjudicate the degrowth debate. It registers the dispute as real, the challenge as legitimate, and the resolution as belonging to the conditional questions the Survival and Opportunity Frameworks must grapple with.

What this essay must do with Hickel: acknowledge that the $2.15/day threshold is a real methodological limitation; note that the directional trend survives higher thresholds; engage the degrowth argument as the more fundamental challenge; conclude that the honest optimism position holds the capability expansion as real and the ecological cost as real — and that the resolution of the tension is the problem the navigation essays must address.

What this essay must not do: strawman the threshold critique as if refuting the direction of the trend is the same as refuting the threshold's validity. It is not. The threshold is a legitimate dispute. The trend direction is not. Both are true.

The optimism survives Hickel. It is a tighter optimism for having engaged him.

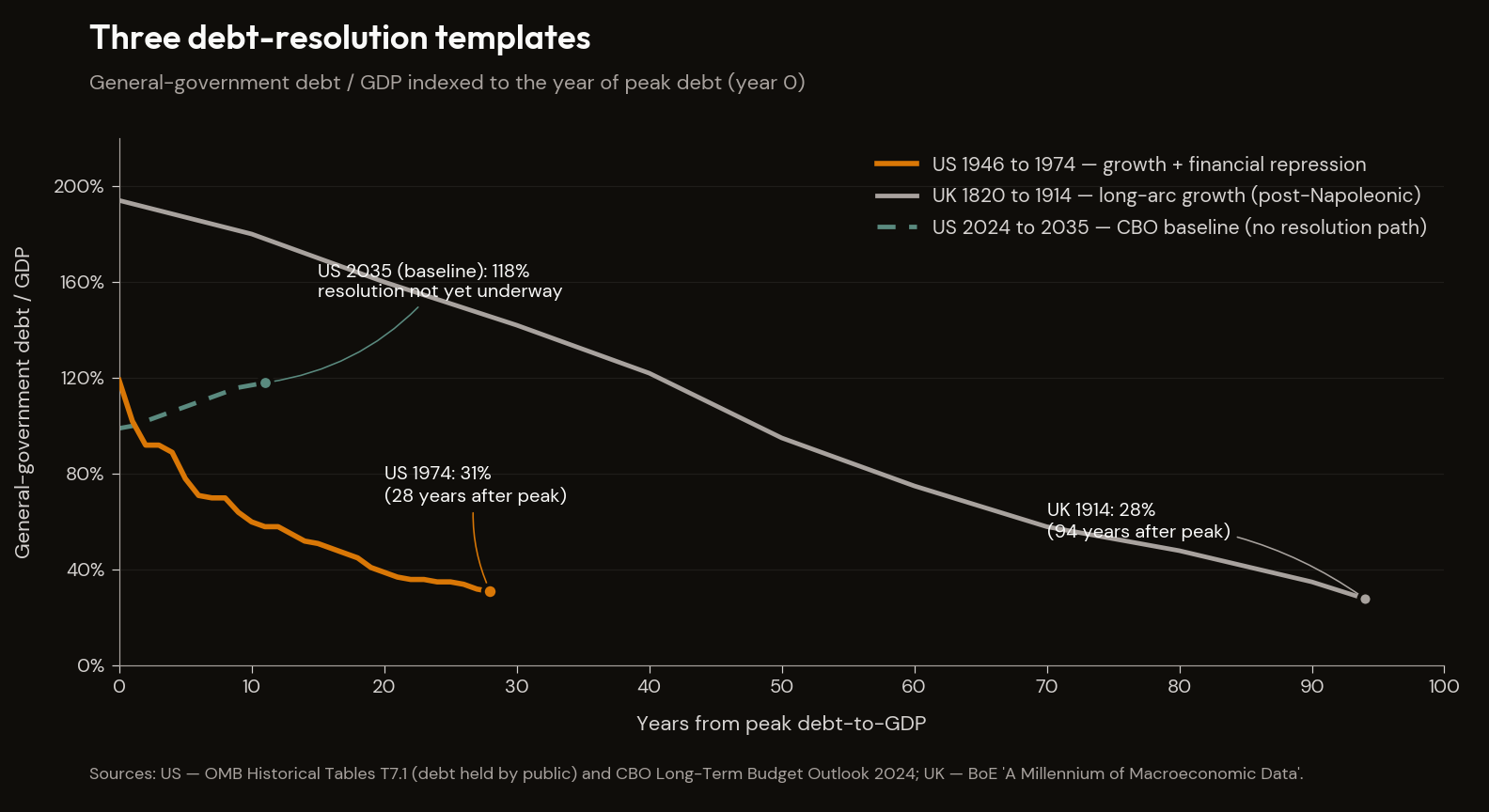

V. The Historical Templates — What the Resolution Side of Comparable Configurations Has Actually Produced

The bear case has, across the diagnostic block, described one side of the constrained set the configuration produces. The other side has a historical record, and that record is the empirical content the optimism case rests on. The post-resolution regime is recognisable across cases — not the same in detail, but recognisable in shape. The financial-institutional architecture reorganises; the human capability stock is preserved through the reorganisation; the regime that emerges on the other side runs for one to three decades before the next destabilisation begins. That is the regenerative-resolution thesis, and it is the analytical contribution of this essay.

Neil Howe's The Fourth Turning Is Here (Simon & Schuster, 2023) carries the load-bearing piece: the empirical observation that post-crisis regimes have been, on the historical record, more cohesive, more institutionally robust, and more economically productive than the pre-crisis regimes whose decay produced the crisis.13 The metaphysics — eighty-year saecula, four-turning archetypes, generational drivers as causal mechanism — are not what does the analytical work here, and the manuscript is not committed to them. The historical observation about the resolutions themselves does the work. Across recognisable cases, the resolutions cluster: institutional architecture rebuilt, sovereign-balance-sheet restructured, capital reallocated from the decaying regime to whatever architecture is being constructed on the other side.

Three historical templates carry the empirical weight.

Post-1933 / The New Deal fiscal-and-regulatory reset. The most direct analogue to the present configuration: a sovereign-fiscal architecture broken under accumulated commitments, a financial system whose intermediation function had failed, a political settlement under redistributive pressure, contested institutional architecture for whether resolution would arrive within democratic norms. The resolution was the New Deal's reconstruction — Glass-Steagall, deposit insurance, securities regulation, the Wagner Act, Social Security.14 The reform did not solve the configuration on its own; the post-WWII Bretton Woods architecture did the harder work, and the New Deal regime was its precondition. The New Deal case is the closest available evidence that such a reset is executable within democratic institutions. The capability stock the 1930s economy carried through the reorganisation was not destroyed; it was redirected.

Post-1945 / Bretton Woods. The configuration before: sovereign-debt arithmetic that did not balance, the worst peacetime depression on record, political extremism that scaled to war. The resolution was not orderly. The post-1945 architecture — Bretton Woods fixed exchange rates and capital controls, the Marshall Plan reconstruction, welfare-state consolidation, the dollar's enthronement as the reserve asset.15 The post-resolution regime ran for roughly twenty-five years and generated the broadest-based productivity expansion in modern history, the most measurable middle-class formation in any comparable period, and the institutional infrastructure within which the late-twentieth-century technology stack was built. The reorganisation was not the avoidance of the crisis; it was the architecture that emerged when the crisis forced one.

Post-1979 / The Volcker-Reagan disinflation regime. The configuration before: 1970s stagflation, dollar credibility under attack, inflation at 14.8 percent in March 1980, OPEC shocks compounding the underlying breakdown.16 The resolution was Volcker's 1979-1981 interest-rate-driven disinflation despite 10.8 percent unemployment,17 paired with the post-1982 tax-reform and capital-market-liberalisation regime that anchored the next forty years. The post-resolution regime delivered the largest equity bull market in measurable history. The point that matters: the world's most valuable companies of the cycle that followed — Microsoft 1975, Apple 1976, Home Depot 1978 — were built inside, or immediately preceding, the structurally flat nominal-return environment of the late 1970s, and inherited the post-resolution capital-market architecture that scaled them. The institutional resolution did not vaporise capital. It reorganised it around the architecture that was being constructed.

| Post-1933 / New Deal | Post-1945 / Bretton Woods | Post-1979 / Volcker-Reagan | |

|---|---|---|---|

| Crisis trigger | 1929 crash + 1932 Depression trough | WWII economic exhaustion + Soviet-bloc rivalry | 1979 inflation crisis; institutional-credibility collapse |

| Mechanism of resolution | Regulatory reset; deposit insurance; Glass-Steagall; SEC; Social Security | International monetary architecture; capital controls; Marshall Plan reflation | Real-rate shock; financial-repression unwind; supply-side tax + deregulation |

| Preconditions present | Hegemonic position; demographic upcycle; institutional-elite consensus | Hegemonic position post-war; demographic upcycle; bipartisan elite consensus | Institutional-credibility recovery via Volcker; coherent political coalition; demographic dividend |

| Time to regime stabilisation | ~6–8 years | ~3–5 years | ~5–7 years |

| Current analog preconditions | None of three present (no hegemony, no demographic upcycle, no elite consensus) | None of three present | One partially present (institutional credibility partially intact via central bank); two missing |

The honest reading: each historical template required a precondition stack that the current configuration does not have. The regenerative-resolution thesis is real but does not arrive cheaply — none of the prior templates worked without all three preconditions in place. The current period's resolution will look like none of these three exactly.

What changes the calculus is that none of the three resolutions was chosen. The post-1933 reset, the post-1945 reconstruction, and the post-1979 disinflation were the politically least costly options remaining after every other path had been exhausted. The 1933 settlement was assembled because the alternative — continued banking collapse and deepening Depression — had become more politically dangerous than reform. The 1945 reconstruction architecture was assembled because the alternative — drift back into 1930s-style competitive devaluation and trade collapse — was no longer survivable for the political class that had lived through it. The 1979 disinflation was undertaken at 10.8% unemployment because the alternative — continued accelerating inflation through a third presidency — had become electorally fatal. The current configuration is approaching the same exhaustion point on the same arithmetic. The preconditions for regenerative resolution may not be present in advance; on the historical record they are typically produced by the crisis itself — institutional credibility is rebuilt in the resolution, political coalitions form when the no-resolution path becomes the more dangerous one, and the demographic constraint is partially absorbed by the cost-curve and productivity shifts the resolution unlocks. The post-2026 reset, when it arrives, will look like none of the three templates exactly — but it will look like a reset, because that is what configurations in this state produce when the alternatives are exhausted.

The honest objection — what the templates do not have

The three templates do not resolve the question of which path the present configuration produces. They constrain the set. The strongest objection is that each template required a precondition stack the current configuration does not have — institutional credibility (the present sovereign sits at 17% trust in federal government, with V-Dem Liberal Democracy Index in a 24% one-year decline),18 hegemonic position (the United States now in contested-hegemony posture against China), and a demographic dividend (now in RMD-driven decumulation rather than peak earning years). The asymmetry is real: the regenerative path requires institutional capacity to assemble new architecture under duress, and assembly happens through political institutions whose capacity to act coherently is at historical lows.

What the templates do show is that the shape of regenerative resolution is recognisable across cases. The institutional credibility of the failing architecture is repriced in real time; capital reallocates, slowly and then suddenly, toward whatever architecture is being constructed; the entrepreneur or allocator who is solvent at the resolution participates in the construction. The shape is what the historical record constrains. The specifics — and whether the assembly succeeds — are decided under the configuration in real time.

The regenerative resolution is not guaranteed. The historical record contains the alternative paths: revolutionary collapse, territorial fragmentation, resolutions that extend the crisis indefinitely. This section establishes only that the regenerative path is among the better-probability outcomes of the constrained set — not because it is inevitable, but because, in the cases where comparable configurations have resolved, this is recognisably what the resolution side has produced. The optimism is not consolation. It is the discipline of refusing both ends of the temptation — the bear case's tendency to extrapolate the watch-window fragility across the multi-decade arc, and the optimism case's tendency to forecast the regenerative resolution as if it were already arriving.

VI. The Howe Qualification — Headwinds to Regenerative Resolution

One structural qualification on the Hero Generation thesis sits inside Howe's own framework and deserves naming. The GI Generation's consolidating function — assembling the post-1945 settlement from a fragmented pre-war order — operated under three structural conditions that do not describe the Millennial cohort in the same configuration.

First, ideological bifurcation. Pew's three-decade polarisation tracking registers a roughly sixfold increase in the share of each party holding consistently ideological positions; Iyengar and Westwood's affective-polarisation data show the partisan feeling-thermometer gap now exceeds any other measured social cleavage.1920 The pre-1945 fragmentation was ideological, but the post-war consolidation operated through institutions — labour unions, mainline churches, mass-circulation newspapers, civic associations — that had cross-cutting memberships and could absorb ideological difference. The contemporary equivalents are weaker by an order of magnitude, and the cross-cutting structure has eroded into mutually exclusive media and information environments.

Second, the K-shape. The top quintile of Millennials is on a Boomer-equivalent wealth trajectory; the bottom three quintiles trail historical cohort peers by approximately a decade on homeownership and net wealth, producing a cohort-level mobilisation capacity that is structurally split rather than consolidated.21 The post-1945 settlement consolidated because the GI cohort had a broadly shared economic trajectory: home ownership, union membership, defined-benefit pensions, a single-earner family wage that was achievable in the median. The Millennial cohort does not share that trajectory across its quintiles; the mobilisation capacity is concentrated at the top and frustrated at the bottom, which is not the configuration that produces a unified institutional rebuild.

Third, algorithmic personalisation. The information environment now segments the cohort along ideological lines before shared-narrative consolidation can form — a structural condition Vosoughi, Roy and Aral's diffusion data and Haidt's platform-architecture analysis document at scale.22 False information diffuses faster, deeper, and more broadly than true information on social-media platforms; the diffusion advantage is approximately 70% for false claims over true ones on Twitter's full population over a decade of data. This is a structural condition the post-1945 consolidation did not face.

None of these three conditions forecloses the regenerative path. They are friction, not foreclosure. The historical templates carry the empirical weight regardless of the friction. The Hero Generation's task is more structurally constrained than its GI analogue was, and the framework is sharpened, not abandoned, by naming that.

The honest reading: regenerative resolution is harder from the present starting position than from the 1933, 1945, or 1979 starting positions. The optimism is conditional on capacity for institutional assembly that the political-amplifier essays have shown to be at historical lows. That is the friction the templates need to be read against.

VII. The Structural Mechanism — Cumulative Knowledge and the Time-Price Frame

The Roser data describes what has happened. The structural account of why runs through two compounding mechanisms.

Time prices. The "time price" of a resource is the number of hours an average worker must work to purchase it — a unit that bypasses the PPP-conversion and purchasing-power debates that complicate nominal poverty data. Tupy and Pooley's analysis, drawing on wage and commodity price data across 1980–2018, finds the time price of a basket of basic commodities — food, energy, materials, basic services — has fallen by approximately 75% over the period.23 The median worker globally can purchase roughly four times as much basic goods per hour worked in 2018 as in 1980. The framework updates the Simon-Ehrlich wager at scale: Simon's 1980 bet with Paul Ehrlich that a basket of five commodities would be cheaper in real terms in 1990 than in 1980 was won by Simon; Tupy and Pooley extend the analysis across 50 commodities and 37 years with the same directional result. This essay uses the methodology and the directional finding; the surrounding political framing is not the manuscript's.

Cumulative knowledge. Innovation is exchange; exchange is the substrate of progress; specialisation enabled by trade — Adam Smith's insight at civilisational scale — is the causal engine of the long-arc capability expansion.24 Knowledge is cumulative in a way physical goods are not: knowledge can be shared without the original losing it, and the combination of ideas across specialists produces capabilities no individual specialist could reach alone. Writing, printing, the internet, vaccines, the global trade system itself — each is specialisation-via-exchange that expanded human capability beyond what pre-specialisation humanity was capable of, and each became a substrate on which the next round of specialisation was built.

The contemporary expression is the solar photovoltaic cost curve. Solar PV per watt has fallen from roughly $76/watt in 1977 to approximately $0.30–$0.40/watt in 2024 (Bloomberg NEF; IEA World Energy Outlook 2023/2024).25 A 99.5% decline over 47 years. Wright's Law — cost falling by a fixed percentage for every doubling of cumulative production — is the formalism underlying the observed decline, and solar PV is now among the best-documented examples in any industry. The curve is the cumulative-knowledge mechanism operating in real time on one of the most important inputs to Hickel's strongest argument: the transition to non-extractive energy production. It is the structural answer to the degrowth challenge — on a decade-scale rather than a year-scale, and one that does not, on its own, resolve the planetary-boundary question for the 2030s or 2040s. The near-term capacity-build bottleneck is real; the cost curve is real on the multi-decade arc; both are true.

A note on the source. Ridley's pre-2008 work included confident advocacy for financial-sector deregulation; he was a non-executive director of Northern Rock when it became the first British bank to suffer a public bank run in 150 years. The cumulative-knowledge framework can be intellectually genuine even when individual judgement-calls — including the framework's author's — miss badly. The structural argument does not depend on the author's reading of Northern Rock. The two are separate.

The capability stock is a stock, not a flow. It is what survives the financial-institutional reorganisation. Time-price compounding and cumulative knowledge are the structural reasons the long arc is the long arc.

VIII. Closing — What the Watch Window Produces

Apple Computer was founded in 1976. Home Depot was founded in 1978. Microsoft incorporated in 1975. The world's most valuable companies of the next forty-year cycle were born inside the structurally flat 1966–1982 nominal-return environment.

This is the load-bearing observation the closing argument is built on, and it is not a long-arc trend. It is a near-term operational fact about the kind of activity a structurally flat regime systematically produces — on the same calendar as the bear case, not on a 20-year horizon that has no bearing on a 2026 reader.

What kind of business gets started inside a structurally flat regime? On the historical record: businesses whose value compounds on the gap between what the capital markets are pricing and what the underlying capability stack can produce, businesses that do not need the cap-weighted index multiple to expand to make their first decade work, businesses founded by people who built operational discipline into the cost base because the wider environment was not subsidising margin. The 1975-to-1978 window did not produce these companies by accident. It produced them because a regime that is not paying for hype is a regime that disciplines what gets funded, what gets built, what survives the first three years, and what gets capitalised on by founders who could not have raised a price-of-perfection round if they wanted to. The same regime is what kills the businesses that depend on a 23× multiple holding. The two facts are the same fact.

What kind of institution gets rebuilt inside the resolution of a regime? On the historical record: institutions whose credibility has been repriced in the resolution itself, not in the lead-up to it. The Federal Deposit Insurance Corporation existed because the resolution forced it; Bretton Woods existed because the resolution forced it; the post-1979 monetary credibility was a property of the resolution, not its precondition. The institutional architecture the next cycle runs on is assembled in the years on either side of the crystallisation, not before it.

What kind of career gets compounded inside the watch window? On the historical record: careers built on the cost-base discipline the regime imposes, on the relationship capital that accrues to operators who keep their commitments through the resolution, on the cumulative-knowledge mechanism that does not switch off when financial conditions tighten. A 2026 thirty-five-year-old who is positioned to participate at the resolution is a 2046 fifty-five-year-old whose career compounded through the watch window the manuscript names. The capability stock that the long-arc data documents is not a property of the index. It is a property of the people who keep building inside the configuration that the bear case is the financial expression of.

This is the operational optimism the manuscript closes on. It is not a 20-year arc. It is a 2026–2030 observation about what the watch window structurally produces for the people who survive it intact — businesses founded inside the flat regime, institutions rebuilt through the resolution, careers compounded across the period the index goes nominally sideways. The post-resolution regime, when it arrives, runs on the architecture assembled in the resolution itself. Survival positioning is the precondition for being inside that architecture when it assembles.

What an honest reader is entitled to conclude

The manuscript is committed to its watch-window calendar. That is the falsifiable commitment Essay 13 names: the dashboard either reads the regime change inside 2026–2027 or it does not, and the manuscript is on the record either way. The position the closing block defends is that the calendar holds and the indicators will fire inside the window.

A reader who has worked through the manuscript and finds the bull-side rebuttals to the calendar more persuasive than the manuscript's replies is not outside the framework's diagnostic block. They are inside it on a different time-axis. The reading that holds the diagnostic block as broadly correct — the sovereign-fiscal arithmetic, the demographic reversal, the AI capex/revenue gap, the energy bottleneck, the political-amplifier diagnosis, the credit-fragility composite — but discounts the watch-window timing and runs the Opportunity Framework's structural reallocation on a longer horizon is a reading the manuscript is prepared to defend rather than to dismiss. The framework holds. The calendar is the falsifiable piece. The two-horizon discipline is what allows the reading to land in either configuration without breaking — but the manuscript's own emphasis lands on the calendar holding, and the dashboard is the apparatus by which that emphasis is honoured.

Two-horizon synthesis as the second-order frame

The two-horizon distinction sits underneath all of the above as the discipline that makes either reading executable. The bear regime is a property of the financial-institutional architecture. The long-arc optimism is a property of the human capability stock. The bear regime applies to the watch window; The Survival Framework is its architecture. The long-arc optimism applies to the multi-decade arc; The Opportunity Framework is the structural reallocation that participates in what the long arc produces. A financial-system crisis in 2027 does not reverse the trend in child mortality in Nigeria. Democratic backsliding in any specific national context does not reverse the long-arc decline in global illiteracy. The discipline of holding them cleanly is what separates this counterweight from a Pinker-style overreach in the optimist direction or a doom-coda in the bear direction.

The math is the math. The long-arc math and the bear-case math are not in contradiction; they are arithmetic on different time horizons. Position for the regime in front of you. Do not let the regime poison your view of the arc behind and ahead of it.

The bear regime applies to the watch window. The optimism applies to the multi-decade arc. Position accordingly. The distinction is not comfort.

Footnotes

-

Factfulness: Ten Reasons We're Wrong About the World — And Why Things Are Better Than You Think (Sceptre / Hodder & Stoughton, 2018). ↩

-

Our World in Data. The "awful / much better / much better" tripartite is from Roser's framing piece The world is awful. The world is much better. The world can be much better. (2022). ↩

-

UN Inter-agency Group for Child Mortality Estimation — Child Mortality Estimates. ↩

-

David Deutsch, The Beginning of Infinity: Explanations That Transform the World (Allen Lane / Viking, 2011). The "hard-to-vary" criterion is developed in Chapter 1. The "problems are inevitable" and "problems are soluble" formulations appear separately in Chapter 9 ("Optimism") rather than as a single contiguous sentence; the paired form has become canonical in secondary literature and Deutsch deploys both as paired principles in talks. Karl Popper's Conjectures and Refutations (Routledge, 1963) is the prior on which Deutsch builds. ↩

-

Less Is More: How Degrowth Will Save the World (William Heinemann / Penguin Random House, 2020). ↩

-

"Is global inequality getting better or worse? A critique of the World Bank's convergence narrative," Third World Quarterly 38, no. 10 (2017): 2208–2222. ↩

-

World Bank — Poverty and Shared Prosperity 2022: Correcting Course. ↩

-

"A safe operating space for humanity," Nature 461 (2009): 472–475. ↩

-

Neil Howe, The Fourth Turning Is Here: What the Seasons of History Tell Us About How and When This Crisis Will End (Simon & Schuster, 2023). ↩

-

Paul A. Volcker with Christine Harper, Keeping At It: The Quest for Sound Money and Good Government (PublicAffairs, 2018). ↩

-

V-Dem Institute, Democracy Report 2026: Unraveling The Democratic Era? — press release on US decline. University of Gothenburg. United States sub-indices on judicial constraints on the executive, media freedom, and freedom of expression all moved adversely in 2025; six of ten newly autocratising countries in Europe / North America; approximately 25% of nations in active backsliding. ↩

-

Shanto Iyengar and Sean J. Westwood, "Fear and Loathing Across Party Lines: New Evidence on Group Polarization," American Journal of Political Science 59, no. 3 (2015): 690–707. ↩

-

Federal Reserve Distributional Financial Accounts; IndexBox 2025 estimates $88.5T Boomer wealth; Motley Fool/DFA derived 54% equity share. ↩

-

Soroush Vosoughi, Deb Roy, Sinan Aral, "The spread of true and false news online," Science 359, no. 6380 (2018): 1146–1151. Roughly 126,000 verified rumour cascades on Twitter 2006–2017; six independent fact-checking organisations confirming classifications. Six-times-faster finding for false political news; bot-versus-human decomposition in the same paper. ↩

-

Superabundance: The Story of Population Growth, Innovation, and Human Flourishing on an Infinitely Bountiful Planet (Cato Institute Press, 2022). ↩

-

The Rational Optimist: How Prosperity Evolves (Fourth Estate / HarperCollins, 2010). ↩

-

Our World in Data — Solar Photovoltaic Module Prices (1976–present). ↩