The Democratic Trap

In 60 seconds

Democracies cannot reform before crisis because three preconditions have compounded: the median voter is too financially fragile to swallow short-term pain, the information environment now produces persuasive falsehood at $20 a month, and all five historical preconditions for successful pre-emptive reform (the Volcker-Reagan template) have independently eroded. Positioning for the consequences, not the rescue, is the only honest stance.

The diagnostic block ended with a configuration, not a forecast — and a question the configuration leaves open.

The Lens of History closed the manuscript's seven-essay diagnostic argument by showing that the present arrangement is recognisable in the historical record: Ferguson's Law breached in FY2024; Turchin's Political Stress Index at the 1850s level a decade ago, with the underlying instability prediction empirically validated since; the first synchronous developed-world working-age population peak in approximately six hundred years; G7 sovereign debt-to-GDP back at the only prior peacetime peak. The configuration is not unprecedented. It is, in the recognisable shape the historical record gives it, the configuration that precedes structural reorganisation. What the analogue does not tell the reader is which path through the constrained set the present configuration produces. That is decided, the essay argued, by decisions made under the configuration — not by the configuration itself.

The honest reader's next question is the one the diagnostic block has so far evaded. If the configuration is this visible, and the diagnostic this clean, why isn't anyone fixing it? The fiscal arithmetic is in every monthly Treasury statement. The equity-market valuation is in every Bloomberg terminal. The demographic curve is in every census release. The AI capex programme is in every hyperscaler 10-Q. The energy bottleneck is in every NERC reliability filing. None of these are hidden. None require unusual analytical sophistication to read. They sit, fully documented, in the public record of the institutions that compile public records. And the policy response to them is, across the board, an absence.

This essay is the answer to that question. It is the structural keystone of the manuscript's third movement — the political amplifier under the financial amplifier — and it argues that the absence of response is not an accident, not a failure of leadership, not a temporary dysfunction that will resolve when the right people are elected. It is the predictable equilibrium of three structurally compounding facts: a median voter too financially fragile to absorb short-term reform pain; an information environment whose marginal cost of persuasive falsehood has collapsed to roughly the price of a cheap dinner; and a set of historical conditions that enabled democratic course-correction in earlier episodes that have, across all five dimensions, independently eroded.

The argumentative spine, stated up front so the rest of the essay can be examined against it: democracies cannot fix their long-term problems before crisis; the system is therefore not in a position to be saved by its own institutional learning; positioning for the consequences, not the rescue, is the only honest stance.

Each of the three facts is documented separately in the empirical literature. The compounding is the contribution of this essay. The compounding is what produces the trap.

I. The Demand-Side Trap — The Fragile Voter

The opening insight is structural, not cultural. The median voter's discount rate on future welfare is a function of their financial position. The financial position of the median voter in a wealthy democracy in 2026 is, by the most careful measurement available, an arrangement under which roughly a third of all adult households cannot absorb a routine four-hundred-dollar shock.

The Federal Reserve's Survey of Household Economics and Decisionmaking (SHED) has measured this every year since 2013. The 2024 release (published May 2025) found that 32 percent of US adults could not cover a four-hundred-dollar emergency expense in cash or its equivalent.1 The 2013 baseline was 50 percent. The improvement is real. The persistence of the residual is the load-bearing fact. In a twelve-year window across an unbroken expansion, three rate cycles, two presidential transitions, and a pandemic, the share has not gone below thirty-two percent. The fragility is not evenly spread; among adults without a high school education the share falls below thirty percent; among Black households fifty-two; among adults aged eighteen to twenty-nine sixty-three; among non-metropolitan residents fifty-nine. The fragility is concentrated in cohorts whose vote, in any close election, is decisive.

A household one paycheque from disaster cannot afford to vote for harder now, easier later. Not because they are stupid, but because later does not exist for someone who cannot make rent next month. Reform platforms that ask for short-term sacrifice in exchange for long-term gain lose that comparison on instinct, before reasoning even starts. The household is making a survival calculation under constraint.

Pew Research's 2015 Politics of Financial Insecurity documented the political consequence directly.2 The most financially secure Americans were registered to vote at ninety-four percent; the least financially secure at fifty-four. Actual turnout in the 2014 midterms was sixty-nine percent among the most secure and thirty percent among the least. The voice of the financial precariat is not opposed at the ballot box. It is largely absent from it. The median voter is drawn from the financially secure top, not the financially fragile bottom.

That fact would seem to argue against the trap. The reason it does not produce reform is the second part of the mechanism. The financially secure voter, in a polity with a fragile bottom third, votes against any reform whose first-order effect is to make the bottom third visibly worse. Loss aversion does the analytical work. Kahneman and Tversky's Prospect Theory established that losses loom psychologically about twice as powerful as equivalent gains. Layer the concreteness asymmetry on top: short-term pain is concrete (the petrol bill, the pension cut, the factory closing); long-term gain is abstract and statistical. Voters are comparing a vivid wound to an actuarial whisper. The Alesina et al. NBER working paper on loss aversion in politics formalised what the literature had been documenting for decades: under loss-averse preferences, a mass of voters votes for the status quo even when their rationally preferred policy differs from it.3

A causal piece of evidence locks the mechanism in place. A 2025 Federal Reserve Bank of Dallas working paper by Liu, McCartney, Ramcharan, Zhang and Zhang exploited the eligibility discontinuity in the Home Affordable Refinance Program during the Great Recession to identify the causal effect of household financial relief on political participation.4 Borrowers who refinanced between 2009 and 2012 were measurably more likely to vote in the 2012 general election than otherwise-similar borrowers who did not refinance. The increase in turnout was concentrated among households that received the largest payment reductions, and concentrated among independents rather than partisan loyalists. The authors' conclusion is the load-bearing one: "policy-induced mortgage relief can extend beyond household balance sheets into the political sphere." Financial relief causally produces political participation. Financial fragility causally suppresses it. The relationship is not correlational. It is identified.

The structural anchor for what the fragility produces is Mancur Olson's distributional-coalitions mechanism (The Rise and Decline of Nations, 1982; never substantively refuted in the public-choice literature since).5 Stable societies accumulate, over decades, small organised groups extracting concentrated benefits against dispersed costs — tariffs, occupational licensing, regulatory exemptions, agricultural subsidies, tax expenditures, entitlement carve-outs. Benefits concentrated enough to make organisation rational; costs dispersed enough to make individual opposition irrational. The longer a democracy is stable, the more sclerotic it becomes; the more sclerotic, the harder reform gets — not by design, but because the cumulative weight of small organised interests has set the political price of any change asymmetrically high.

Achen and Bartels's Democracy for Realists (2016) is the empirical voter anchor.6 Their central claim is that voters do engage in retrospective voting, but cannot distinguish between government actions, environmental shocks, and pure luck. They punish incumbents for outcomes incumbents do not control, as long as some culturally plausible narrative connects the incumbent to the pain. "Election outcomes are mostly just erratic reflections of the current balance of partisan loyalties in a given political system," Achen and Bartels write — the formulation appears in Chapter 1 of Democracy for Realists, page 16, previewing the synthesis the economic-voting machinery of Chapter 6 ("Musical Chairs: Economic Voting and the Specious Present") then demonstrates. In their analysis of state-level vote shares from 1900 to the present, droughts and floods cost the incumbent party 0.7 percentage points in vote share in a typical state and year, with extreme weather episodes costing 1.5 percentage points. The implication for reform is brutal. A government that delivers short-term pain will be punished for the pain regardless of whether the pain produces the long-term gain. Voters do not have the mechanism for the disaggregation. Achen and Bartels call it blind retrospection, and the empirical record they assemble for it across a century of American elections is one of the most thoroughly documented findings in political science.

The doom loop closes here. Fragile voters with compressed time horizons. Secure voters with loss-averse preferences. An organised coalition of beneficiaries of every existing arrangement. An empirical voter who cannot distinguish reform pain from luck pain and punishes the incumbent for both. Can-kicking platforms win. Debt and entitlements compound. Next cycle's fragility deepens. Discount rates compress further. The next cycle's reform window is narrower than the last.

This is not a moral failing of the electorate. It is the predictable equilibrium of a system in which the median voter — across both the fragility cohort and the loss-averse cohort — is too close to the margin to afford the future.

A counter is honest to engage. Bryan Caplan's The Myth of the Rational Voter (2007) argued voters hold systematic anti-market, anti-foreign, make-work, and pessimistic biases against the consensus of professional economists;7 the essay defers to Achen-Bartels because the voter-fragility case does not require irrationality, only that voters be rationally responsive to a structurally compressed time horizon — a lower analytical bar the SHED data clears.

II. The Supply-Side Trap — The Corrupted Information Environment

If the demand-side trap explains why financially fragile voters cannot afford long-term thinking, the supply-side trap explains why even the voters who could afford it now navigate an information environment that has lost the scaffolding the previous generation could rely on. These are not separate failures. They compound multiplicatively.

Information manipulation has always existed. What is new is not the manipulation; it is the cost. NewsGuard's AI Tracking Center has logged the AI-generated content-farm count from 49 in May 2023 to 1,121 by November 2024 to 3,006 by March 2026 across sixteen languages.8 The headline factor-of-sixty growth figure is best read as a directional claim about the cost curve. NewsGuard's analysts have produced a working AI content farm site for one hundred and five US dollars in marginal cost. Producing ten thousand personalised persuasive messages used to require a state propaganda apparatus or a billionaire publisher. It now requires a twenty-dollar-a-month subscription. Persuasion has been democratised — but to bad actors, not to citizens.

This is a difference in kind. The new AI-generated content does not replace the legitimate journalistic infrastructure. It is added to it. The baseline of legitimate reporting still exists; what is new is that it now sits inside a content environment whose volume of plausibly-presented falsehood has grown materially across three years and continues to compound.

The transmission, on Vosoughi, Roy and Aral's 2018 Science paper analysing 126,000 verified rumour cascades, runs at six times the speed of truth, ten times the reach, ten layers deeper — with the effect strongest for political content, and not bot-driven (humans spread the falsehood).9 AI-generated content is optimised by the engagement-maximising loss function for the same fitness function, at a marginal-cost structure legitimate journalism cannot match.

The cross-essay link is exact. The End of the Bull Run argued that the marginal price-setter in equity markets is no longer the informed value investor; it is an algorithm executing passive-flow rules indifferent to underlying valuation. The marginal narrative-setter in democratic discourse is no longer the informed citizen; it is an algorithm — engagement-maximising recommendation compounded by the AI-generation cost-curve collapse — indifferent to the underlying truth of any signal. The two mechanical replacements are happening at roughly the same time, in the same regime, for structurally analogous reasons.

The other half of the corruption is the asymmetry Chesney and Citron named in their 2019 California Law Review article.10 The Liar's Dividend runs in both directions: "deep fakes make it easier for liars to avoid accountability for things that are in fact true." Bad actors gain offensively (they can fabricate) and defensively (they can dismiss authentic recordings as fabrication). The Brennan Center's 2024 documentation includes a Spanish foreign minister dismissing photographic evidence of police violence as "fake photos"; the Detroit mayor dismissing audio recordings later confirmed authentic; an Indian politician dismissing as AI-generated a recording subsequently confirmed real; defence counsel for a January 6 Capitol-riot defendant arguing audiovisual evidence was deepfaked.11 Producing a plausible deepfake takes seconds; debunking one takes hours; the debunk reaches a tenth of the audience. The epistemic floor is the casualty.

DiResta's Invisible Rulers (2024)12 names the result: bespoke realities — custom-made informational worlds tailored to individual audience members, generated on demand. Deepfaked endorsements, fabricated quotes, AI-generated "experts" with plausible credentials and no underlying person. "If you make it trend, you make it true." Cambridge Analytica was crude and pre-LLM. The current model is millions of messages to one voter at a time.

The scaffolding has collapsed in parallel. The Stanford History Education Group's 2016 study (replicated 2019 and 2022 with no significant improvement) found 93% of college students could not identify "MinimumWage.com" as a corporate lobbying front.13 Northwestern's 2025 State of Local News documents that nearly 40% of US local newspapers have vanished in two decades, with roughly fifty million Americans now in limited or no-access news deserts.14 The information substrate that made informed civic participation feasible — local newsrooms with institutional memory, civic education with epistemic content, slower information cycles — has thinned simultaneously with the AI-content compounding.

The strongest counter is Schneier and Sanders's Harvard Ash Center post-mortem — "The dreaded 'death of truth' has not materialized — at least, not due to AI"15 — alongside the GMF Spitting Images tracker logging 133 deepfakes across roughly sixty 2024 elections, a small absolute number.16 The structural claim is not that AI swung the 2024 cycle. It is that the information environment within which any future reform platform must compete has lost the scaffolding earlier reform platforms relied on. The 2024 cycle was the warm-up: relatively transparent deepfakes, slow LLM generation, weak personalisation tooling. The cost curve continues to collapse. The window in which any reform platform might still be communicated through an information environment that resembles the one Volcker spoke into is closing.

III. Why This Generation Is Different — The Five Conditions, Eroded

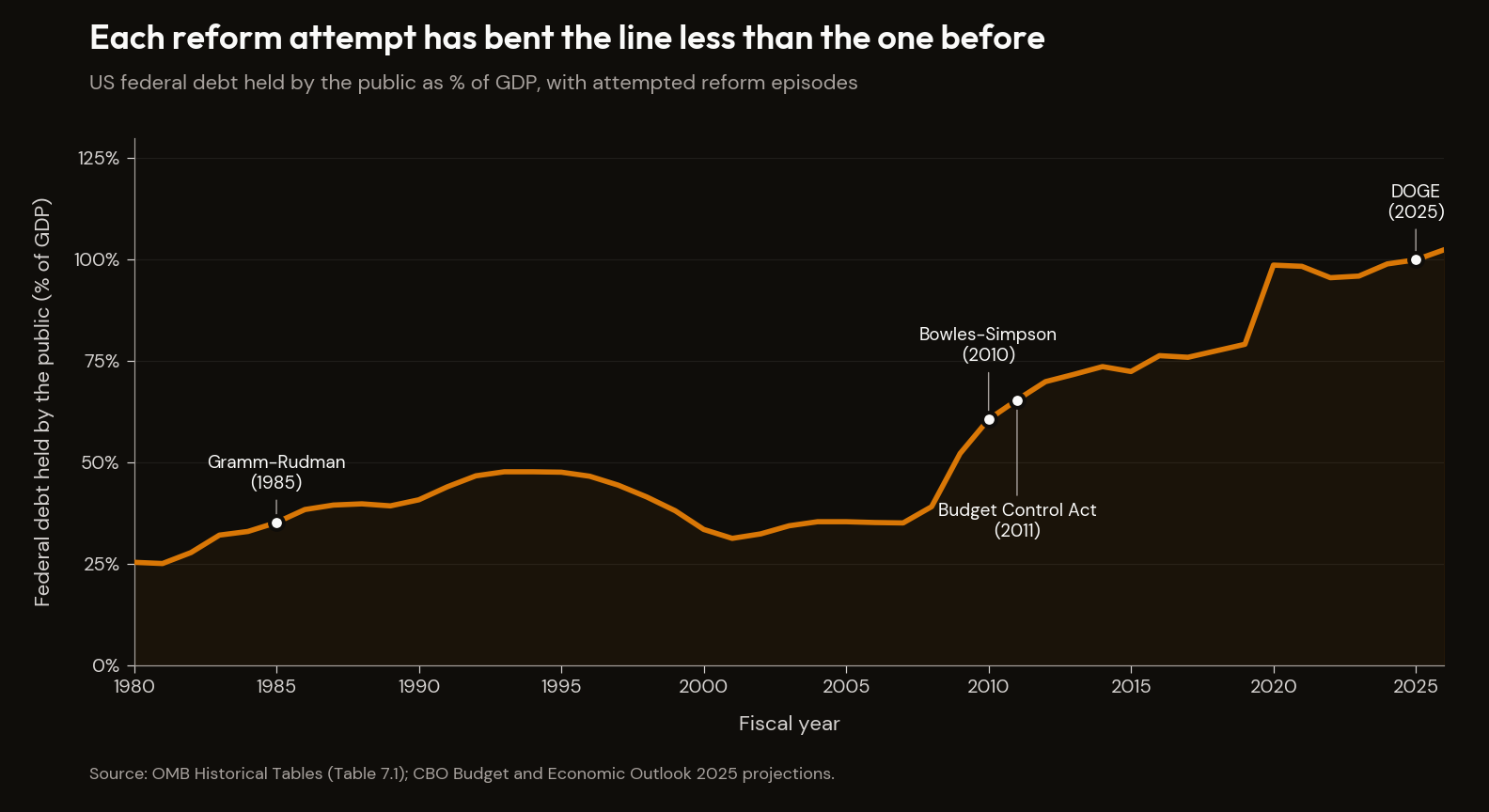

History does not produce reform platforms that voters love in the moment. It produces reform platforms voters tolerate because the alternative is worse, conducted under specific conditions, by leaders who chose to spend political capital they could have hoarded. The historical record across the five most-cited postwar reform episodes — Volcker-Reagan, Hawke-Keating, Rogernomics, Laar's Estonian shock therapy, Erhard's West German currency reform — shows a recognisable set of enabling conditions. Successful structural reform required at least three of five: an acute double-digit crisis; technocratic insulation politically protected by the executive; cross-party elite consensus on what the crisis required; organised labour either accommodating the reform or absent as a blocking constituency; and a narrative cover backed by rapid visible recovery before the next election cycle.

The structural argument is that all five conditions, in 2026, have been independently eroded — not by design but as the cumulative product of changes happening for unrelated reasons that compound to remove the institutional substrate prior reforms depended on. The five conditions were not separable in the prior reforms; they reinforced each other. The erosion is also not separable.

Volcker delivered, between August 1979 and June 1981, the most severe monetary contraction since the Great Depression. The Federal Funds rate rose from an 11% average in 1979 to 19.1% in June 1981. Inflation fell from 14.8% in March 1980 to 3.8% by December 1982. Unemployment reached 10.8% in November 1982 — the highest since 1940.17 Volcker's own framing of the October 1979 decision is unambiguous: "it was time to act — to send a convincing message to the markets and to the public."18 The reception was tangible: "Farmers once surrounded the Fed's Washington building with tractors. Home builders, forced to shut down, sent sawed-off two-by-fours with messages to the Federal Reserve Board."18 The political pressure was organised, and absorbed.

Reagan won re-election in November 1984 by 525 electoral votes to thirteen despite presiding over the deepest postwar recession in his first term. He won because all five historical conditions were simultaneously present. The crisis was acute and double-digit. The Fed was technocratically insulated and politically protected: Reagan reappointed Volcker in June 1983, when the political case for sacking him was overwhelming and Volcker was a Democrat. Reagan made the choice anyway. Cross-party consensus was real: both parties agreed inflation was the existential threat. Organised labour did not accommodate the reform but was not strong enough to block it. The narrative cover was Morning in America, backed by rapid visible recovery: unemployment fell from 10.8 percent in November 1982 to 7.2 percent by election day November 1984. Voters saw the trajectory, not the trough. Recovery before the election was the precondition for political survival of the reform.

This is the historical exception that defines the rule. The five enabling conditions were present simultaneously. They are not now.

Hawke-Keating delivered Australia's structural reform on a different model — the Accord, 1983–1996 — through the Australian Council of Trade Unions, a peak confederation representing close to 40 percent of the workforce, capable of delivering cross-class wage restraint in exchange for guaranteed welfare expansion and superannuation extension. The mechanism required labour strong enough to block reform if it wanted to, and organised enough to deliver compliance if it agreed. US private-sector unionisation in 2026 is 10.1 percent, down from 35 percent in 1955; UK density is similar. There is no peak confederation capable of an Accord-style bargain. Labour is too weak to negotiate, too fragmented to be absent.

Rogernomics is the negative case: cabinet control, speed before opposition, an electoral mandate; none of the other four conditions. The reforms passed; the political coalition that delivered them collapsed at the next election. Erhard's 1948 currency reform required Allied occupation; Estonia's 1990s shock therapy required the Soviet state's collapse and an institutional vacuum. Neither is replicable inside a stable polarised democracy with mature interest-group structures.

The 2026 baseline weakens each of the five conditions. The crisis is slow-motion — a 0.5 percent annual debt-to-GDP increment, a 0.1 percent annual working-age decline, a 1 percent annual capex outrun on AI — none of which flags the political-decision threshold 14.8 percent inflation did. Technocratic insulation is contested. Cross-party consensus on the diagnostic, let alone the treatment, does not exist. The narrative cover assumes a unified information environment that the AI-content cost-curve collapse has already removed.

The condition-by-condition reading, compressed:

| Precondition for the Volcker template | Volcker-Reagan era (1979–86) | Current state (2026) | Status |

|---|---|---|---|

| 1. Cross-partisan elite consensus on the problem | Yes (Carter appointment + Reagan reappointment delivered continuity) | Fragmented within both parties — diagnosis disputed, entitlements untouchable | Partially eroded — consensus exists in fragments but does not aggregate to the cross-party floor Volcker had |

| 2. Median voter able to absorb short-term pain | Households had buffer; 70s inflation made cost legible | Median household cannot cover $1,000 emergency | Eroded |

| 3. Information environment with shared facts | Three networks, common evening news (contested at the time — Watergate-era trust was itself a product of recent collapse from 1964 highs) | Persuasive falsehood at $20/month; algorithmic personalisation | Eroded — the 1979 baseline itself was a lower bar than the retrospective lionisation suggests |

| 4. Institutional capacity (Fed independence, civil-service competence) | Fed independence intact; civil-service institutional memory deep | Fed independence contested; ~1/8 federal workforce reduction; DOJ contested | Eroded |

| 5. Sovereign fiscal room for transition costs | Debt/GDP ~33%; deficit small | Debt/GDP ~100%; deficit ~$2T/yr | Eroded |

The information-environment erosion adds a fifth dimension to the §II diagnosis: not only has the scaffolding of trusted journalism thinned and the marginal cost of persuasive falsehood collapsed — the speed at which falsehood propagates has crossed a threshold that the error-correction mechanisms the prior reform episodes relied on cannot match. Decentralised error-correction (Ridley's Evolution of Everything, developed later in this manuscript by The Case for Optimism)19 holds only when the correction loop runs faster than the propagation loop; at digital network speeds, that condition can fail.

The failed reform attempts of the past two decades confirm the structural case:

| Attempt | Year | Outcome | What this tells us |

|---|---|---|---|

| Bush Social Security privatisation | 2005 | Withdrawn within 6 months | Even within-party majority insufficient |

| Simpson-Bowles Commission | 2010 | Recommendations shelved | Bipartisan elite consensus insufficient without electoral cover |

| ECB Greek bailout terms | 2010–15 | Required external compulsion | Sovereign reform under acute crisis, not pre-emptive |

| Macron pension reform | 2023 | Passed via Article 49.3 (without vote); ongoing political cost | Reform possible but at high political cost; demographic baseline irreversible |

| UK 2022 mini-budget | 2022 | Reversed within 44 days | Market discipline can force reversal; not the same as pre-emptive reform |

Sweden in the 1990s is the strongest counter — an acute currency crisis (Riksbank defending the krona at 500 percent overnight rates in 1992), decisive fiscal consolidation, world-leading pension reform with automatic stabilisers. Two conditions present (acute crisis; corporatist consensus) in a small homogeneous polity with deep corporatist institutions and an EU-Maastricht external constraint that mattered. Sweden is not a model for large polarised democracies, and by 2026 even Sweden's consensus-corporatist model faces challenge from immigration politics. Where the conditions exist, reform works; where they erode, it does not.

South Africa is the clinical extreme — the limiting case SA & Africa documented. A median voter so financially fragile that even mild structural reform is electorally suicidal; a dominant political party plus a fractured opposition that removes the cross-party escape hatch; an information environment in which state-funded narratives propagate without effective counterweight. The five conditions are not weakened in South Africa. They are absent. The country is what the trap looks like when it has been allowed to run for thirty years.

IV. Prescription, Honest

The diagnostic of the trap is brutally strong. The prescription must not over-claim. The mechanisms most often proposed all empirically operate as scaffolding that requires prior political consensus — which is precisely what the trap removes.

Begin with independent fiscal councils — OBR, Sweden's Fiscal Policy Council, the Netherlands' CPB, Chile's Autonomous Fiscal Council, the US CBO. Beetsma and Debrun's IMF evaluation finds councils magnify the reputational cost of rule-breaking but cannot enforce compliance when political incentives diverge.20 The canonical failure case is the UK in September 2022: the Truss Growth Plan announced £45 billion of unfunded tax cuts without requesting an OBR forecast.21 The OBR could not compel a forecast; the market did the disciplining the OBR could not. Italy and France have repeatedly broken Stability and Growth Pact commitments without meaningful enforcement.

Citizens' assemblies are the second fix. Ireland's 2016–18 assembly is the success case (abortion referendum at 66.4% approval; partial climate implementation).22 France's 2019–20 Convention Citoyenne is the failure: 149 recommendations, 53% rejected outright, no binding implementation, Macron personally vetoing the dividend tax before parliament voted.23 The OECD's 2020 review of approximately 300 deliberative practices is consistent: assemblies work on discrete high-salience single issues; they fail on compound long-term tradeoffs.24 Sortition is a tool for one decision. The trap requires hundreds.

Compulsory voting on the Australian model pulls turnout to roughly 90 percent but has not prevented fiscal short-termism, climate underinvestment, or housing-policy capture; it changes who votes, not politician behaviour facing loss-averse voters and distributional coalitions. Central-bank independence works only where rule of law is already robust, and post-2008 QE demonstrated independence can be circumvented by policy redefinition.25 Information-environment reform — the EU DSA, public-service media support — is partial, contested, and politically deadlocked in the United States, where Section 230 reform has stalled for a decade; Ofcom's 2024 review finds a 15–20 percentage-point correlation between strong PSM and citizen political knowledge and institutional trust, the only mechanism with durable independent empirical support.26

All six mechanisms assume institutional rules constrain behaviour absent political consensus. The empirical record reverses this: rules persist only given prior political consensus. They are complements to political will, not substitutes. None pass the political bar before crisis arrives.

The second layer is catalytic. Reform windows are narrow and reactive. The Volcker-Reagan template required building the technocratic capacity and narrative scaffolding before the window opened. The honest prescriptive move is to argue for that pre-positioning now, in calm: assemble the technocratic capacity, build cross-party elite consensus on what the structural problems are (separately from what the solutions are), pre-stage the narrative scaffolding. The 2026–2027 watch window is the timing constraint. If the reform window opens in 2027 or 2028 and the technocratic capacity has not been pre-positioned, the window closes before the institutional response can land.

The third layer is personal, and it is the one this manuscript points its later essays at. Do not bet your life on the system fixing itself in time. Position for the consequences, not the rescue. Cultivate optionality — geographic, financial, career, jurisdictional. The orderly hegemonic transition Britain executed between 1922 and 1956 was not orderly for most British households. Survivors of the prior comparable configurations did not, on average, navigate them by waiting for the political system to deliver the rescue.

The objection that this view "justifies disengagement" is serious and must not be ducked. Three of the five historical conditions can be partially rebuilt before crisis: cross-party elite consensus on what the structural problems are; technocratic capacity ready to be deployed; narrative scaffolding pre-built. The catalytic layer is explicitly about preparing for the reform window, not denying it can open. Distinguishing pre-positioning from rescue is the move. The further objection that conditions have always been hard to assemble is partial: all five eroding simultaneously is new. The cost curve of persuasive falsehood has collapsed in a way unprecedented in industrial-democracy history. US private-sector unionisation at 10.1 percent is qualitatively different from the 35 percent baseline that enabled the Accord. The argument is not that no reform episode has ever occurred under any subset of the conditions; it is that all five eroding at once is the regime change.

V. The Trap as Diagnostic Glue

The diagnostic essays of this manuscript catalogued the problems — fiscal arithmetic, equity valuations, demographic reversal, mag-seven concentration, the AI capex / productivity-ceiling forced choice, the energy bottleneck, the historical analogue. Egos and Ideology catalogued the political symptoms the trap structurally produces — populist backlash, institutional backsliding, polarisation feedback loop. This essay names the structural mechanism that explains why the diagnostic catalogue is not being acted on, and why the political-symptom catalogue is the predictable equilibrium rather than the contingent breakdown.

What cannot be fixed eventually breaks. Phase transitions are readable.

The italicised closing claim, in the form the argument has earned: democracies cannot fix their long-term problems before crisis; the system is therefore not in a position to be saved by its own institutional learning; positioning for the consequences, not the rescue, is the only honest stance.

The trap is why the system that diagnosed the math will not, in the time available, deliver the timing.

Footnotes

-

Federal Reserve SHED 2024 — Economic Well-Being of US Households. ↩

-

Pew Research — The Politics of Financial Insecurity: A Democratic Tilt Undercut by Low Participation (January 2015). ↩

-

Alesina, Passarelli, et al., Loss Aversion in Politics, NBER Working Paper 21077 (2015). ↩

-

Liu, McCartney, Ramcharan, Zhang & Zhang, Household Finance Shapes Political Participation: Evidence from Mortgage Refinancing, Federal Reserve Bank of Dallas Working Paper 2517 (May 2025, revised March 2026). ↩

-

Mancur Olson, The Rise and Decline of Nations: Economic Growth, Stagflation, and Social Rigidities (Yale University Press, 1982). ↩

-

Christopher H. Achen and Larry M. Bartels, Democracy for Realists: Why Elections Do Not Produce Responsive Government (Princeton University Press, 2016). The "erratic reflections" formulation appears in Chapter 1 ("Democratic Ideals and Realities"), p. 16, previewing the synthesis Chapter 6 ("Musical Chairs: Economic Voting and the Specious Present") then demonstrates. ↩

-

Bryan Caplan, The Myth of the Rational Voter: Why Democracies Choose Bad Policies (Princeton University Press, 2007). ↩

-

Soroush Vosoughi, Deb Roy, Sinan Aral, "The spread of true and false news online," Science 359, no. 6380 (2018): 1146–1151. Roughly 126,000 verified rumour cascades on Twitter 2006–2017; six independent fact-checking organisations confirming classifications. Six-times-faster finding for false political news; bot-versus-human decomposition in the same paper. ↩

-

Bobby Chesney and Danielle Citron, "Deep Fakes: A Looming Challenge for Privacy, Democracy, and National Security," California Law Review 107, no. 6 (2019): 1753–1820. ↩

-

Goldstein & Lohn, Deepfakes, Elections, and Shrinking the Liar's Dividend (Brennan Center for Justice, January 2024). ↩

-

Renée DiResta, Invisible Rulers: The People Who Turn Lies into Reality (PublicAffairs, 2024). "If you make it trend, you make it true" — operating maxim of the book; phrase first appears as the title of DiResta's October 2018 Yale Review essay. ↩

-

Stanford History Education Group, Evaluating Information: The Cornerstone of Civic Online Reasoning (November 2016). ↩

-

Northwestern University Local News Initiative, Medill School of Journalism, State of Local News 2025 Report. ↩

-

Bruce Schneier and Nathan Sanders, The apocalypse that wasn't: AI was everywhere in 2024's elections, but deepfakes and misinformation were only part of the picture (Ash Center for Democratic Governance, Harvard Kennedy School, December 2024). ↩

-

German Marshall Fund — Spitting Images: Tracking Deepfakes and Generative AI in Elections. ↩

-

Paul A. Volcker with Christine Harper, Keeping At It: The Quest for Sound Money and Good Government (PublicAffairs, 2018). ↩ ↩2

-

Matt Ridley, The Evolution of Everything: How New Ideas Emerge (Harper, 2015). HarperCollins. ↩

-

Roel M.W.J. Beetsma and Xavier Debrun, Fiscal Councils: Rationale and Effectiveness, IMF Working Paper WP/16/86 (2016). ↩

-

Institute for Government, Blocking OBR Forecasts Undermines the Credibility of Liz Truss's Economic Plans (September 2022). ↩

-

Citizens' Assembly Ireland — Reports and Recommendations (2016–2018). ↩

-

Averchenkova, Koehl, and Smith, Policy Impact of the French Citizens' Convention for the Climate: Untangling the Fate of the Citizens' Recommendations (LSE Grantham Research Institute, 2025). ↩

-

OECD, Innovative Citizen Participation and New Democratic Institutions: Catching the Deliberative Wave (2020). ↩

-

Acemoglu, Johnson, Querubin, and Robinson, When Does Policy Reform Work? The Case of Central Bank Independence, NBER Working Paper 14033 (2008). ↩