The Lens of History

In 60 seconds

The diagnostic block describes a configuration that looks unprecedented against the 70-year post-1945 base rate but is recognisable in the longer historical record. Ferguson's Law (net interest > defence) was breached in FY2024; Turchin's political-stress index hit pre-Civil-War levels in 2012; G7 sovereign debt sits at peacetime peak. The historical analogue does not forecast the resolution. It constrains the set.

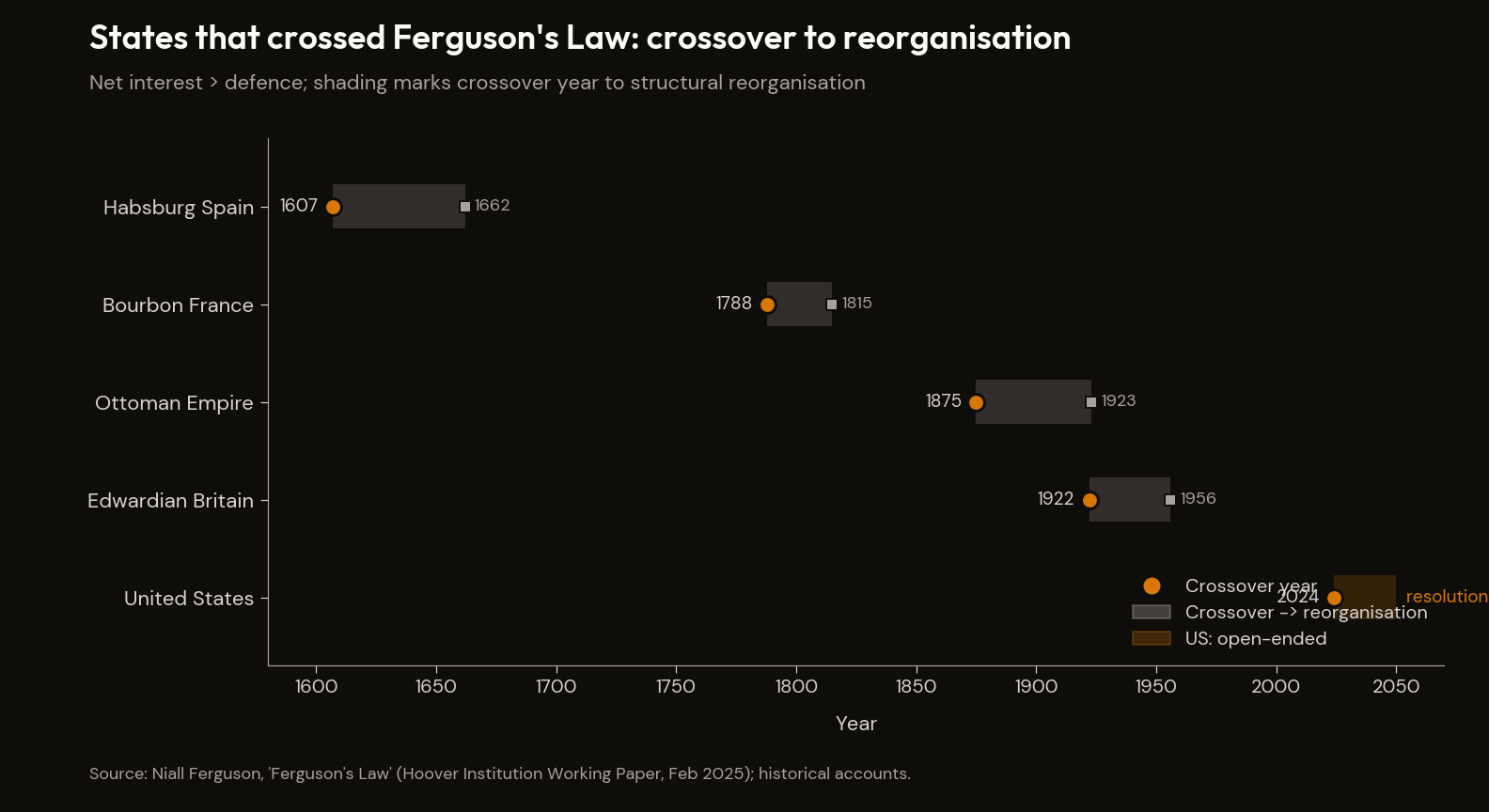

In fiscal year 2024, the United States federal government paid $881 billion in net interest on its debt and $874 billion on national defence.1 The crossover is small in dollars and large in meaning — the first time the US has spent more on debt service than on the armed forces in nearly a century. The previous comparable episode was the 1930s, with a brief reading in the post-1918 demobilisation. The line is named — Ferguson's Law — and the historical record of states that have crossed it is short, well-documented, and consistent.2

"Any great power that spends more on debt servicing than on defense risks ceasing to be a great power. … This is because the debt burden draws scarce resources towards itself, reducing the amount available for national security, and leaving the power increasingly vulnerable to military challenge." — Niall Ferguson, "Ferguson's Law: Debt Service, Military Spending, and the Fiscal Limits of Power", Hoover Institution Working Paper 202502, February 20252

The diagnostic block argued the post-2008 financial system is structurally broken on its own arithmetic. The natural next question is whether the configuration is unprecedented. The reader's implicit base rate is the post-1945 American era: roughly seventy years of reserve-currency status, a demographic dividend, and non-binding energy. Inside that base rate, the configuration is unprecedented. Outside it, in the broader 2,000-year historical record, it is not.

Three anchors — Ferguson's Law, Turchin's Political Stress Index, and G7 sovereign debt at peacetime peak — are the same moment seen from three vantages. The historical analogue does not forecast the resolution; it constrains the set. What the diagnostic block has been describing is not a system breaking in unprecedented ways. It is a system breaking in the way the historical record has always shown systems break before they reset.

I. Why History Matters Here

The post-1945 American era is the only era most working market participants have been alive for, the only era for which complete and reliable financial data exists, the only era in which the institutions that frame the discussion — the IMF, the World Bank, the Federal Reserve in its modern form, the post-Bretton Woods dollar regime — have been operating. Inflation regimes, currency reserve status, equity-market valuations, demographic structures, fiscal arithmetic — all have been measured against a seventy-year window in which the United States has been the structurally privileged hegemon.

The configuration the diagnostic block describes — debt at peacetime peak, working-age population in decline, productivity gains contested, capital concentrated, political legitimacy under measurable stress — is rare in the post-1945 record because that record covers only one country's structural ascent and the orderly hegemonic period that followed. It is common in the broader historical record, appearing with reasonable consistency at the late stage of every major systemic regime since the Reformation. Each case has its own contingent causes, and a serious historian will be impatient with any reading that flattens them. The structural commonality is not the contingencies. It is the configuration.

This is not a prediction. It is a relocation of the prior. The right base rate is two thousand years, not seventy.

II. Ferguson's Law and the Empire-Decline Pattern

The naming is Niall Ferguson's, in a February 2025 Hoover Institution working paper.2 Ferguson is a divisive citation in academic circles, and the discipline here is to use him for the named-law datapoint and the historical-pattern observation, not for his contemporary commentary.

The empirical line was crossed in FY2024 at net interest $881B vs defence $874B.1 Net interest as a share of GDP is approaching the 1991 post-WWII peak of 3.2% (FY2024 reading: 3.1%). FY2025 is projected at roughly $970B in net interest against $917B in defence; FY2026 year-to-date has net interest annualising above $1 trillion.3 The crossover is the new baseline, not a one-year curiosity.

The historical record on what happens to states that cross the line is short and consistent. Bourbon France's royal debt service overran military spending by the late 1780s; the regime was finished within four years, continental hegemony within twenty. The Ottoman 1875 default and 1881 Public Debt Administration transferred fiscal sovereignty to a European-creditor consortium; territorial fragmentation followed within a generation. Edwardian Britain abandoned the Two-Power Standard at the 1922 Washington Naval Treaty because the Treasury could not finance both debt service and the fleet; the imperial position was structurally finished by Suez 1956, when the US vetoed the Anglo-French intervention by withholding sterling support. Habsburg Spain's declining silver flows against fixed military commitments produced five sovereign defaults between 1607 and 1662. In each case, when the fiscal arithmetic forced the choice between debt service and force projection, the system reorganised — and the reorganisations, though not identical, were recognisable: currency loses reserve status, hegemonic position erodes, next system organises around a different anchor.

The United States crossed the line in FY2024. Ferguson's framing on this narrow empirical point is that the law is not deterministic: states that cross the line risk ceasing to be great powers when other variables compound. The reader knows what those look like in the present configuration. The demographic curve is reversing. The productivity offset is too small. The energy infrastructure cannot be built on the capex cycle's timeline. The political-cohesion variables are deteriorating on their own measures. The variables that historically determine whether the risk is realised are not, on present trend, running in the direction of mitigation.

The obvious counter is that Britain ran above Ferguson's Law for most of the nineteenth century and remained the global hegemon. The counter has force as a constraint on the claim's strength, not as a refutation of it. Pre-1914 Britain serviced its debt from a unique hegemonic position — undisputed reserve-currency status, an empire generating remittance and tribute flows, and a Royal Navy whose Two-Power Standard was financed against a tax base that other powers could not match. The 1922 Washington Naval Treaty is the moment the structure stopped working: the Treasury could no longer fund both debt service and the fleet on the post-war debt load, the Two-Power Standard was abandoned, and sterling lost reserve status across the next thirty years to a power that had crossed Britain on the underlying fiscal arithmetic in the opposite direction. The pre-1914 above-Ferguson record was sustained by a hegemonic position the United States in 2026 does not have; the post-1922 sterling experience is the analogue the present configuration sits closer to. The "Britain ran above the line and was fine" reading is the pre-1914 half of the British case; the post-1922 half is what the line crossing actually looked like once the hegemonic buffer was gone.

The implication is narrower than "the US is Bourbon France": the US is now in the configuration historical states have entered before they reorganised. The historical record does not say what reorganisation looks like in this case. It says only that the set is bounded and recognisable.

III. Elite Overproduction and the Validated Prediction

A peer-reviewed quantitative model of political instability, published in 2010, made a specific decade-scale prediction that subsequent events validated — the closest available empirical refutation of the standard objection that cycle theories are post-hoc rationalisation.

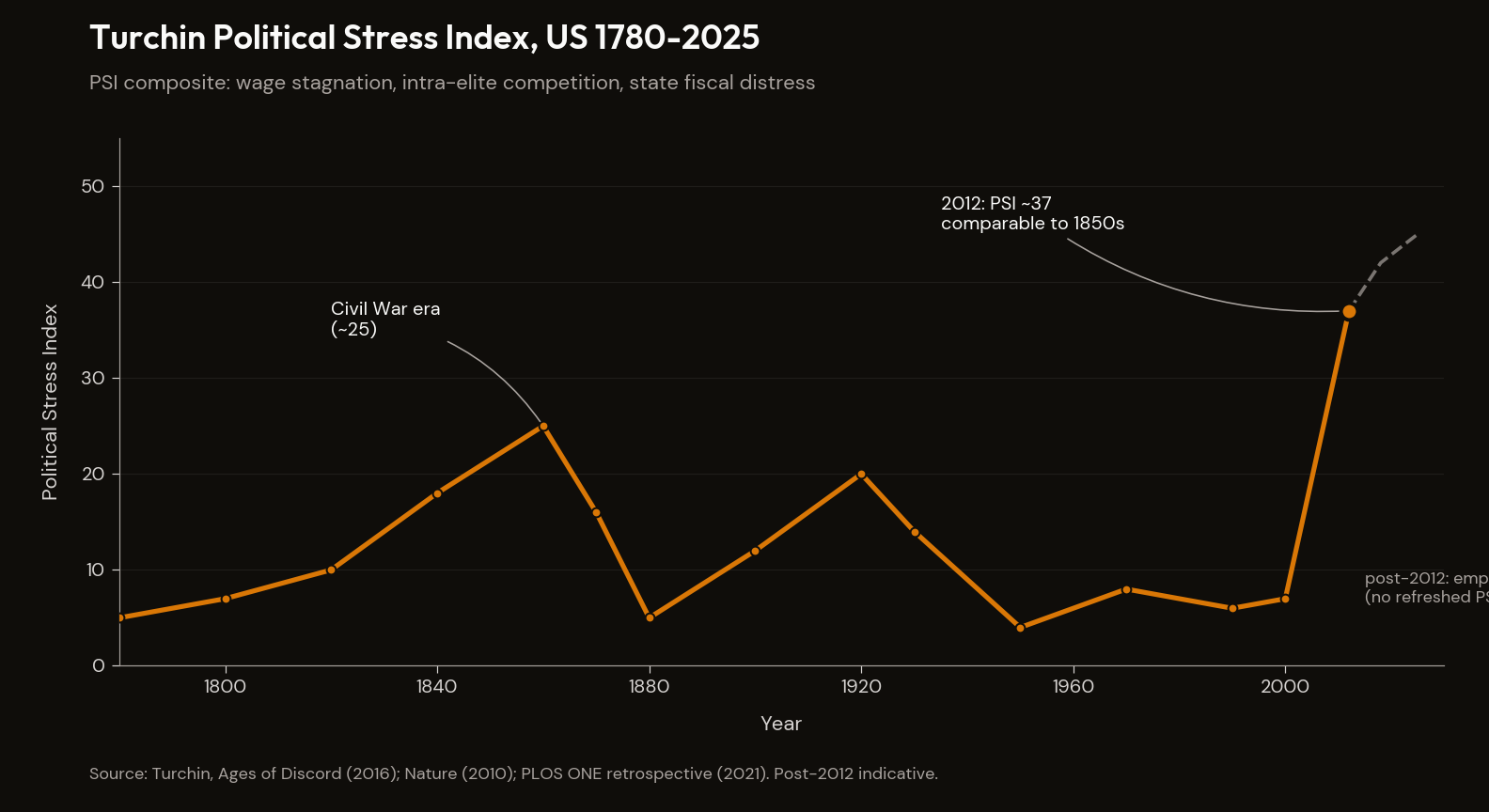

Peter Turchin's 2010 Nature paper predicted that the year 2020 would mark the peak of a roughly fifteen-year-long instability cycle in the United States and Western Europe.4 The paper's quantitative basis was the Political Stress Index, a composite measure combining wage stagnation, intra-elite competition, and state fiscal distress. The prediction was specific enough to be falsifiable. The August 2020 PLOS ONE retrospective, co-authored with Andrey Korotayev, examined the prediction against the 2010–2020 record. The retrospective concluded that the incidence of both non-violent anti-government demonstrations and violent riots in the United States rose "by an order of magnitude" after 2010, with the same pattern visible in the United Kingdom, France, Italy, and Spain.5

The framework that produced the prediction may be wrong about the underlying mechanism — the literature is contested on this point, and the contestation is engaged below. The prediction itself is on the record.

The framework is structural-demographic theory, formalised in Secular Cycles (Turchin and Nefedov, 2009) and applied to US history in Ages of Discord (Turchin, 2016). The mechanism, restated in Turchin's 2023 popular synthesis End Times, runs through what he calls the wealth pump: as income inequality surges and prosperity flows disproportionately to elites, society-wide efforts to become an elite grow more frenzied; the bounded number of status-consistent senior positions against a growing pool of aspirants produces frustrated elite aspirants who harness popular resentment to turn against the established order.

Turchin's operational definition of elite overproduction is precise: the presence of more elites and elite aspirants — those with advanced education, wealth, or power — than society can provide status-consistent positions for. The mechanism, in the structural-demographic literature, runs through three channels. The first is wage stagnation at the median, which compresses popular legitimacy of the existing distributional order. The second is intra-elite competition, which compresses the legitimacy of the elite class itself, as credentialed aspirants compete for a bounded number of senior positions and the unsuccessful share of the cohort — well-educated, networked, organisationally competent — becomes available to a counter-elite politics. The third is state fiscal distress, which compresses the state's capacity to mediate between contending classes via redistribution, public employment, or institutional accommodation.

The Political Stress Index aggregates these three channels into a single time-series. Turchin's reading of the US series, anchored in Ages of Discord and updated periodically since, has the index moving from approximately 7 in the year 2000 to approximately 37 in the year 2012 — comparable in magnitude to the index's reading in the 1850s, the decade preceding the Civil War. The post-2012 reading is harder to pin down precisely, because Turchin has not published a refreshed PSI calculation for 2025–2026 in the academic literature. The honest framing of the gap is that the 7-to-37 figure is locked through 2012, and the 2010 Nature prediction validation runs through 2020. What the index reads now is empirically open. The honest position is to note the gap rather than to invent a number for it.

The empirical anchors for elite overproduction in the present US configuration are visible in three independent datasets. The American Association of University Professors' 2022 study found that only 10.5% of US faculty positions are tenure-track, despite continued PhD production at rates set by an earlier era's institutional structure — a bounded number of senior positions against a structurally over-credentialed candidate pool.6 The Federal Reserve Bank of Minneapolis's 2025 paper "What Happened to the College Wage Premium?" documented that the college wage premium has been roughly stagnant since 2000, even as the credentialed share of the workforce rose from 31% to 45% — a doubling of supply against flat marginal compensation, the classic signature of a labour-market saturation.7 The Federal Reserve's Distribution of Household Wealth data shows the top 0.1% wealth share rising by a multiple of roughly 1.6× from 1989 through 2024 — the wealth-pump mechanism in the data, expressed as a ratio rather than a percentage to avoid ambiguity over whether the change is measured in shares or in percentage points.8

These anchors describe the configuration. Turchin's framework describes the mechanism. The empirical question — and it is the right question to engage honestly — is whether the configuration is caused by the mechanism Turchin specifies, or whether the configuration and the mechanism happen to co-vary because some other underlying structural shift produces both.

The mechanism is contested in the peer-reviewed literature — Georgescu's 2023 PLOS ONE decomposition attributes the wage variance primarily to automation rather than labour oversupply.9 What is not contested is the configuration: the PSI as a descriptive indicator runs from approximately 7 in 2000 to 37 in 2012, and the prediction the 2010 Nature paper made about the 2010–2020 decade has been validated on the PLOS ONE retrospective record. The fact of the rise is on the record; the mechanism by which it occurs is the live academic argument.

IV. The Demographic Layer

The Demographic Crunch (Essay 3) anchored the macro mechanism: the post-1980 disinflation and asset-price expansion was a one-time labour-supply event, and that tailwind has reversed. The mechanism (Goodhart-Pradhan; Lyman Stone on fertility recovery) does not need to be re-anchored here. What this section adds is the historical-scale framing.

Working-age population peaks across the developed world have arrived, or are arriving, in close synchronous sequence: Japan ~1995; Germany ~1998 (sustained above the native-fertility curve only by immigration); Italy ~2002; China 2014 (the cohort has contracted by sixty-eight million in the eleven years since); South Korea ~2016. The US is the last major developed economy still on the rising side, and only because of net immigration; Census Bureau projections are explicit that all US working-age growth through 2050 is expected to come from immigration.

What is new is the synchronisation. Every prior demographic transition involved one country transitioning while others were on a different part of the curve — emerging-market labour absorbing the developed-world ageing, Eastern Europe absorbing Western European ageing, the US absorbing European ageing through capital recycling and immigration. There is no demographic counter-flow available at scale. China was the last; China is now contracting faster, in absolute terms, than any other major economy.

The G7 sovereign debt arithmetic compounds the claim. Average G7 sovereign debt-to-GDP crossed 100% in 2020.10 The only prior modern reading above 100% was post-WWII mobilisation, and that came down between 1945 and the early 1970s principally through demographic-driven nominal GDP growth — the baby boom expanding the denominator faster than the numerator could be issued. The current configuration cannot run that path. The denominator-expansion mechanism that resolved the post-1945 peak is precluded by the demographic configuration. The fiscal anchor and the demographic anchor describe the same constraint from different vantages.

V. The Methodological Corrective

The hazard at this point is the slide into cyclical determinism. Cycle theories — Dalio's, Modelski's, Goldstone's, Turchin's, Howe's — are useful as taxonomy. They become misleading when the taxonomy is mistaken for mechanism, when the recognisable pattern is mistaken for an inevitable trajectory, when the historical analogue is read as a forecast rather than as a constraint.

Adam Tooze's Crashed (2018), Shutdown (2021), and the ongoing Chartbook output provide the discipline that prevents the slide.11 Crisis is not a meteor: it is a sequence of decisions. The 2008 financial crisis was a structural configuration of leverage, deregulation, and shadow-banking exposure that could have resolved without a Lehman-equivalent event. The configuration produced the conditions for systemic instability; the specific shape of the resolution — TARP's architecture, the AIG bailout's structure, the Fed's emergency facilities — was not produced by the configuration. It was produced by decisions Paulson, Bernanke, and Geithner made under stress, in specific institutional roles, on specific days.

The 2020 COVID-19 intervention is the cleaner test case. By every cycle-theoretic reading, the corporate-credit market should have produced a 2008-style cascade through the deepest unemployment readings since 1932. It did not. The reason was the CARES Act fiscal package and the Federal Reserve's March 2020 facilities — specific decisions made in days and weeks rather than years, that altered the trajectory the underlying cycle would have produced.

Tooze's methodological claim, applied to the present essay, is consequential. The configuration produces a narrow set of resolutions — Bourbon France, Ottoman, Edwardian, Habsburg Spain are recognisable rather than infinite — but the specific path through the set is determined by decisions made under the configuration, not by the configuration itself. There is a meaningful difference between a state that crosses Ferguson's Law and resolves through orderly hegemonic transition (Britain, partially, 1922–1956) and one that resolves through revolutionary collapse (Bourbon France, 1788–1799). The configuration was structurally similar; the decisions under the configuration produced different paths through the same constrained set.

This is the discipline the essay needs. The argument is not that history repeats, nor that the cycle is on a known calendar. The configuration produces a recognisable set of futures; the decisions made next matter more than the path of any single underlying variable. Cycle theory's predictive value is bounded; its diagnostic value is real. The Survival Framework and The Opportunity Framework are the manuscript's attempt to construct portfolios robust across the constrained set, not scenarios against a deterministic backdrop.

Each of the historical cases this essay has cited looked from inside like an unprecedented configuration to which the prior record did not apply. The Bourbon court of 1788 had Europe's most sophisticated tax bureaucracy, its largest standing army, and a financial system rebuilt after the John Law collapse; the contemporaneous "this time is different" argument was made on serious institutional grounds. In each subsequent case — the Tanzimat reforms in the late Ottoman world, Edwardian Britain's central bank and naval supremacy — the same claim was made, on equally serious grounds, and in each case it did not hold.

The discipline Tooze's framing imposes on this essay is that the "this time is different" claim — applied to the present US configuration on grounds of central-bank sophistication, institutional depth, technological dynamism, and reserve-currency network effects — is the same claim that has been made and has not held in each prior case. The claim might hold this time. The historical record makes it the lower-probability prior, not the higher-probability prior, against which the diagnostic block's arguments should be priced.

A contemporary version of the same "this time is different" claim is worth engaging by name: the argument that the United States is on the cusp of a state-led industrial mobilisation in which Congress appropriates trillions for chips and power, the leading AI labs voluntarily merge under federal coordination, and the resulting fiscal-military-industrial alignment delivers a decisive economic and military advantage over the CCP. The historical precedents the argument cites are precisely the precedents this essay's empirical record invokes — Manhattan, Apollo, the British rail mania, telecoms, WWII US borrowing. The fiscal preconditions of those precedents are not the fiscal preconditions of 2026.

The argument is Leopold Aschenbrenner's Situational Awareness: the AGI race forces a Manhattan-style federal mobilisation by 2027–28.12 The Manhattan Project began in 1942 against US debt-to-GDP of roughly 50% on a falling trajectory; the AI Project Aschenbrenner forecasts is being proposed against debt-to-GDP above 100% with net interest the largest line item — Ferguson's-Law breached for the first time in a century. The Manhattan Project's fiscal capacity was real; the AI Project's fiscal capacity is contested.

VI. The Optimist Outlier

The same late-stage configuration this essay has been describing produces, on a competing reading, a regenerative resolution: the post-crisis regime is reliably more cohesive, more institutionally robust, and more economically productive than the pre-crisis regime that decayed. The post-Civil War expansion. The post-WWII Bretton Woods order. The post-Reformation peace of Westphalia. The post-Black Death demographic recovery. All are, on this reading, the output of the cycle, not just the cost.

The reading is Neil Howe's, in The Fourth Turning Is Here (Simon & Schuster, 2023) — the manuscript's optimist counterweight. Howe's diagnostic of the present configuration tracks Turchin's, Dalio's, and the diagnostic block's; the disagreement is about the resolution. The full litigation of his regenerative-resolution thesis — including whether long-run progress holds across cycle transitions, against Rosling, Roser, Tupy, and the Hickel/V-Dem counter-record — belongs to Essay 16, The Case for Optimism, not here.

The discipline of including Howe here, briefly, is to make explicit that the diagnostic block's argument is not a permabear argument. It is a structural argument. The structure produces a constrained set of futures; the regenerative future is one element of that set. The manuscript's argument is not that the constrained set excludes flourishing. The manuscript's argument is that the path through the set is decided by decisions made under constraint, that the constraint is binding now, and that the navigation problem the later essays take up is the problem of being well-positioned across the set.

VII. The Constrained Set

The three anchors do not forecast the resolution. They constrain the set. The set is bounded in two directions. Below, by the configuration: states in this configuration do not, in the historical record, return to the prior status quo by inertia — some structural reorganisation occurs. Above, by the available paths: orderly hegemonic transition (Britain), revolutionary collapse (Bourbon France), territorial fragmentation (Ottoman, Habsburg Spain), and the regenerative resolution Howe's framework points to (post-WWII, by partial analogy). Which path the present configuration produces is determined by decisions made under it. The historical analogue tells the reader the decisions matter; it does not tell the reader what they will be.

This is the moment at which the reader's relevant base rate is reset, from seventy years to two thousand. The diagnostic block has not been claiming the system is broken in unprecedented ways — it has been claiming the system is broken in the way the historical record has always shown systems break before they reset.

Footnotes

-

Treasury Financial Report of the United States Government, FY2024 — Statement of Long-Term Fiscal Projections. ↩ ↩2

-

Niall Ferguson, "Ferguson's Law: Debt Service, Military Spending, and the Fiscal Limits of Power," Hoover History Working Paper 202502, February 2025. ↩ ↩2 ↩3

-

Peter Turchin, "Political instability may be a contributor in the coming decade," Nature 463 (2010): 608–609. ↩

-

Peter Turchin and Andrey Korotayev, "The 2010 structural-demographic forecast for the 2010–2020 decade: A retrospective assessment," PLOS ONE (August 2020): e0237458. ↩

-

AAUP — Data Snapshot: Tenure and Contingency in U.S. Higher Education (2022). ↩

-

Federal Reserve Bank of Minneapolis — "What Happened to the College Wage Premium?" (2025). ↩

-

Federal Reserve Distributional Financial Accounts; IndexBox 2025 estimates $88.5T Boomer wealth; Motley Fool/DFA derived 54% equity share. ↩

-

Oana-Maria Georgescu, "The structural-demographic theory revisited: An empirical test for industrialized societies," PLOS ONE 18, no. 11 (2023): e0287912. ↩

-

Adam Tooze, Chartbook (ongoing). Book-length context: Crashed: How a Decade of Financial Crises Changed the World (Viking, 2018); Shutdown: How Covid Shook the World's Economy (Viking, 2021). ↩

-

Leopold Aschenbrenner, Situational Awareness: The Decade Ahead (June 2024); Section IV, "The Project," articulates the trillion-dollar federal-appropriation forecast on the 2027–28 timeline. ↩