The Opportunity Framework

In 60 seconds

Post-resolution positioning, built on the spine of Druckenmiller's Q4 2025 13F with corroborating reads from Faber, Alden and Marks. Three pillars: productive equities (institutional-quality EM, real-asset earnings); commodities and producers (uranium, aluminium, precious metals); cash-equivalents as optionality reserves. The named rotation — Brazil, Alcoa, financials, equal-weight, short long-duration bonds, gold — is illustrative of the framework, not a recommendation.

The prior essay established the defensive posture: convex tail protection, zero long-duration nominal bonds, real-asset allocation against a regime of financial repression. That is the survival architecture. This essay turns to the other question: what does the bear regime actually displace — and where does the displaced capital go?

The displacement is not a metaphor. Capital does not vanish in a regime change; it leaves the configuration the prior regime rewarded and enters the configuration the new regime will. Survival is the precondition for participation; the Opportunity Framework that follows is not a contradiction of the diagnosis — it is what the diagnosis makes possible.

The conclusion, briefly stated up front so the rest can be examined against it. The spine of this essay is the diagnostic-block arithmetic the prior thirteen essays have built. Ferguson's Law breached; equity multiples inconsistent with positive forward real returns; the demographic tailwind reversed; Mag 7 concentration at modern-history extremes; the AI capex/revenue gap; the energy bottleneck pricing two years at the FERC ceiling; private credit's shadow defaults; the political amplifier blocking pre-emptive reform. That arithmetic points an allocator. Stanley Druckenmiller's Q4 2025 Duquesne Family Office positioning is the strongest single articulation of where it points — a portfolio rotated systematically out of the post-1980 default and into the configuration the regime change rewards. Marc Faber's commodity super-cycle, Lyn Alden's Three-Pillar architecture, and Howard Marks's second-level mispricing apparatus are the corroborating reads — independent derivations from different empirical anchors that converge on the same allocation map: real assets and producers, energy infrastructure where the price signal is binding, equal-weight against mechanical-bid concentration, selected emerging-market exposure under an institutional-quality test, and a structural under-allocation to the cap-weighted passive default. The math is what the prior thirteen essays established. This essay operationalises the timing.

A scope note. Names listed in this essay — Brazil via EWZ and EWZ calls, Alcoa, Delta and American, the Financial Select Sector SPDR, the Invesco S&P 500 Equal Weight ETF, Treasury shorts via inverse ETFs, Barrick Gold — are illustrative of the framework, not a recommendation; do your own work. The Druckenmiller 13F is a publicly filed record, not a tip sheet.

I. The Question — What the Manuscript's Argument Cashes Out To

The prior twelve essays have done the diagnostic work. Ferguson's Law breached in FY2024.1 Equity multiples are not consistent with positive forward real returns at the index level.2 The demographic tailwind that ran from 1965 to 2015 has reversed; Japan's thirty-four-year residential property deflation and the BOJ's 49% holding of JGBs outstanding is the empirical preview, not the analogue.3 Mag 7 concentration is at modern-history extremes — top ten S&P 500 names above 40% of the index, with the consumer-revenue concentration The AI Reckoning documented.4 The AI capex programme runs against Cahn's revenue gap.5 PJM capacity has cleared at the FERC ceiling of $329.17 per megawatt-day for two consecutive years.6 The political amplifier cannot reform before crisis. The cracks are mechanically aligned to the same 2026–2027 window. The Survival Framework documented the defensive architecture against this regime.

What follows is the question the prior essay left open: given that the regime requires this defensive architecture, where does the architecture create asymmetric opportunity?

The answer lives at the intersection of three simultaneously-true facts. The regime in the watch window is structurally hostile to the post-1980 portfolio default — the cap-weighted passive index, the long-duration nominal bond, the developed-market consumer-AI mega-cap concentration. The long-arc capability expansion documented in The Case for Optimism — the 99.5% solar PV cost decline since 1977, the 35-year poverty-reduction trajectory, the cumulative-knowledge compound — operates on a different time horizon and through different mechanisms; it does not reverse in a financial crisis. The bear regime applies to the watch window. The optimism applies to the multi-decade arc. Opportunity holds both. Watch-window survival positioning is a different portfolio from multi-decade-arc structural reallocation; confusing them is the final form of the trap.

The opportunity is not the absence of the bear regime. The opportunity is what the bear regime structurally produces.

II. Reading the Macro — Where the Diagnostic Arithmetic Points an Allocator

The four structural tailwinds that drove the post-1980 bull market — deflationary globalisation, the secular bond-yield decline from Volcker to zero, the demographic expansion that built the mechanical bid, and the multiple expansion that compounded the first three — have all reversed inside the diagnostic block's arithmetic. The 1982-to-2021 portfolio default does not survive that reversal, and the arithmetic itself forces the rotation this essay describes. The strongest single articulation of that rotation in public form is Stanley Druckenmiller's, who put the historical-analogue claim cleanly in Fortune, September 15, 2022:

"There's a high probability in my mind that the market, at best, is going to be kind of flat for 10 years, sort of like this '66 to '82 time period."7

And the structural-reversal claim that underwrites it. Druckenmiller, in the same Fortune piece (syndicated by The Acquirer's Multiple):

"When I look back at the bull market that we've had in financial assets really starting in 1982…all the factors that created that not only have stopped, they've reversed."8

The framework rests on a historical claim. The 1982-to-2021 bull market was driven by the compounding of four structural tailwinds: deflationary globalisation; the secular bond-yield decline from the Volcker peak of 1981 to the zero bound of 2020; demographic expansion in developed markets — the boomer cohort moving through peak earning and peak asset-accumulation years, with the equity-side transmission running through pension and 401(k) plan flows that built the mechanical bid; and multiple expansion as the consequence of the first three.

The central claim is not that the four tailwinds have weakened. It is that they have reversed. Globalisation has reversed into tariff regimes and supply-chain reshoring. The bond-yield secular decline has reversed into a fiscal-dominance regime in which, per Hunt's monetary-policy-asymmetry argument, the Fed cannot loosen meaningfully without producing the inflationary outcome the policy is supposedly designed to prevent. The demographic expansion has reversed — Goodhart and Pradhan's framing is that the next three decades will look more like the 1970s than the 2010s, with worse demographics, and Japan's thirty-four-year residential property deflation is the developed-economy preview.3 Multiple expansion has reversed into multiple compression: every ten-year window starting at 23× forward earnings produces an annualised real return between +2% and −2%, every time.2

The 1966-to-1982 regime is the closest historical parallel: positive nominal returns, negative real returns, broad-index underperformance, with a specific subset of companies — those founded during the structurally flat regime — emerging as the largest companies of the next cycle. The framework is not a prediction that 2026-to-2042 will be 1966-to-1982: the 1970s were inflation-without-financial-fragility; the current configuration is inflation-with-financial-fragility. The analogue is a pattern-recognition lens, not historical prophecy. It translates the diagnostic block's regime change into an instruction: rotate out of the configuration the post-1982 regime rewarded; rotate into the configuration the post-1982 regime systematically under-owned.

The demographic-inversion reading is the most under-stated piece. The 1966-to-1982 regime was a demographic-inversion story before it was anything else: boomers were entering the workforce at the start; the cohort retiring across the regime was the smaller pre-war cohort. The 2026-to-2042 regime is the same story in reverse — boomers retiring at the start, the entering cohort structurally smaller. The 1966-to-1982 analogue is, at the deepest level, the same demographic mechanism running in reverse.

The framework is testable at a specific level: what does it look like when an investor working from the analogue actually allocates capital? Druckenmiller's Q4 2025 13F filing for the Duquesne Family Office shows $4.49 billion across sixty-two positions with 43.06% turnover.9 The exits are as informative as the entries. Nvidia, held in size 2023-to-2024, was exited completely — "I couldn't stand success."10 Meta, Boeing, BlackRock, Bank of America, Citigroup all exited. The pattern is a withdrawal from concentration in the consumer-AI mega-cap complex.

The entries are the operationalisation: Brazil ($247 million combined EWZ equity and calls), Alcoa ($73 million on the aluminium / AI-capex energy-intensity thesis), Delta and American (cyclical rotation), XLF ($301 million on financials outperforming in inflationary cyclical regimes), RSP ($225 million on equal-weight beating mega-cap), inverse Treasury ETFs (15-to-20% of portfolio notional — Druckenmiller has said he shorted bonds "literally the day the Fed cut" 50 basis points, viewing the cut as a mistake11), and Barrick Gold across late 2024-to-2025, building on the long-standing rationale Druckenmiller articulated to Bloomberg in February 2017: "I wanted to own some currency and no country wants its currency to strengthen."12

Brazil + Alcoa + airlines + financials + equal-weight + short bonds + gold. That is a portfolio rotated systematically away from the post-1980 default and into a configuration the post-1980 regime made unfashionable. It is, almost by construction, the opposite of the cap-weighted passive index produced by 401(k) auto-enrollment flows. The specific names are the operational expression; the framework is what travels.

Illustrative positions (not advice — do your own work)

| Position | Rationale | Risk |

|---|---|---|

| EWZ + EWZ calls | Brazil: rate cuts coming; commodity exposure; institutional-quality EM | Lula fiscal slippage; commodity bear |

| Alcoa | AI capex bottleneck → aluminium demand; tight supply | Recession demand-destruction |

| Delta / American | Post-pandemic capacity discipline; pricing power; balance-sheet rebuild | Fuel spike; consumer demand softness |

| XLF (US financials) | Steepening yield curve; rate normalisation tailwind; M&A pipeline | Credit-cycle exposure |

| RSP (S&P equal-weight) | Mag 7 concentration unwinds → equal-weight outperforms cap-weight | Bull-continuation scenario unwinds the thesis |

| Short long-duration Treasuries (inverse ETFs) | Fiscal arithmetic + supply-demand at the long end | Recession bid for duration |

| Barrick Gold | Gold producer leverage to fiscal-credibility arbitrage | Mining-equity beta to broader market drawdown |

| Uranium producers/trusts | AI energy demand structural; uranium supply constrained | Long-cycle; sentiment-driven volatility |

The Alcoa position converges on the manuscript's most concrete opportunity data point. PJM capacity has cleared at $329.17 per megawatt-day for two consecutive years — the textbook empirical signature of a binding physical constraint that capital has not yet repriced.6 Alcoa is the bet that the energy-and-materials layer of the AI capex cycle earns the revenue the platform layer is failing to translate into earnings. The picks-and-shovels argument — DeepSeek's reported sub-$6 million training cost on Huawei chips, the most disruptive single data point for the hyperscaler capex thesis13 — converges on the same point. If inference cost commoditises, the value accrues to the physical infrastructure layer: energy, materials, data-centre construction.

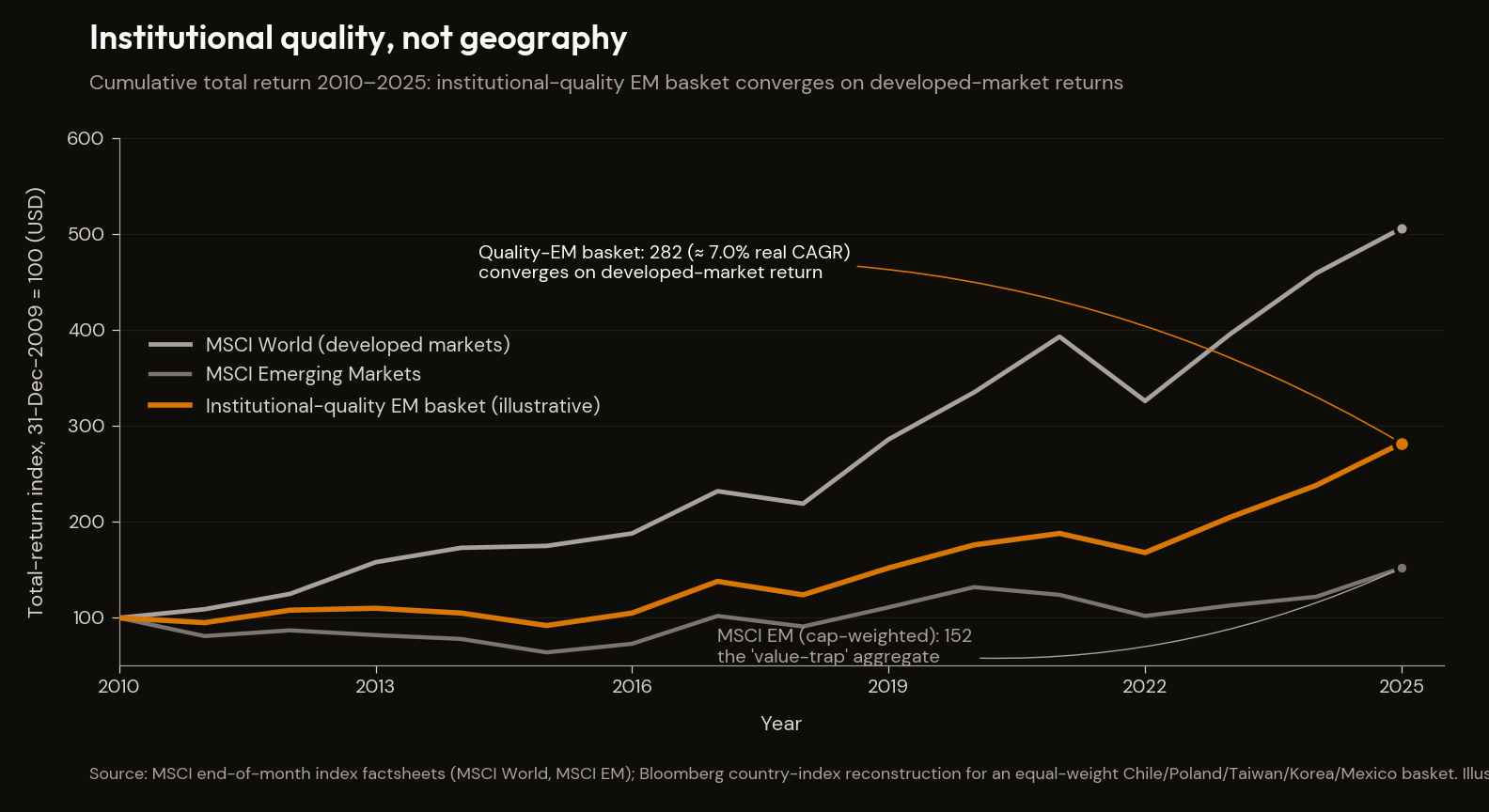

The Brazil position cross-references the de-dollarisation analysis upstream, which foreclosed the naive de-dollarisation thesis empirically. The Renminbi sits at 2.5% of COFER reserves;14 70% of EM external sovereign debt is dollar-denominated; approximately $13 trillion of dollar-denominated debt outside the United States is the empirical anchor of dollar inescapability.15 The opportunity is not exit US, buy everything non-US. Brazil is an opportunity story for specific reasons — resource exporter to the dollar system, improving institutions on certain dimensions, undervalued currency against dollar-debt fundamentals, exposure to the commodity super-cycle. The institutional-quality axis is the discriminator. The geography is secondary.

III. The Commodity Super-Cycle — Decadal Under-Investment

The macro positioning tells you the regime. The cyclical lens tells you how long the regime lasts and which underlying real-asset cycle it sits inside. Marc Faber's framework on commodity super-cycles — with Tomorrow's Gold (CLSA Books, 2002) as the original cyclical anchor and the 2015 MarcoPolis commentary the more recent articulation — corroborates Druckenmiller's positioning from a different empirical base, and is testable ex ante:

"Commodity cycles last 45 to 60 years roughly, from trough to trough or peak to peak, with a peak in 1980, weak prices throughout the 1980s and 1990s, and a pickup starting in 1999 that made a peak for most commodities in 2008."16

Tomorrow's Gold was published in 2002; the 1980 peak and 1999 trough were already in the data, but the 2008 commodity peak was a forward call. It materialised on schedule. The current reading: last trough approximately 1999-to-2000. Peak 2008. Correction 2008-to-2020. Renewed pickup from 2020, accelerating across 2022-to-2026 with the energy crisis, structural under-investment in extractive capex through the 2014-to-2020 down-cycle, and the AI-capex demand inflection. We are six-to-eight years into a cycle that has another twenty-to-thirty-plus years to run.

The implication is operational. Emerging-market equities and commodity producers are not one-to-two-year mean-reversion plays — they are secular rotations on a decade-or-more time horizon. The convergence with the energy-bottleneck analysis from a different empirical anchor is the signature of a structurally under-invested real-asset complex meeting a structurally inflationary policy regime at the same time.

The contrarian principle is the meta-rule: the asset that has outperformed for 25 years is owned by almost nobody, which is the definition of a contrarian trade. US large-cap equities have outperformed since the late 1990s on every long-horizon metric that matters. Consensus capital is crowded into US mega-cap, US dollar, long-duration nominal bonds, and mega-cap technology.

The currency-debasement framing closes the cyclical reading. Faber's recurring thesis in Gloom, Boom & Doom Report commentary is that all paper money — dollars, euros, rupees — is losing value, and that measured against gold, silver, or platinum, equity indices are all down.17 The framework requires the structural observation that simultaneous fiscal trajectories of every major fiat-issuing economy produce currency-debasement pressure. The operational test is purchasing power, not nominal price.

Addition not substitution runs as the manuscript-wide lens. Renewables add to fossil generation in the near term; they do not replace it. The portfolio-level corollary: capital allocates additionally to real assets; it does not substitute the entire portfolio.

IV. The Three-Pillar Allocation — Real Assets, Producers, Cash

The macro spine and the cyclical lens are the what. The allocation framework is the how. Lyn Alden's Three-Pillar Portfolio converts the regime claim into a portfolio architecture and corroborates the Druckenmiller rotation from a third empirical base.18

"the three main pillars consist of 1) profitable equities 2) commodities/producers and hard monies and 3) cash-equivalents."19

The three pillars are the structural frame. Specific weights vary by inflation regime and relative valuations across pillars. The pillar structure is the load-bearing claim; the percentages below are the operationally honest commitment, not an instruction.

The three-pillar opportunity allocation (illustrative ranges)

| Pillar | Indicative range | Reasoning | Examples |

|---|---|---|---|

| Productive equities (institutional-quality EM, real-asset earnings) | 50% | Real cash flow with limited fiscal-flow dependency; institutional-quality discount | Brazil ETFs + call exposure; Vietnam, Indonesia; fallen-angel bond ETFs; quality dividend producers |

| Commodities, producers, and hard-asset exposures | 25–30% | Demographic + energy + fiscal regimes all favour real assets | Uranium producers/trusts; precious-metals equities (Barrick etc.); aluminium (Alcoa); copper producers; oil & gas E&P with disciplined capex |

| Cash-equivalents & optionality reserves | 20–25% | Dry powder for asymmetric rotations; yield in short-duration | Short-Treasury via inverse ETFs (TBT-equivalent) where rate view directional; short-credit; option premium |

The operational structure of the second pillar is the distinctive contribution. Distinguish high-stockpile commodities — precious metals, uranium, agricultural commodities — from constrained-supply commodities — oil, natural gas, certain industrial metals. For high-stockpile commodities, producers have weak pricing power; the framework recommends direct ownership of the underlying commodity or a commodity trust. For constrained-supply commodities, producers can have meaningful pricing power, but only if they exercise capital discipline. XLE's underperformance through 2022-to-2025 despite rising oil prices is the empirical validation.

The third pillar — cash-equivalents — is an optionality pillar, not a returns pillar. The function is dry-powder discipline: a cash reserve that allows redeployment when assets go on sale. The allocation is asymmetric — higher when equities and commodities are expensive, lower when cheap.

The Bitcoin allocation is modest, conditional, and tied to fiscal dominance. Most of the excess returns came from replacing a small slice (typically 2-5%) of the equity portion with bitcoin-related securities.19 Bitcoin is a small optional sub-allocation that captures the monetary-expansion tail of the fiscal-dominance regime without making the portfolio's outcome contingent on Bitcoin succeeding.

The purchasing-power lens is the framework's distinctive analytical move. Alden's recurring framing is that investors should think in terms of purchasing power, not just nominal returns.20 A portfolio that produces positive nominal returns while losing purchasing power against gold, against Bitcoin, against an internationally-traded basket of commodities — that portfolio is failing on the framework's primary metric.

The Three-Pillar Portfolio is reflation-independent by construction. Hunt's monetary-policy asymmetry — tightening still bites in over-indebted economies; loosening pushes on a string as velocity collapses — means the framework cannot wait for the Fed.

The dollar-system point matters because it constrains how the framework actually accesses non-dollar exposure. The framework does not exit the dollar system. It uses dollar-denominated instruments — accessible ETFs, dollar-listed commodity exposure, dollar-denominated EM access — to access non-dollar real-asset exposure. The institutional-quality axis is the discriminator.

V. The Mispricing Apparatus — Second-Level Thinking on the Under-Owned

The macro positioning and the cyclical lens identify the regime. The allocation framework identifies the pillars. The mispricing apparatus identifies which side of the trade is under-owned — second-level thinking, the discipline that distinguishes targeted opportunity from naive contrarianism, and the fourth empirical base corroborating the rotation.

"Second-level thinking is deep, complex and convoluted." First-level thinking, in Marks's formulation, says "'It's a good company; let's buy the stock.'" Second-level thinking says "'It's a good company, but everyone thinks it's a great company, and it's not.'"21

First-level thinking buys the cheap asset. Second-level thinking asks why the asset is cheap and whether the consensus has correctly identified the reasons. Sometimes the consensus is right and the asset is cheap because the underlying business is genuinely impaired — a value trap. Sometimes the consensus is wrong and the asset is cheap because it has been mechanically dumped, ignored, or systematically under-owned by a flow regime that is not pricing fundamentals — a mispriced opportunity. The discipline is in the separation. The framework rules out being contrarian for contrarian's sake: to be an intelligent contrarian, you have to know what others are doing, know why they're doing it, know what's wrong with what they're doing, and then figure out if there's appropriate action to be taken on that.21

Apply the apparatus. Mag 7 is priced for perfection. The consumer-revenue concentration, the 18-to-23% consensus EPS growth required to justify current multiples, Cahn's revenue gap5 — every bear case is priced in, every growth case is priced in, the margin of safety is thin to zero. The appropriate action is under-allocation relative to the cap-weighted index, not necessarily a short position. The operational consequence is the rotation documented above.

The inverse application is the framework's distinctive contribution. What is priced as failure that is merely under-owned? Brazil. Indonesia. Vietnam. Energy infrastructure. Uranium. The aluminium-and-copper-and-grid-equipment supply chain to AI capex. Selected EM credit. Fallen-angel bond ETFs, where mechanical sellers from BBB-constrained mandates produce systematic mispricing across the BBB-to-BB threshold. None of these are priced as failure because they are failing on fundamentals. They are priced as failure because the post-1980 portfolio default does not allocate to them at scale, and the mechanical-bid framework means the marginal flow does not reach them. Mechanical, not informed. The apparatus identifies these positions not as contrarian bets but as systematically under-owned for mechanical reasons. The opportunity is the under-owned side.

The cycle-aware diagnostic, in Mastering the Market Cycle (Houghton Mifflin Harcourt, 2018), runs through four conditions: profits more likely to swing upward than down; investor psychology sober rather than buoyant; risk consciousness real rather than complacent; and market prices not yet moved too high.22

Apply the four conditions to early-2026. Investor psychology — buoyant on Mag 7, complacent on credit spreads, sober on specific segments (energy, EM, aluminium). Risk consciousness — low on tight credit spreads where the high-yield default rate sits at 1.8% versus the 2.5% post-GFC average while spreads have compressed regardless.23 Market prices — high on mega-cap equities; under-owned in specific commodity, EM, and energy-infrastructure segments. Opportunities exist within specific segments, not across the broad market.

The November 2025 credit-spread warning makes the operational point.24 The compressed spreads of 2025 are not a sign of low credit risk; they are a sign of low risk consciousness. When the high-yield default rate is below long-run average and spreads have compressed below long-run average, risk has not been priced out of the market — it has been un-noticed. The response is not to chase yield at compressed spreads; it is to wait for the mispricing to be re-priced, and deploy capital at the dislocation. The same apparatus anchors The Survival Framework's defensive posture and the Opportunity Framework's tactical mispricing identification — one apparatus, two operational consequences.

VI. The Synthesis — One Spine, Three Corroborations, One Allocation Map

The framework is built on Druckenmiller's positioning, with Faber's commodity super-cycle, Alden's Three-Pillar architecture, and Marks's second-level mispricing apparatus as corroborating reads from independent empirical anchors. The convergence is what makes the thesis defensible: four people, looking at the regime from different vantage points and with different methodologies, allocating capital toward the same configuration.

Four lenses on the rotation thesis

| Lens | Voice | Core read | Where it overlaps |

|---|---|---|---|

| Macro-spine (primary) | Druckenmiller (Q4 2025 13F) | EM institutional-quality; commodities; short long-bond | All four converge on the rotation away from cap-weighted DM equity |

| Cycle / commodities | Marc Faber | Real assets vs financial assets; gold; EM selectively | Faber + Druckenmiller on commodity-producer rotation |

| Liquidity macro | Lyn Alden | Fiscal-dominance tail; gold; selected emerging | Alden + Druckenmiller on fiscal-credibility positioning |

| Skeptical bull | Howard Marks | Defensive at 23× forward P/E; rotation discipline | Marks discipline = Druckenmiller's risk-management approach |

Honest framing: the framework's spine is the diagnostic-block arithmetic from the prior thirteen essays — not Druckenmiller. Druckenmiller's Q4 2025 positioning is the strongest single articulation of where that arithmetic points an allocator with a four-decade record, with Faber, Alden and Marks as corroborating reads from independent methodological starting points. The defensibility rests on the convergence across the four lenses and the structural derivability of the rotation from the manuscript's prior arithmetic — not on any one investor's 13F.

The allocation map: real assets and producers; energy infrastructure where the price signal is binding; equal-weight against mechanical-bid concentration; selected emerging-market exposure under an institutional-quality test; gold at 10-to-25% on the deleveraging-anatomy reading from Survival; Bitcoin at small allocation as the fiscal-dominance tail; cash as dry powder for dislocation deployment; structural under-allocation to the cap-weighted passive default.

The institutional-quality axis is the discriminator. The de-dollarisation analysis upstream foreclosed the naive de-dollarisation thesis. The thesis is targeted: capital allocation follows institutional quality, not geography. Brazil, Indonesia, and Vietnam are opportunity stories because of specific resource endowments, improving institutions on certain dimensions, and undervalued currencies against dollar-debt fundamentals — not because they are non-US. The institutional-quality-not-geography case found its sharpest form in the JSE-Top-40-earns-offshore observation: the listing geography is not the investment geometry. The opportunity is in globally competitive businesses listed in jurisdictions whose institutional cover is thinning, not in local-state-dependent businesses.

The AI-capex / sovereign-debt forced choice closes the synthesis. The misallocation creates the opportunity. The platform layer — Mag 7 — cannot earn what its current valuation requires.5 The suppliers to the capex programme — Alcoa, the energy-infrastructure stack, transformer and grid-equipment manufacturers, the copper-and-rare-earths supply chain, the uranium producers and trusts, the picks-and-shovels of the AI build-out — earn the revenue regardless of whether the platform layer earns its return. PJM's auction at $329.17 per megawatt-day for two consecutive years is the pricing signal.6 The constraint is binding; capital has not yet repriced.

The dragon-king recovery framework adds the timing discipline: crashes are not randomly distributed; they are preceded by structural signatures, and the post-crash period shows systematic mispricing of recovery assets. Opportunity is not available before the mechanism completes — it arrives at the phase transition's other side. Survival is the precondition for participation. The Opportunity Framework is what the precondition is for.

The math — Druckenmiller's structural-reversal positioning, the commodity super-cycle, the Three-Pillar architecture, the mispricing apparatus — converges on a coherent allocation. The timing — when the dislocations crystallise into prices that reward the allocation — is the watch-window-versus-multi-decade-arc distinction. Survival positions for the watch window; Opportunity positions for the multi-decade arc. They are different portfolios. The reader who holds both correctly is the reader who can survive the watch window with sufficient capital to participate in the long-arc rotation.

A brief execution aside, because two cognitive habits earn separate naming even when the surrounding apparatus is cut: do outside-view-first sequencing on base rates before any case-specific analysis — what does the historical reference class do at this configuration, before what is specific about this configuration adjusts it; and pre-commit to revision rules — state at the time of forming a view what specific evidence would cause you to raise or lower the probability. These are the two cognitive disciplines that travel; the rest of the cognitive-stack apparatus does not need to.

VII. Honest Counter-Arguments

Eight counters engaged at the steel-man version; Appendix A extends several at length. The first is the structural tension the manuscript's own diagnostic block raises against the framework.

0. "The manuscript spends fourteen essays calling Treasury demand 'mechanical, not informed' — and then builds the Opportunity Framework on Druckenmiller's 13F." This is the sharpest internal counter and it must be named. The diagnostic block's recurring motif is that flows-not-fundamentals distort price discovery — the mechanical bid is structural, not informed; the 401(k) auto-enrollment vector and the BOJ ownership of 49% of JGBs are mechanical, not informed. Building a tactical rotation on one investor's 13F is, on its face, the kind of macro-guru anchor the diagnostic block's epistemics rule out. The response is structural. Druckenmiller's Q4 2025 positioning is treated in this essay as a corroborating diagnostic of the regime change, not as the basis for the framework's claims. The four-lens convergence — Druckenmiller, Faber, Alden, Marks, arriving at the same allocation from four different methodological starting points — is the diagnostic; the rotation that emerges from it is structurally derivable from the diagnostic block's arithmetic without any one investor's positioning carrying it. The energy-bottleneck PJM auction, the Cahn revenue gap, the 60% defensive weight at 23× forward earnings, the institutional-quality EM axis against the foreclosed naive de-dollarisation thesis — each is independently derivable from the manuscript's prior essays. Druckenmiller's 13F is one piece of supporting evidence that an investor with a four-decade record, operating with the same diagnostic, allocated the same way. It is not the spine. The spine is the diagnostic-block arithmetic. The convergence is the argument.

1. "Druckenmiller's track record runs through the great bond bull. He hasn't run an active fund through a structurally different regime." The sharpest external counter. Duquesne Capital closed to external capital in 2000 after returning approximately 30% annualised. The Q4 2025 rotation has not been pressure-tested by a sustained bear regime. The response: the framework — that structural reversals require rotation — is testable independent of the personal track record. The willingness to rotate from conviction-tech (Nvidia 2023-to-2024) to conviction-EM (Brazil at $247 million notional Q4 2025) and to short Treasuries despite a decades-long bearish-bond track record demonstrates self-correction. The framework rests on Druckenmiller's positioning with corroborating reads from Faber, Alden and Marks — four independent voices, one convergent allocation.

2. "The cyclical framework has been bearish on US equities since the 1990s. The call has not paid." Empirically true. The S&P 500 returned approximately 450% from 1995-to-2025. The framework is about cycles, not perpetual bearishness. The 1987 crash, 2000 Nasdaq peak, and 2002-to-2008 commodity super-cycle peak were all correctly called. The 1980/1999/2008 sequence in Tomorrow's Gold is the ex-ante validation. The 2025-to-2026 EM positioning comes after Q3-Q4 2025 EM outperformance — confirmation of an emerging trend, not an early contrarian call.

3. "Frontier markets have been a value trap. Institutional capital cannot scale into them." The sharpest operational counter. EM equities are often cheap for reasons: illiquidity, lower governance standards, capital controls, political risk, currency volatility. The response is the institutional-quality axis. Brazil, Indonesia, and Vietnam are opportunity stories because of specific resource endowments, improving institutions, and undervalued currencies against dollar-debt fundamentals — not because they are non-US. The recommendation is selective — typically 5-to-15% of equity exposure, not 50%.

4. "The mispricing framework requires capital, time, and structural advantage retail investors don't have." Oaktree has $165 billion AUM, institutional relationships, full research teams. The response: the framework is identification, not execution. Retail can adopt second-level thinking, cycle awareness, patience, discipline. Direct deployment via accessible instruments: equal-weight index ETFs, diversified commodity ETFs, gold via bullion or trusts, high-quality EM ETFs (iShares MSCI Brazil is accessible to any retail investor). The thesis is transferable; the execution is not, at the scale Oaktree operates.

5. "Active stock-picking macro hedge funds have systematically underperformed since 2008." Empirically true. The argument is structural: the post-1982 regime is broken. The 2010-to-2020 hedge-fund underperformance reflected a regime in which passive flows mechanically over-concentrated capital in the largest names. The contrarian bet pays when the mechanical concentration unwinds.

6. "You can't time the rotation. Just buy global equities and rebalance." The 60/40 default is conceptually robust over 30-to-50-year horizons. The response: the watch window is the load-bearing distinction. Survival positioning is for a watch window in which the cap-weighted index is itself a concentrated bet on the consumer-AI complex (top ten S&P = 40%-plus of the index). The rotation is structural reallocation that prices the regime change the cap-weighted index cannot price. The honest position is both watch-window survival positioning and multi-decade-arc structural reallocation.

7. "EM diversification reproduces dollar-system risk in less liquid wrappers." 70% of EM external sovereign debt remains USD-denominated.15 The response is targeted dollar-system arbitrage: own resource-exporting nations with improving institutions whose currencies are undervalued against dollar-debt fundamentals. The Brazil call — 3.55 million EWZ shares plus $134 million call options, all denominated in USD — is the framework operationalised: long EWZ via dollar-denominated ETF, leveraged via call options, in a market where commodity exposure plus improving institutions plus undervalued real-against-dollar-debt converge.9 The framework is selective use of dollar-system instruments to access non-dollar real-asset exposure, not exit-from-dollar-system.

VIII. One Discipline Before the Close — The Hard-to-Vary Filter

The four-lens convergence above does load-bearing work for the framework, but the manuscript's reader is entitled to a methodological discipline that distinguishes the framework from its bull-case alternatives. David Deutsch's hard-to-vary criterion is the right tool. (Deutsch is treated at greater depth in The Case for Optimism, §III, in the "mechanism, not just the data" subsection.)

A hard-to-vary explanation is one whose components are tightly coupled — change one and the explanation breaks. The bull case for AI productivity has historically been easy-to-vary: when the productivity data does not arrive, the timeline shifts; when one transmission mechanism fails, another is named; when displacement appears, the productivity-offsets story rotates to retraining or to "augmentation rather than substitution." An easy-to-vary explanation accommodates any outcome and predicts nothing.

The manuscript's diagnostic block, applied to the watch window, is hard-to-vary by design. The fiscal arithmetic, the demographic configuration, the AI capex/revenue gap, the energy bottleneck, the credit-fragility composite — change any single component (immigration recovers, AI productivity arrives at the GP-tech historical base rate, the energy buildout closes the constraint, exorbitant privilege defers the constraint indefinitely) and the watch-window timing argument materially weakens. That is the right structure for the claim. The framework should be vulnerable to specific empirical updates, not robust to all of them.

A reader applying the same discipline to the bull-case rotations Appendix A engages should find each rebuttal more hard-to-vary in its long-arc claim and less hard-to-vary in its watch-window timing claim. That is the right calibration. The framework's defensibility rests on this asymmetry — and it is the same discipline this essay's allocation rests on.

IX. Closing — Rotation, Not Exit

The manuscript opened with an observation. The fiscal math of the United States does not work. It is not a question of will or politics; it is a question of arithmetic.

Fourteen essays later, the answer has been assembled. The arithmetic balances through a regime change. The watch-window 2026-to-2027 fragility is structural; the political amplifier cannot reform before crisis; the Fed cannot loosen meaningfully without producing the inflation the policy is supposedly designed to prevent; the AI capex programme cannot earn its returns at the platform layer; the energy build-out cannot substitute on the schedule the hyperscalers require; the demographic tailwind has reversed; the cap-weighted passive default is a concentrated bet at multiples consistent with negative forward real returns. The configuration does not resolve gradually. It resolves through the regenerative-resolution pattern The Case for Optimism develops: structural fragility crystallises, institutional resolution arrives under duress, the assets that survive intact become the seed of what comes next.

The Survival Framework is the architecture that allows the reader to survive the resolution. The Opportunity Framework is the structural reallocation that participates in what comes next. Different portfolios on different time horizons. Confusing them is the final form of the trap; holding both is the analytical move.

The framework is rotation, not exit. The dollar system is not being abandoned; it is being used as the access layer for the assets the post-1980 regime systematically under-owned. The bear regime documented across the prior thirteen essays does not vaporise capital. It displaces it. The Opportunity Framework is where the displaced capital meets the rotation that rewards informed positioning when the mechanical bid reverses.

Inside the 1966-to-1982 regime — the analogue Druckenmiller has been pointing at — Apple Computer was founded in 1976, Home Depot was founded in 1978, and the world's most valuable companies of the next cycle were born inside a structurally flat nominal-return environment. The question is not whether the crisis produces opportunity. The question is whether you survive intact to participate.

Footnotes

-

Howard Marks, The Calculus of Value (Oaktree Capital memo). ↩ ↩2

-

Charles Goodhart and Manoj Pradhan, The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival (Palgrave Macmillan, 2020). Publisher page. LSE School of Public Policy working-paper version. ↩ ↩2

-

Motley Fool — Magnificent Seven S&P 500 Tracker (April 14 2026). ↩

-

AI's $600B Question, Sequoia Capital, September 2024. ↩ ↩2 ↩3

-

PJM Reliability Pricing Model — capacity auction results portal. ↩ ↩2 ↩3

-

Stanley Druckenmiller interview cited in Shawn Tully, "Legendary investor Stanley Druckenmiller warns there is a 'high probability' the stock market will be 'flat' for an entire decade," Fortune, September 15 2022. ↩

-

"Stanley Druckenmiller: The Market Is Going To Be Flat For 10 Years," The Acquirer's Multiple (September 2022). ↩

-

Morgan Stanley — Hard Lessons podcast with Iliana Bouzali, "Duquesne's Stan Druckenmiller" (February 2025). "I couldn't stand success" was Druckenmiller's framing for exiting Nvidia at the end of his 2023–24 holding period. ↩

-

Norges Bank Investment Management — In Good Company podcast with Nicolai Tangen (November 2024). The "literally the day the Fed cut" formulation is verbatim from the same interview; surrounding rationale (50bp cut framed as a mistake) is paraphrased from the broader transcript. ↩

-

Stanley Druckenmiller, Bloomberg interview, "Druckenmiller Bought Gold in December, Reversing November Stance" (February 8, 2017). The "no country wants its currency to strengthen" rationale is the long-standing currency-rationale Druckenmiller carried forward into the Q4 2024 – Q1 2025 Barrick Gold position visible in 13F.info — Duquesne Family Office holdings. ↩

-

BIS Quarterly Review, December 2022 — "Dollar Debt in FX Swaps and Forwards: Huge, Missing and Growing". ↩ ↩2

-

Marc Faber, MarcoPolis interview, "Marc Faber on Commodities and the Commodities Super-Cycle" (August 6, 2015); cyclical framework originally developed in Tomorrow's Gold: Asia's Age of Discovery (CLSA Books, 2002). ↩

-

"2026 Warning: Most Investors Are Walking Into a Trap Right Now". ↩

-

Lyn Alden, April 2024 Newsletter (Lyn Alden Investment Strategy). The three-pillar formulation and the 2-to-5% Bitcoin-replacement observation appear verbatim in the April 2024 newsletter. ↩ ↩2

-

Howard Marks, The Most Important Thing: Uncommon Sense for the Thoughtful Investor (Columbia Business School Publishing, 2011). ↩ ↩2

-

Howard Marks, Mastering the Market Cycle: Getting the Odds on Your Side (Houghton Mifflin Harcourt, 2018); notes summary at Novel Investor. ↩

-

Oaktree Capital — The Roundup: Top Takeaways from Oaktree's Quarterly Letters – December 2025 Edition. ↩

-

CNBC — "Veteran investor Howard Marks warns over credit 'carelessness'" (November 12 2025). ↩