The World Outside America

In 60 seconds

The dollar system did not collapse. It migrated. USD reserve share has moved gradually from ~73% (2001) to ~57% (mid-2025), substantially absorbed by gold rather than by any rival currency. China's surplus is the forced export of domestic underconsumption — the institutional structures that would let households consume more have not been built. The K-shape that applies within economies applies between them with equal force. Elsewhere is mostly still here: the real diversification axis is institutional quality and current-account configuration, not geography.

The dollar system did not collapse. It migrated.

If the diagnostic block established that the post-2008 financial system is structurally broken on its own arithmetic, and the companion essay on crypto established that the most successful crypto product has been wired into the Treasury market by statute, the natural investor question is no longer when does the dollar end? It is what does the world outside America actually look like, given that the dollar does not end? The conventional answer is to move capital elsewhere — buy the rise of the rest, diversify out of the US into the markets that benefit from American structural overextension.

This essay's answer is qualified in a way most investors do not want to hear: elsewhere is mostly still here. The post-American world, in its monetary architecture, is the dollar system extended further into precisely the places where the rotation thesis says capital should flow. Chinese overcapacity does not resolve when its export destination shifts. EM diversification reproduces dollar-system risk in less liquid wrappers. The K-shape applies with equal force between economies as within them. Strong-institutional countries are navigating the post-2020 polycrisis. Weak-institutional countries are experiencing the same global pressures as catastrophic shocks. The investment axis that matters is institutional quality and current-account structure. Geography is the abstraction that hides it.

The argument runs from a Cape Town vantage that the four canonical voices — Pettis on the mechanism, Setser on the empirics, Tooze on the K-shape between countries, Zakaria on the geopolitical rise of the rest — articulate from inside the dollar-system core. The view from the periphery, where I write, sees the same architecture from the other side of the rotation thesis: as an EM that is itself one of the destinations capital is supposedly rotating into, and one whose dollar-denominated borrowing costs are the real-time price of any shift in the meta-clock the architectural voices describe. The mechanism is structural, the empirics are persistent, the global K-shape is the transmission, and the geopolitical narrative is the part of the post-American world that has changed without changing the part that has not.

I. The Mechanism — Pettis's Architectural Constraint

Current account imbalances are the international expression of domestic income-distribution choices. Pettis has stated the insight identically across two decades of Carnegie commentary and Trade Wars Are Class Wars (2020),1 and stating it cleanly forecloses most of what the popular trade-conflict narrative gets wrong.

China's current account surplus — running at roughly 3% of Chinese GDP, the largest bilateral imbalance in the global system — is not a trade-policy outcome or a currency-manipulation outcome or a Chinese government conspiracy against the West. It is the mechanical result of a Chinese domestic income distribution in which households receive too small a share of output to clear that output domestically. Wages are suppressed relative to productivity. Household consumption sits at roughly 38% of GDP, a figure approximately twenty percentage points below the US level and meaningfully below every comparator in the developed world. State direction of investment continues to expand production capacity in steel, solar, electric vehicles, batteries, and semiconductors at rates that domestic demand cannot absorb. The surplus is forced onto global markets. It cannot be cleared at home because the institutional structures that would allow households to receive and spend more of Chinese output — independent unions, household-side social insurance, wealth taxation, a property regime that does not lock the household sector into a single deflating asset class — have not been built.

The absorption counterpart to that surplus is equally structural, and this is the part of the argument the popular discussion of trade conflict tends to omit. The dollar system — the US current account deficit, the Treasury market, the deep liquidity of dollar-denominated financial assets — is the global absorber of last resort because no alternative deep liquid market exists at the relevant scale. The eurozone does not have a comparably deep sovereign bond market, and the institutional fragmentation between national balance sheets and the ECB's mandate prevents one from emerging. Japan absorbs some of the surplus, and runs its own surplus dynamics that compound rather than offset China's. The United Kingdom is too small. Switzerland is too small. The dollar absorbs the surplus because it has to. That is the precise structural sense in which the dollar system survives — not because confidence holds, but because the alternative structures required to take the surplus elsewhere have not been built.

The conclusion Pettis draws from this — and the part of his framework that the popular trade-conflict narrative most consistently mishandles — is that the trade war is not the cause of the imbalance. It is the political symptom of it. The imbalance was already forcing rebalancing; the conflict is what politically-mediated rebalancing looks like when the structural adjustment is economically inevitable but domestically painful in both countries. American workers who have absorbed two decades of import competition without commensurate wage gains were not going to absorb a third. Chinese savers who have absorbed two decades of suppressed consumption without a domestic safety net were not going to absorb a third. The political reaction in each country is the form the structural adjustment takes when the institutional mechanisms for managing it through redistribution are blocked.

The investment implication Pettis draws from the framework is one the "diversify into emerging markets" narrative has not fully engaged. Surplus countries cannot diversify their consumers. If Chinese factories shift their export destination from the US to Europe to Southeast Asia, the global supply picture does not improve; it shifts geographically while remaining structurally unchanged. The "friend-shoring" and "China+1" manufacturing narratives are real at the margin — Vietnam, Mexico, and India are genuine beneficiaries of supply-chain diversification — but they describe a redistribution of where the addition lands, not a reduction in the addition itself. The overcapacity will continue to press on global margins in every sector it enters, because the domestic distribution mechanism that creates it has not changed. China's share of global manufacturing value-added is approximately 31% in 2024, up from around 22% in 2010 and 9% in 1990 — more than the United States, Germany, Japan, and South Korea combined, on UNIDO's series.2 That share is a global supply addition, not a substitution. The same motif that ran through The Energy Bottleneck and The Demographic Crunch runs through trade flows: addition not substitution. China adds capacity; the rest of the world does not relinquish its own; the global price level is set by the marginal producer with the lowest unit cost; and the dollar system is the financial absorber of the resulting imbalance because no alternative absorber of comparable depth exists.

Klein and Pettis make one further point that this essay needs to carry explicitly, because the casual reading of the framework as a critique of China obscures it. The surplus-country / deficit-country symmetry is structural, and the United States is the co-architect of the imbalance. The book's seventh chapter argues, on the empirical record of the post-1980s decades, that US financial deregulation was the deficit-side enabler of the surplus-side suppression. American workers' wage stagnation suppressed domestic consumption; US financial deregulation channelled cheap Chinese savings into US mortgage credit; American households consumed beyond their wage incomes by drawing down the credit the deregulated financial system extended to them; the consumption absorbed the Chinese surplus; the imbalance compounded. The trade-conflict narrative casts the US as the aggrieved party and China as the unfair competitor. The Pettis-Klein framework casts both as participants in the same distributional failure, expressed through different domestic institutions and producing the bilateral imbalance as the international shadow of the domestic policies on each side. The framework is not anti-China. It is also not anti-American. It is a structural diagnosis in which the two domestic distribution failures are mutually reinforcing, which is why the bilateral conflict is so politically combustible: each side can identify the other as the source of its problems and be partly correct, while the structural condition that makes both partly correct is identified by neither.

II. The Empirical Update — Setser's Reserve-Share Migration

The empirical operationalisation of Pettis's framework lives in the global capital-flow data, tracked in close to real time on Setser's Follow the Money.3 The bilateral imbalance moves faster than the popular discussion of it; the headline figure and the analytically load-bearing figure diverge in ways that change the diagnosis.

Begin with China's surplus, because the framing matters. Setser's tracking through 2024 documents China's goods-trade surplus at approximately one trillion dollars — the largest goods-trade surplus in world economic history. This is the number that has anchored the headline coverage of the imbalance. It is not, strictly, the same as China's current account surplus. The current account composite includes services, where China runs a structural deficit driven by Chinese tourists and students abroad, and the resulting current-account figure was approximately $700–900 billion in 2024 depending on which SAFE release one uses, with the IMF's April 2025 World Economic Outlook projecting a further rise in 2025.4 The distinction matters because Pettis's framework operates on the current account: it is the savings-investment imbalance that is the domestic distribution shadow, and the goods-trade figure overstates the imbalance by the value of the services deficit. The honest framing is that the current account surplus is approaching one trillion dollars and the goods-trade surplus, the more frequently cited figure, has already crossed that threshold. The surplus is expanding at a time when China's trading partners have less institutional capacity to absorb it than they did in the pre-2020 period.

The second Setser empirical anchor is foreign holdings of US Treasuries. The TIC data series tracks the share of marketable Treasury debt held by foreign entities — central banks, sovereign wealth funds, official reserve managers, and private foreign holders combined — and that share has fallen from approximately 50% in 2008 to approximately 30–32% by 2025–26.5 This is the empirical backbone of the dollar-system-extension argument. The decline is not a function of foreign sellers leaving the market in volumes that would qualify as a flight; it is a function of the total stock of Treasury debt growing faster than foreign holdings have grown. Foreigners are net buyers in absolute terms, on most measurement windows; they are simply not buying at the rate the issuance is expanding. The marginal Treasury buyer has therefore become increasingly domestic and increasingly mechanical. Private credit allocators are running Treasury collateral to lever insurance-mediated balance sheets. Stablecoin issuers, under the GENIUS Act, are running a mandated Treasury bid that scales with stablecoin issuance. The Federal Reserve's own balance sheet has cycled through QE and partial QT phases that have not, in net terms, returned the share of foreign holdings to the pre-2008 level. This is the mechanical, not informed motif operating at the sovereign debt layer: the foreign official-sector buyer who historically anchored the Treasury market through deliberate reserve management is being progressively displaced by buyers whose decision-making is regulatory-mandate-driven or algorithm-driven. There is no internal price-discovery brake on a regulatory bid.

The third Setser anchor is the structure of EM external sovereign debt. The CFR tracking work documents that approximately 70% of EM external sovereign bond issuance — bonds issued internationally to non-domestic investors — remains denominated in US dollars, on BIS international debt statistics.6 The "original sin" problem identified in the original Eichengreen-Hausmann-Panizza analysis has improved modestly in some markets — India, Brazil, and to a lesser degree Mexico have developed domestic sovereign bond markets that are increasingly investable by international participants in local currency — but the structural feature remains the dominant one. An investor "diversifying into EM" via the standard external-sovereign-debt route is not diversifying away from dollar exposure. They are adding sovereign credit risk, sovereign liquidity risk, and (often) political risk on top of the same dollar-denominated credit exposure they would have inside the US fixed-income market. This is the empirical version of the addition not substitution motif applied to capital flows: moving capital "elsewhere" via the most common EM debt instrument adds dollar-system exposure rather than substituting for it.

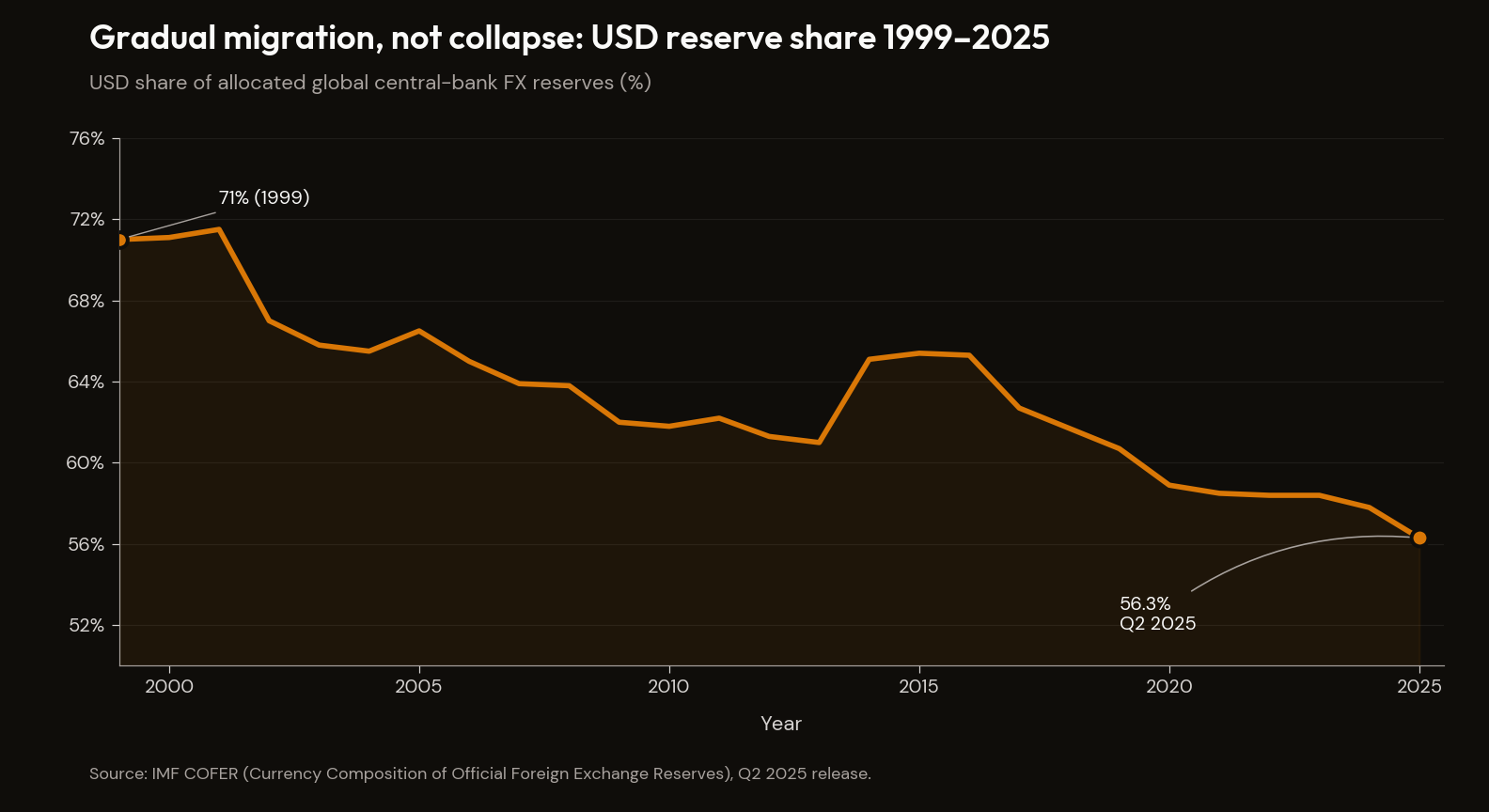

The headline reserve number is the IMF COFER series, falling from roughly 70% in 2000 to approximately 56–57% in 2024–25.7 That is a real decline — gradual, partial, and substantially absorbed by gold rather than by any rival currency. The renminbi sits at ~2.5%; a decade of explicit Chinese internationalisation policy has moved the dial by single percentage points. The arc is China-out, rest-of-world-in.

| Year | USD share | EUR share | JPY share | GBP share | RMB share | Other |

|---|---|---|---|---|---|---|

| 1999 | 71% | 18% | 6% | 3% | 0% | 2% |

| 2001 | 73% | 20% | 5% | 3% | 0% | <1% |

| 2010 | 62% | 26% | 4% | 4% | 0% | 4% |

| 2020 | 59% | 21% | 6% | 5% | 2% | 7% |

| Q2 2025 | 56.3% | 20% | 6% | 5% | 2.5% | 10% |

The story is gradual migration — RMB and "other" gaining share, USD losing — not collapse. A reserve share of 56% remains globally dominant by any standard.

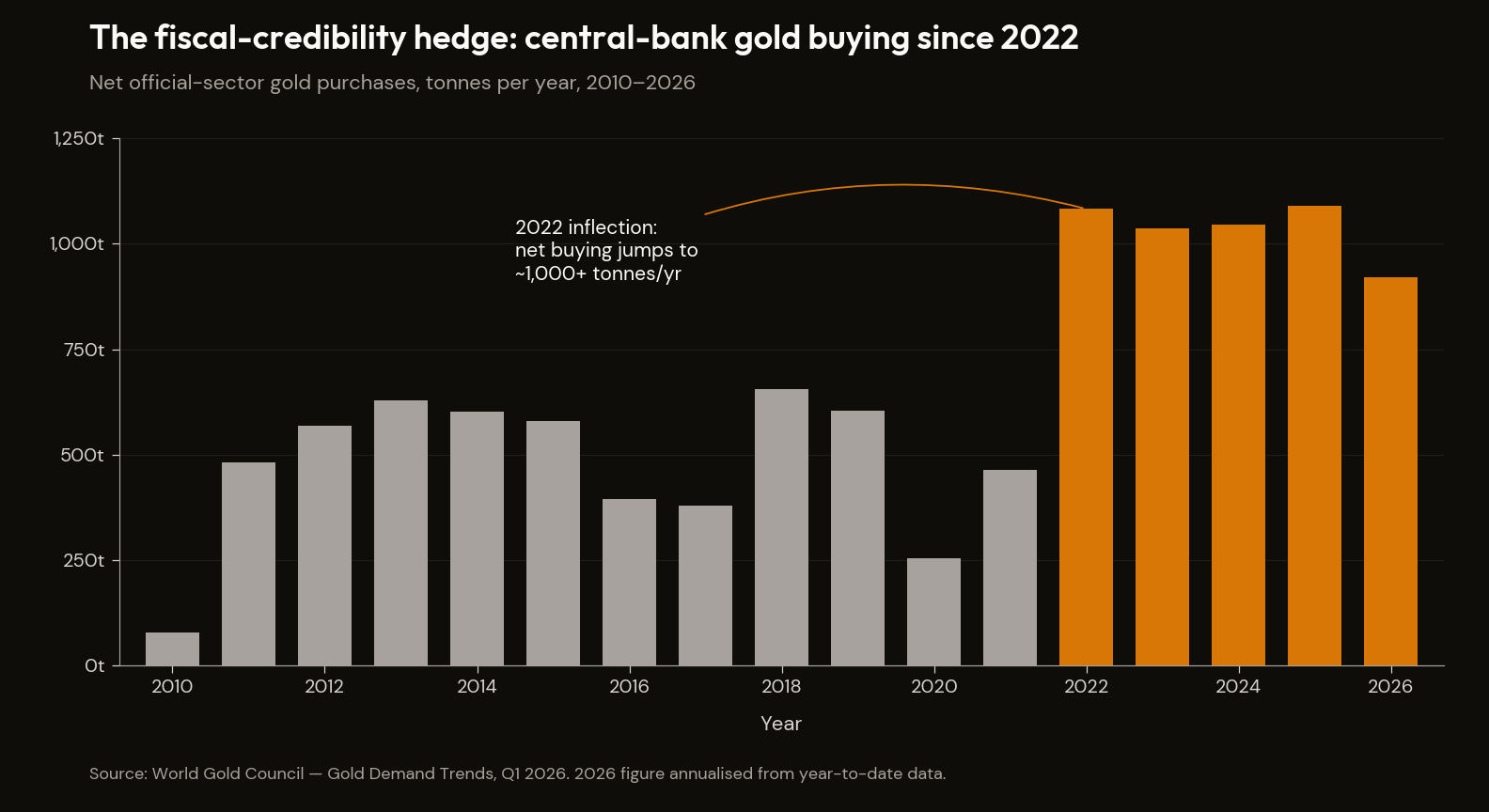

Central-bank gold purchases have increased, which is real and structurally significant — gold is now signalling the hedge-seeking behaviour the dedollarisation discourse predicted — but a hedge is not a replacement, and the volumes involved (roughly 1,000 tonnes per year of net official-sector purchases against a $13-trillion-plus stock of dollar-denominated foreign debt that requires servicing) are not at the scale required to displace the dollar system.8 The practical alternative-reserve argument runs into Pettis's architectural constraint: for any reserve asset to replace the dollar's monetary role, some country or institution must be willing to absorb global imbalances at scale by running a structural current account deficit large enough to supply the world with the reserve asset. No BRICS economy is structurally configured to do this. China, the largest, runs a structural surplus. The slow movement of the COFER series, despite a decade of explicit Chinese policy to internationalise the renminbi, is the empirical record on how slow this transition actually moves when it is progressing at all. The mechanism by which dollar dominance erodes is real; the timeline on which it materially shifts the investment landscape, on Setser's empirical record, is longer than the rotation thesis assumes.

The view from Cape Town sharpens the point. From inside an EM whose external sovereign bond stack is overwhelmingly dollar-denominated, the COFER decline is not the relevant series — the relevant series is the rand cost of servicing dollar debt at whatever the Fed's policy rate happens to be, and that cost is set not by the marginal reserve manager in Beijing or Riyadh but by the marginal Treasury buyer in Washington. South Africa's external sovereign curve, like nearly every EM-issuer curve outside India and Brazil, prices in dollars and pays in dollar cash flows that have to be earned through a rand revenue base whose own exchange rate is partly a function of dollar-system rotation. Dedollarisation from the EM-issuer side is not a thesis. It is a budget line. The reserve-manager rotation thesis is debated in central-bank policy departments; the EM-issuer's dollar-cost line is debated in every monthly cash-flow forecast a South African treasury team produces. The asymmetry between those two debates is the underweighted feature of the discussion when it is held from inside the dollar-system core.

III. The K-Shape Between Countries — Tooze's Corrective

The K-shape this manuscript has documented within economies — top quintile pulling away, the rest stagnating — operates with equal force between economies. Pettis's framework gets the income-distribution mechanism right but underweights the institutional context that determines which countries can manage the forced adjustment of surplus recycling and which cannot. Tooze's Crashed (2018), Shutdown (2021), and the ongoing Chartbook are the canonical corrective.9

The structural predecessor of this essay's argument is the central insight of Crashed: the 2008 financial crisis was a crisis of dollar-plumbing, not just of US mortgage finance. Tooze documented, on the post-2008 archival and central-bank-disclosure record, how the dollar-funding system — extended through dollar-denominated interbank credit, repo markets, and the international wholesale funding architecture — transmitted US mortgage stress into a global crisis within weeks. Central banks that had no direct exposure to US subprime mortgages found their commercial banks' dollar-funding locked up, because the system that cleared dollar-denominated transactions globally was seizing. The Federal Reserve's response — the swap lines extended to the ECB, the Bank of England, and a handful of other central banks; eventually the Mexico, Brazil, Singapore, and Korea swap lines — was the operational confirmation of the architectural reality: the dollar was not merely the reserve currency in a passive sense; it was the operational plumbing of the global financial system, and the Fed was the lender-of-last-resort to non-US institutions facing dollar-funding stress because there was no other entity with the balance sheet capable of clearing the system. The post-2008 institutional response did not change that structural reality. It deepened it. The Fed has been the contingent backstop of the global financial system from 2008 onward, in a way that the IMF, by design, cannot be at the relevant scale.

The K-shape between countries is the recovery-era expression of the same dynamic. Post-2020, Shutdown and the ongoing Chartbook analysis document a divergence in recovery trajectories that maps closely onto institutional capacity rather than onto geographic identity. G7 economies deployed fiscal stimulus at scale and recovered faster than any prior post-recession cycle. Emerging-market economies with weaker fiscal capacity — or with dollar-denominated external debt that tightened as the Fed's 2022–23 hiking cycle proceeded — experienced the global interest-rate tightening as a disproportionate shock. IMF data on the 2020–2024 recovery period shows that per-capita GDP in sub-Saharan Africa remained below pre-pandemic levels through 2023–24, while G7 per-capita GDP had exceeded pre-pandemic levels by 2022.10 The divergence is not uniform across EM. India and Vietnam outperformed the EM aggregate. Türkiye and Argentina produced their own currency-crisis arcs. The direction of the K-shape, however, is consistent across the major comparator data: institutional quality and current-account position — surplus versus deficit, domestic-currency versus dollar-denominated debt, fiscal capacity versus fiscal exhaustion — determined recovery trajectory more than any geographic abstraction did. Tooze's framing in the Chartbook commentary is that the K-shape is not a contingent feature of the post-2020 recovery; it is the structural feature of how a dollar-system shock transmits through institutionally heterogeneous absorbers, made unusually visible by the size of the shock.

The polycrisis frame — multiple independent crisis processes interacting and compounding rather than resolving sequentially, which Tooze popularised in Chartbook from 2022 onward — is the analytical reason the essay cannot be a simple "here is the good EM opportunity" piece. The post-2020 global environment has featured, simultaneously: the pandemic shock and its uneven recovery; the supply-chain disruption that exposed the integration limits of the just-in-time architecture; the fastest monetary tightening cycle in 40 years; the energy shock from the Ukraine war; the Chinese property sector implosion (with $5–6 trillion of wealth destruction in the developer complex); and the US-China trade conflict that has accelerated through every administration since 2017. These are not sequential crises that clear and allow normal conditions to resume. They are compounding stresses on a global system whose absorptive capacity was already stretched by the post-2008 decade of financial-repression-era capital flows. The investor who is "moving capital elsewhere" is moving it into the polycrisis environment, not away from it. The environment in which non-US assets are priced is the same environment in which US assets are priced, and the non-US assets do not have the dollar-system backstop the US assets have — even when the US assets are the immediate source of the stress.

The honest corrective on Pettis runs in two directions. First, Pettis identifies income distribution as the primary driver of current account imbalances, but the framework arguably underweights the role of state capacity and institutional context in determining which countries can manage the forced adjustment of surplus recycling and which cannot. The dollar-system architecture is not symmetric. When US deficits force dollar assets into global markets, the institutional capacity to hold and manage those assets is unevenly distributed. A country with deep capital markets, an independent central bank, and a domestic-currency sovereign bond curve can absorb dollar inflows and recycle them without forced asset-quality compromise. A country without those institutions absorbs the inflows in a more brittle configuration, and the unwinding — when the dollar tide ebbs — is correspondingly more violent. Second, Pettis's framework is centred on the US-China bilateral; Tooze would note that the European dimensions — Germany's structural surplus, Italy's structural fragility, the ECB's institutional constraints, the divergence between northern-European surplus countries and southern-European deficit countries — are not captured in the bilateral framing and are arguably more proximate sources of financial stress in the 2026–2027 watch window. The absence of eurozone fiscal union means the external surplus is not symmetrically distributed, and the resulting internal stresses transmit through bond-market spreads in ways the US-China framing does not engage. These corrections are refinements, not refutations. Pettis's mechanism is correct; the transmission paths are more institutionally heterogeneous than the bilateral framing implies, which is precisely why this essay's investment conclusion is institutional-quality rather than geographic.

IV. Rise of the Rest — Zakaria's Honest Update

The post-American world is not the anti-American world. The geopolitical multipolar transition has moved much faster than the monetary architecture — China, India, the Gulf, parts of Southeast Asia and Latin America now exercise foreign-policy and economic-policy agency insensitive to US preferences without organising in opposition to the US — and that distinction, sharpened across Zakaria's Post-American World (2008/2011) and Age of Revolutions (2024), disciplines the rise-of-the-rest framework against the triumphalism that dated the 2008 original by 2016. The post-American world is one in which American dominance is no longer the organising principle of international politics, while America remains a powerful and influential actor — perhaps the single most powerful — in an order whose other actors do not require American permission to act. The anti-American world is a world hostile to America, organising itself in opposition to American interests. The empirical record of the past twenty years is that the world is moving toward the former, not the latter. China, India, the Gulf, parts of Southeast Asia, parts of Latin America — these are powers whose foreign-policy and economic-policy choices are increasingly insensitive to US preferences, but they are not, in their majority, organised in opposition to the US. The distinction matters for this essay because it prevents two analytical mistakes that the popular discussion routinely commits: the mistake of treating "post-American" as a synonym for "dollar collapse" (it is not — the geopolitical multipolar transition has moved much faster than the monetary architecture, which is what Setser's data documents), and the mistake of treating "dollar persistence" as evidence that nothing has changed (it is not — the geopolitical landscape has changed in ways the monetary landscape does not yet reflect).

The three revolutions framework, from Age of Revolutions (2024), is the structural extension of this position and the part of the framework that this essay needs to anchor verbatim. Zakaria writes:

"Since the fall of the Berlin Wall in 1989, the world saw the liberalization of markets, the democratization of politics and the explosion of information technology. Each of these trends seemed to reinforce the other… We are living in an age of backlash to three decades of revolutions in different realms."

— Fareed Zakaria, Age of Revolutions: Progress and Backlash from 1600 to the Present (Norton, 2024)

The three revolutions identified — market liberalisation (1989–2008), democratic expansion (1989–2010), and information technology (1995–2020) — were each, in their original framing, supposed to reinforce one another and converge on a unified liberal order. Each, on Zakaria's reading of the past decade, has generated its own backlash. Markets opened, inequality surged, and protectionist politics returned. Democracy expanded, polarisation deepened, and illiberal democracy emerged. Information technology exploded, misinformation spread, and institutional trust collapsed. These are not three independent observations. They are the three revolutions whose interaction produces the K-shape between countries this essay is diagnosing — the K-shape that Tooze documents at the level of recovery trajectories is the macroeconomic shadow of the institutional divergence Zakaria's framework identifies at the level of regime type and democratic durability.

The institutional mechanism by which the divergence accelerates is the "illiberal democracy" pattern Zakaria identified in his 1997 Foreign Affairs article — the seminal piece in which he named a phenomenon that has since become the dominant institutional story of the past quarter-century:11

"Democratically elected regimes are routinely ignoring limits on their power and depriving citizens of basic freedoms."

— Fareed Zakaria, "The Rise of Illiberal Democracy," Foreign Affairs (November/December 1997)

The pattern — democratic mandate, illiberal consolidation, institutional capture — is the mechanism by which institutional divergence between countries accelerates over time. Strong-institutional countries have institutional structures resistant enough to block the slide; weak-institutional countries do not. Hungary under Orbán, Türkiye under Erdoğan, the Philippines under Duterte, Russia under Putin — each follows the same architectural pattern even where the political content differs. The democratic mandate is the entry vehicle; the institutional capture is the operational outcome. The investment-relevant point is that the K-shape between countries, in Zakaria's framework, is not primarily democratic versus authoritarian. It is strong-institutional versus weak-institutional, and the distinction predicts both economic trajectory and capital-flow patterns more accurately than the regime-type label alone.

The honest update on the original 2008 Post-American World thesis is the part of Zakaria's framework that the essay needs to engage cleanly, because the popular reading of "the rise of the rest" tends to lapse into either uncritical endorsement or dismissive rejection, and neither captures the structural reality. The thesis was never a prediction that non-Western countries would overtake the US in absolute per-capita terms by some particular date. It was a prediction that they would become consequential actors that the US cannot unilaterally dominate. On that more modest claim, the thesis has held, and the 2024 update in Age of Revolutions is honest about the asymmetry of the rise. China at $17–18 trillion of GDP, India as the world's fastest-growing large economy with a per-capita GDP under $3,000, Indonesia and Vietnam as genuine manufacturing platforms, Brazil as a major agricultural and commodities power — these are materially different from the 2008 baseline, and the geopolitical agency they exercise is not reversible by US policy choice. At the same time, the 2024 update is honest about what did not happen on the original timeline: China's economic model is now generating its own domestic stresses (the property sector implosion, deflationary overcapacity, the demographic cliff The Demographic Crunch documented); India's per-capita GDP remains an order of magnitude below the US; Brazil is institutionally fragile and cyclical; Russia's aggression has isolated it from the global capital base it would need to grow. The "rest" has risen, and the rise is uneven, and the K-shape within the rest is as analytically important as the K-shape between the rest and the developed world. The investor who treats "the rise of the rest" as a portfolio thesis without distinguishing between the institutional-strong and institutional-weak segments of that aggregate is buying the average of two distributions whose tails diverge.

V. Gold as Fiscal-Credibility Arbitrage

Gold is at roughly $4,700 an ounce on April 28, 2026. Central-bank net buying continues at a pace not seen since the 1960s, with the PBOC now in its seventeenth consecutive month of accumulation.8 The IMF's April 2026 Fiscal Monitor pulled forward by a year its projection for global public debt to pass 100% of global GDP; global net interest as a share of GDP has risen by half in four years.10

What gold is voting on, sitting above $4,700 while Treasury yields stay around 4.4%, is not the demise of the dollar specifically. It is the credibility of the fiscal path of the entity that issues the dollar. De-dollarisation implies a winner; fiscal-credibility scepticism implies an arbitrage. Gold is the arbitrage. Roughly 1,000 tonnes per year of net official-sector purchases against a $13-trillion-plus stock of dollar-denominated foreign debt is not at the scale required to displace the dollar system. Gold will continue to be bid for as long as the credibility deficit persists — a long time.

The most sophisticated proponents of the dedollarisation thesis — Russell Napier on financial repression, Zoltan Pozsar on Bretton Woods III as commodity-currency emergence — articulate real long-run structural pressure, and the engagement deserves to be on their strongest formulation rather than dismissed in passing. Napier's argument is that governments will use savers' assets to recapitalise themselves through regulated yields, GENIUS Act-style mandates, and QE-era mechanisms, and that under sufficiently adverse conditions the system could bifurcate into commodity-exporting blocs pricing commodities in non-dollar units. Pozsar's argument, articulated through his Credit Suisse research notes and subsequent independent commentary, is that a Bretton Woods III architecture is emerging in which commodity-backed currencies — anchored on energy, metals, and food rather than on sovereign credit — handle trade settlement. The dollar, on this reading, retains its financial-asset role but loses its commodity-pricing anchor as the geopolitical bifurcation proceeds. Russia priced energy in non-dollar units to a meaningful subset of buyers post-2022; the Gulf states have hedged settlement in renminbi for selected oil contracts; the BRICS new development bank is articulating an alternative trade-finance architecture.

Both Napier and Pozsar identify pressures that will compound over the coming decade. The honest engagement is on the timeline, not the direction. Alden's flywheel is the load-bearing counter — the ~$13 trillion of dollar-denominated debt outside the US creates inescapable transactional demand, and every BIS triennial survey since 2010 has confirmed the dollar's ~88% share of FX trading volumes against a falling but still-dominant ~57% reserve share. The commodity-settlement layer is real and gaining ground; the financial-architecture layer is durable and gaining depth. The two are not the same layer, and the dedollarisation thesis often conflates them. The renminbi at 2.5% of COFER after a decade of explicit Chinese policy effort is the empirical record of how slow the financial-architecture transition actually moves when it is progressing at all. Dedollarisation is a real long-run vector. It is not a near-term investment thesis.

VI. EM Credit Divergence

The portfolio-rotation thesis holds that US equity valuations are stretched, dollar risk is building, and capital should flow to cheaper, faster-growing markets outside the US. The thesis is correct in direction — US equity valuations are stretched (Bull Run, Mag 7), much of non-US equity trades at a substantial discount to long-run earnings power, and a mechanical reversion of US equity multiples from current levels to long-run averages would be among the largest wealth-transfer events in investment history. The capital that moved early and selectively into non-US markets would capture some of that reversion. The structural case for the rotation is real; the proponents who hold a non-trivial allocation away from US equities at current levels are not making an arithmetic error.

The thesis is incomplete in the abstraction. The problem is not the direction of the argument but the geographic level at which it is implemented. "Non-US equity" is not an asset class. It is a collection of markets with wildly different institutional architectures, current-account structures, dollar-debt exposures, and demographic trajectories. The investor who buys the iShares MSCI Emerging Markets ETF in response to the US valuation problem has not diversified away from dollar exposure; they have added currency mismatch and liquidity risk to a portfolio whose underlying companies still derive a meaningful share of their revenue and financing from dollar-denominated transactions. The MSCI Emerging Markets weight in the broader MSCI ACWI has fallen from approximately 13% in 2010 to approximately 10–11% in 2026,12 even as the structural case for individual emerging markets has strengthened on the fundamentals — precisely because the aggregate "EM" category is dominated by markets with dollar-debt overhangs, institutional fragility, or single-name index dominance (the China weight inside EM is approximately 25–30%, which makes the "ex-China EM" trade a materially different position from the headline EM allocation). The investor who buys Japanese equities adds a yen-carry dynamic and a demographic structure even more severe than the US to their portfolio. The investor who buys European equities adds the ECB's institutional constraints, Germany's manufacturing transition, France's fiscal trajectory, and Italy's debt-to-GDP at 137%.10 The aggregate-geography rotation is a partial truth that hides the institutional heterogeneity.

The real diversification axis, the one Pettis's framework implies and Setser's data confirms, is institutional structure and current-account configuration. Countries that run current account surpluses, with domestic-currency-denominated sovereign debt, strong rule of law, and productive working-age demographics, are structurally less exposed to the dollar-system dynamics the diagnostic block documents. The list is short. Singapore. Switzerland. Parts of Scandinavia. India, on demographics and the manufacturing-shift trajectory, with significant institutional caveats. Vietnam, as a structural manufacturing beneficiary, with limited capital-market depth that constrains the size of position any institutional investor can take. Mexico, as the structural nearshoring beneficiary, with peso-denominated domestic earnings but significant dollar-pass-through in traded goods. None of these is "diversification out of the dollar system." They are diversification into institutional structures that are better positioned to manage within the dollar system when it is under stress. That is the sharpened version of the rotation thesis, and it is the version that this essay's structural argument supports.

South Africa sits on the wrong side of that axis on most institutional readings and on the right side on a narrower one. The rand is the most-traded EM currency outside Asia, the JSE has a settlement architecture that survived the post-2008 stress events, the Reserve Bank's inflation-targeting record is among the cleanest in the EM cohort, and the sovereign domestic-currency curve is meaningfully developed by EM standards. None of that makes the country a candidate for the "institutional-quality EM" allocation a Singapore or Switzerland would qualify for. It does mean that the South African case is the live test of how far an EM with mid-quality institutions can run the rotation thesis from the destination side — and the answer on the recent record is that the running is constrained more by political-economy execution than by the architectural features the rotation thesis selects on. The full case belongs to SA and Africa.

The motif this section needs to surface explicitly is the one that has run through The Energy Bottleneck, The Demographic Crunch, and the trade-imbalance discussion above: addition not substitution. Capital flows "elsewhere" mostly add exposure to the dollar system rather than substituting for it. The investor who moves from US Treasuries to Mexican peso-denominated government bonds has added currency exposure but is still holding the debt of an economy deeply integrated into the US-dollar trade-financing system. The investor who moves from US equities to Indian equities is holding companies whose growth depends partly on the same global liquidity cycle that drives US risk-asset valuations. The substitution model — exit US risk, enter non-US safety — is a partial truth that hides a structural reality: the same forces operate everywhere, with different intensities and different institutional buffers, and the "elsewhere" the investor reaches for is mostly a geographic relocation of the same exposure rather than a substitution for it.

VII. Institutional Quality as the Discriminator

The argument is the manuscript's structural case. The counter-arguments deserve engagement on their strongest formulation.

The China-collapse thesis. The strongest version observes that China's property sector implosion has destroyed $5–6 trillion of wealth, that youth unemployment crossed 20% in 2023 before the series was discontinued, that deflationary CPI prints have characterised 2023–24, and that the demand-rebalancing Pettis says cannot happen via market forces may in fact be happening via a severe deflationary adjustment — which would, if it proceeded, resolve the global overcapacity problem through Chinese contraction. The Pettis framework directly addresses this. Resolution via deflation is not a structural rebalancing; it is the absence of rebalancing, achieved through economic contraction rather than institutional reform. The global implication of Chinese deflation is not benign. Chinese deflation exports itself through lower export prices, compressing margins of manufacturers everywhere else; the "China dumping" framing that AI Reckoning applied to the AI-hardware dimension generalises across the industrial complex. Global manufacturing deflation favours Chinese exporters (more market share in a price-war environment, lower unit costs against scale) at the expense of higher-cost manufacturers in Europe, Japan, Korea, and the US. The overcapacity problem is reduced in volume terms by Chinese contraction, but the global competitive dynamics of that reduction are not positive for the non-Chinese manufacturers the rotation narrative assumes will benefit. The "China collapses, the world rebalances" version of the bull case for non-China EM is a misreading of how Chinese contraction transmits internationally.

The EM-diversification-works thesis. The empirical record of 2024–25 shows selective non-US outperformance: Indian equities outperformed in dollar terms through 2024, Brazilian equities had a strong 2024 first half, Vietnam and Mexico attracted genuine FDI on the nearshoring narrative. The honest counter is not that EM diversification never works. It is that geographic diversification is necessary but not sufficient, and that the abstraction level at which most investors implement it (broad EM ETF, headline non-US allocation) replicates dollar-system exposure in less liquid form. The investors who outperformed in 2024–25 were doing institutional-quality and current-account selection at the country and sector level, not passive aggregate-geography allocation. The aggregate has fallen as a share of global indices over fifteen years even as the structural case for individual markets has strengthened, which is the empirical signal that the aggregate is the wrong unit of analysis.

The post-American-world-is-geopolitical-not-financial thesis. The strongest formulation holds that Zakaria's framework is primarily geopolitical — the rise of the rest is about diplomatic leverage — and the financial architecture is a separate domain that can coexist indefinitely with dollar monetary dominance. Both halves are true in different timeframes. In the near term, on Setser's empirical record, the dollar's monetary architecture is durable. In the medium term, if US institutional trust continues to erode (Zakaria's explicit concern in Age of Revolutions), the financial architecture eventually follows. This is not a contradiction; it is the timing-is-the-question distinction the manuscript applies across all of its structural arguments.

The Pettis-is-anti-China critique. A specific reading of Trade Wars Are Class Wars — held in some Chinese academic and Washington-think-tank quarters alike, for different political reasons — is that the framework assigns primary responsibility for global imbalances to China while exonerating US consumption and US fiscal policy, and is therefore a sophisticated dressing of the trade-deficit grievance. The text directly refutes this. Klein and Pettis make the US-as-co-architect point explicitly and repeatedly. The framework is structurally even-handed in a way that makes both the pro-China and the pro-US political readings uncomfortable, which is one of the reasons it is the most useful framework for this essay's purposes.

Pull the threads. The dollar system did not collapse. It migrated and deepened. China's surplus is the mechanical result of a domestic distribution that under-pays its households relative to productivity; the dollar absorbs that surplus because no alternative deep liquid market exists at scale; the COFER series is a slow rebalancing of the reserve composition, not a dramatic collapse; gold is the fiscal-credibility arbitrage, not the de-dollarisation trade; the K-shape between countries transmits the polycrisis through institutionally heterogeneous absorbers; the geopolitical multipolar transition is real and not the same as the monetary one; and the headline EM rotation reproduces dollar-system exposure in less liquid wrappers without capturing the institutional-quality differentiation that drives the structural case.

The investment axis that matters is institutional quality and current-account structure. Geography is the abstraction that hides it.

Elsewhere is mostly still here. That is the uncomfortable shape of the post-American world.

Footnotes

-

Michael Pettis — Carnegie Endowment expert page. Book: Matthew C. Klein and Michael Pettis, Trade Wars Are Class Wars (Yale University Press, 2020). ↩

-

UNIDO — World Manufacturing Production reports; World Bank — Manufacturing, value added (% of GDP). ↩

-

Brad Setser — Follow the Money blog, Council on Foreign Relations. ↩

-

Adam Tooze, Chartbook. Book-length context: Crashed (Viking, 2018); Shutdown (Viking, 2021). ↩

-

Fareed Zakaria, "The Rise of Illiberal Democracy," Foreign Affairs (Nov/Dec 1997). Book-length extensions: The Post-American World: Release 2.0 (Norton, 2011); Age of Revolutions (Norton, 2024). ↩